Have you ever thought about what it would look like browsing your favorite online store or shopping in Dubai's busy malls when you come across something you adore, such as a stylish device, a high-end dress, or perhaps your ideal getaway?

But instead of paying the full amount up front, you split the cost into manageable, interest-free installments. This is how Buy Now, Pay Later (BNPL) apps like Tabby work their magic, transforming the way consumers shop in the United Arab Emirates and others. Have you ever pondered what it takes to create a revolutionary software like Tabby in a metropolis as vibrant as Dubai?

Developing a BNPL app involves more than just writing code; it involves designing a smooth, safe, and intuitive user experience that combines innovative finance with state-of-the-art technology. The BNPL app development cost in Dubai depends on a number of factors, including features, market demands, and the integration of payment gateways and adherence to the stringent requirements of the United Arab Emirates.

In this article, we’ll break down the cost to develop a BNPL app like Tabby, diving into the tech stack, design, and regulatory hurdles.

Industry estimates indicate that fees might range from AED 200,000 to AED 1,500,000, contingent on the app's complexity and scope. Let's look at the variables that affect these numbers and how you may achieve your BNPL goal in the heart of Dubai's thriving financial sector.

Tabby App: Key Figures & Stats

In Dubai and elsewhere, Tabby, the top Buy Now, Pay Later (BNPL) platform in the MENA area, has revolutionized financial flexibility and purchasing. Key numbers and statistics illustrating its expansion, influence, and effectiveness in the BNPL app development market are shown below.

Finance Related Market Insights for Dubai Market

The financial sector serves as the cornerstone of Dubai's economy and firmly establishes the emirate as a significant global financial hub. Innovation, prudent policies, and high investor trust have all contributed to Dubai's banking sector's success.

Below are key statistics highlighting its scale, growth, and pivotal role in the BNPL app development cost in the Dubai ecosystem.

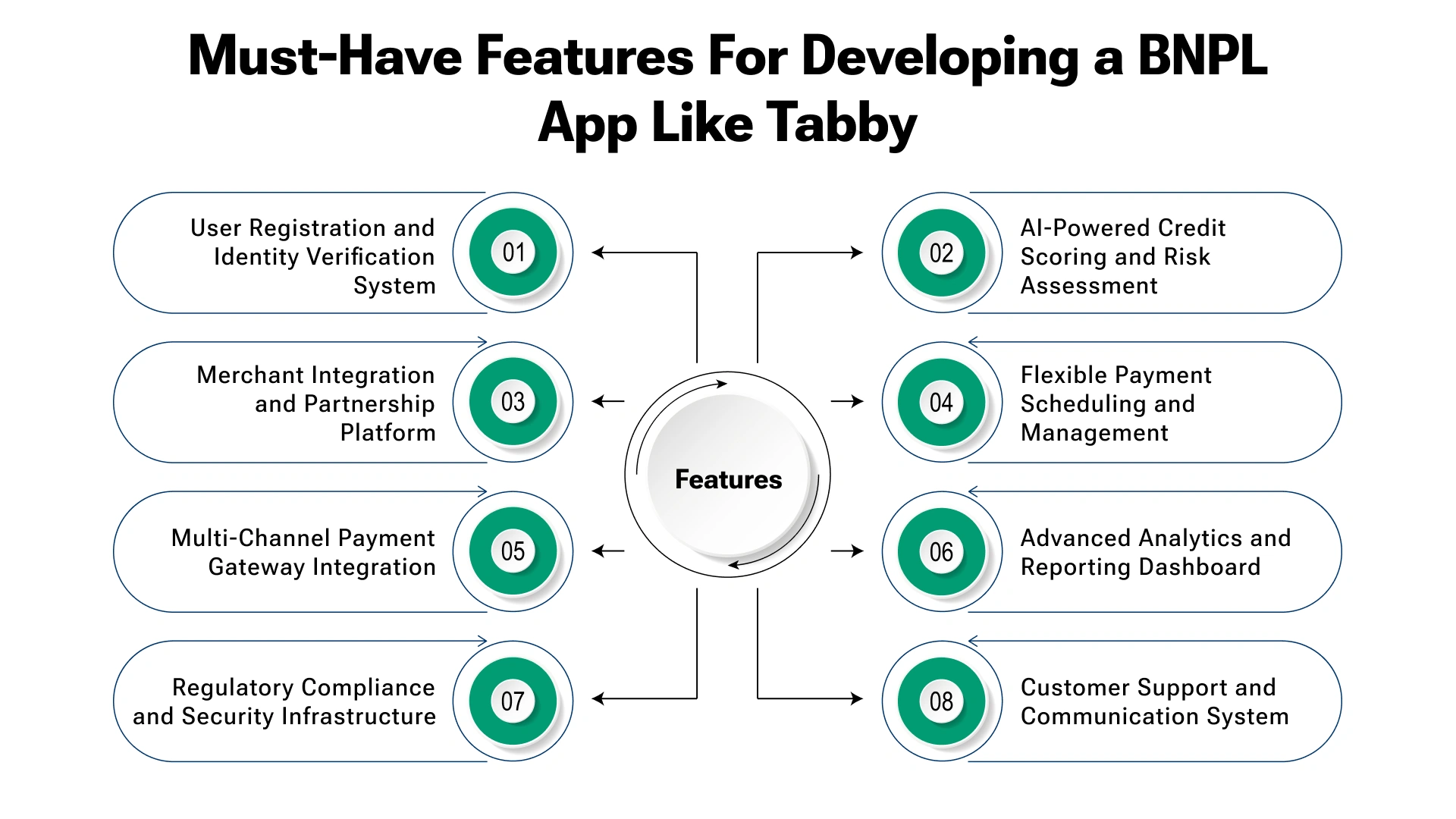

Must-Have Features For Developing a BNPL App Like Tabby in Dubai's Fintech Market

Building a mobile app like Tabby requires careful preparation and a large financial commitment in order to compete in Dubai's rapidly growing fintech sector. Businesses and entrepreneurs that want to get into this lucrative sector must understand the cost to develop a BNPL app like Tabby.

This thorough analysis looks at the key components and related development expenses needed to make a successful Tabby-like application.

1. User Registration and Identity Verification System

A strong user onboarding system that guarantees security and compliance with regulations is the first step in building any BNPL platform. Users must register using verified credentials, such as an email address, phone number, or social media integration, and then undergo stringent identification verification processes in compliance with UAE banking legislation.

Dubai's BNPL app legal compliance standards necessitate stringent know your customer (KYC) and anti-money laundering (AML) procedures. In order to assess creditworthiness, this involves confirming government-issued identification, integrating Emirates ID, authenticating pay certificates, and linking bank accounts. Any Tabby-like app development Dubai project must have a streamlined verification procedure that strikes a balance between user experience and regulatory standards, as demonstrated by Tabby's success.

Development Cost Range: $25,000 - $40,000

2. AI-Powered Credit Scoring and Risk Assessment

A BNPL app's primary feature is its ability to quickly assess credit using sophisticated algorithms and machine learning models. This program analyzes user data, financial information, spending patterns, and employment history to establish creditworthiness in real-time, much like Tabby's quick approval system.

Integration with UAE credit agencies like Emcredit and Al Etihad Credit Bureau (AECB) is essential for a comprehensive risk assessment. The system must handle a number of data sources, including bank statements, transaction histories, and salary certificates, in order to produce reliable credit profiles. The BNPL app development cost in Dubai is significantly impacted by this complex backend infrastructure due to the advanced AI and machine learning requirements.

Development Cost Range: $45,000 - $70,000

3. Merchant Integration and Partnership Platform

Retail partners and e-commerce platforms must integrate seamlessly for a BNPL app to be effective. The program must have easy-to-implement APIs, plugins for popular platforms like Shopify and Magento, and merchant point-of-sale (POS) system connectors for physical businesses.

Tabby's extensive merchant network in the United Arab Emirates, settlement management, risk-sharing agreements, and real-time transaction processing all serve as examples of the value of robust partnership tools like merchant dashboards. The creation of the BNPL Dubai mobile app must take into consideration a number of integration challenges with both domestic and foreign payment systems, which will impact the total cost of mobile app development.

Development Cost Range: $35,000 - $55,000

4. Flexible Payment Scheduling and Management

The core functionality of splitting purchases into installments requires sophisticated payment scheduling systems. Users should be able to choose from various payment plans (typically 3-4 installments over 6-8 weeks), view upcoming payments, and manage their payment schedule seamlessly.

The system must handle automatic payment processing, failed payment recovery, grace periods, and late fee calculations while maintaining transparency about terms and conditions. The assessment of the budget by BNPL app development company in Dubai is strongly impacted by this feature since it necessitates intricate backend logic and interaction with numerous payment channels.

Development Cost Range: $30,000 - $45,000

5. Multi-Channel Payment Gateway Integration

For BNPL apps, secure payment processing is essential, necessitating integration with a variety of payment methods, such as digital wallets like Apple Pay and Google Pay, foreign credit cards, local UAE banks, and other payment methods. Both one-time payments and recurring invoicing for installments must be supported by the system.

The development process becomes more complex when local banking laws, PCI DSS requirements, and 3D Secure authentication are followed. In order to provide smooth transaction processing across all channels, the integration must manage multiple currencies, mainly AED and USD.

Development Cost Range: $25,000 - $35,000

6. Advanced Analytics and Reporting Dashboard

Comprehensive analytics are necessary for both users and merchants to monitor payment histories, spending trends, and financial insights. Like Tabby's user interface, the app should offer comprehensive transaction data, spending classification, budgeting tools, and financial wellness indicators.

The platform must provide merchants with risk assessment reports, settlement tracking, sales statistics, and customer insights. Real-time data processing capabilities and integration with business intelligence tools are necessary for this functionality, which raises the overall development cost considerably.

Development Cost Range: $20,000 - $30,000

7. Regulatory Compliance and Security Infrastructure

Financial services compliance, data protection laws, and Central Bank of UAE (CBUAE) requirements must all be followed when operating in Dubai's regulated fintech ecosystem. Strong security features, including fraud detection systems, end-to-end encryption, and frequent security audits, must be included by the app.

Fair lending procedures, clear pricing structures, and consumer protection laws are all included in the BNPL app's legal compliance. Regulatory reporting capabilities, thorough audit trails, and data residency requirements for UAE operations must all be included in the development.

Development Cost Range: $40,000 - $60,000

8. Customer Support and Communication System

Managing payment-related inquiries, resolving disputes, and providing user support all depend on efficient customer service. Numerous support channels, such as in-app chat, email ticketing, phone support, and chatbots driven by AI for immediate responses, should be integrated within the app.

Payment reminders, past-due alerts, client education materials, and proactive account status communications must all be managed by the system. Efficient customer relationship management is ensured by integration with CRM systems and automated communication procedures.

Development Cost Range: $15,000 - $25,000

9. Automatic Payment Deduction System

Tabby's signature feature allows automatic deduction of installment payments from users' linked bank accounts or cards on scheduled dates. This system requires sophisticated payment orchestration, handling multiple payment methods as backup options, and intelligent retry mechanisms for failed transactions.

The automatic deduction system must integrate with UAE banking APIs, handle currency conversions, manage payment scheduling across different time zones, and provide users with full control over their payment methods. This feature significantly reduces manual payment friction and improves collection rates.

Development Cost Range: $20,000 - $35,000

10. Integrated Dispute Resolution and Chargeback Management

A comprehensive dispute handling system that allows users to raise concerns about transactions, request refunds, and manage chargebacks directly within the app. The system should include merchant notification workflows, evidence collection tools, and automated dispute tracking.

This feature requires integration with payment processors' dispute APIs, merchant communication systems, and regulatory compliance for consumer protection laws in the UAE. The dispute resolution system must handle various scenarios, including delivery issues, product quality concerns, and unauthorized transactions.

Development Cost Range: $25,000 - $40,000

11. In-App Shopping Discovery Platform ("Shop" Feature)

Tabby's integrated shopping platform allows users to discover and purchase from partner merchants directly within the app. This marketplace-style feature includes product catalogs, search functionality, merchant profiles, and seamless BNPL checkout integration.

The shop feature requires extensive merchant onboarding tools, product data management, inventory synchronization, recommendation engines, and integrated payment processing. This significantly expands the app's functionality beyond simple payment processing to become a complete shopping ecosystem.

Development Cost Range: $50,000 - $80,000

12. Spending Limits and Credit Management Tools

Dynamic spending limit management that adjusts based on user payment history, creditworthiness, and risk assessment. Users should be able to view their available credit, pending payments, and credit utilization in real-time.

This feature includes credit limit increase requests, temporary limit adjustments, and integration with the AI credit scoring system to provide personalized credit management recommendations.

Development Cost Range: $15,000 - $25,000

How Much Does it Cost to Develop a BNPL App Like Tabby: Average Breakdown

The cost to develop a BNPL app like Tabby depends on several factors—app complexity, design, feature set, and the development partner you choose.

Whether you're working with a BNPL app development agency in Dubai or a top mobile app development company in Dubai, understanding the breakdown by phases can help you plan your budget smartly.

Cost Breakdown by Development Phase

| Phase | Key Activities | Hours | Cost (AED) |

| Research and Planning | Market study, user flow mapping, defining business logic (including Sharia-compliant features) | 80–120 | 12,000–30,000 |

| UI/UX Design | Wireframes, custom BNPL interface design, user journey optimization | 120-200 | 18,000–50,000 |

| Frontend Development | App interface for iOS & Android using Flutter or React Native | 350–500 | 52,500–125,000 |

| Backend Development | API development, transaction management, payment gateways, user accounts | 450-700 | 67,500–175,000 |

| Compliance Features | Sharia-compliant logic, legal framework, and data privacy setup | 80-150 | 12,000–37,500 |

| Third-party Integration | KYC tools, payment processors, BNPL credit assessment modules | 150-300 | 22,500–75,000 |

| Testing & QA | Security, performance, and functionality testing across devices | 100-200 | 15,000-50,000 |

| Launch & Support Setup | Deployment, app store compliance, launch prep | 50-100 | 7,500–25,000 |

| TOTAL COST | 1,380–2,270 hours | AED: 207,000–567,500 |

Additional Costs

These extra costs ensure your BNPL app performs smoothly post-launch and reaches your target users

| Category | Specific Services | Cost (AED) |

| Server Hosting | AWS, Google Cloud, or Azure setup | 5,000-15,000 |

| Third-Party Tools | Payment gateway fees, SMS, analytics tools | 4,000-12,000 |

| Marketing & ASO | App store optimization, digital ads, influencer marketing | 10,000–40,000 |

| Ongoing Maintenance | Bug fixes, feature updates, compliance changes | 5,000–20,000/month |

| TOTAL COST | 24,000-87,000 |

Total Estimated Cost to Build a BNPL App Like Tabby

| App Tier | Estimated Cost (AED) | What You Get |

| MVP (Basic) | 150,000–300,000 | Core BNPL features, payment integration |

| Mid-Tier App | 300,000–500,000 | Enhanced UI/UX, credit logic, third-party tools |

| Full-Scale Tabby-like App | 500,000–900,000+ | Sharia compliance, advanced analytics, KYC, real-time decision-making |

For businesses exploring Sharia-compliant BNPL app development in Dubai, working with an experienced BNPL app development agency in Dubai ensures your platform aligns with local financial norms while delivering top-tier functionality.

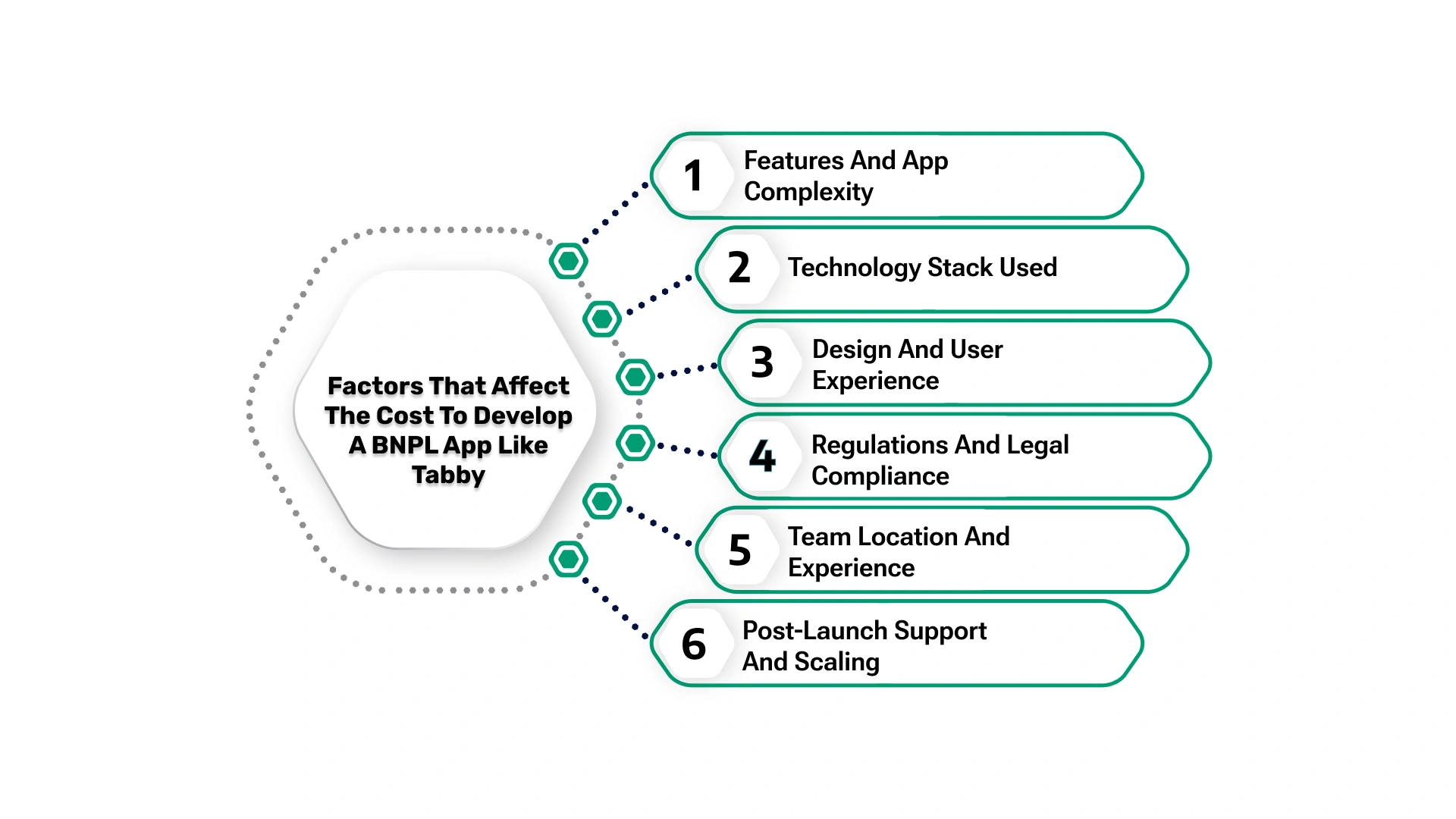

Factors That Affect the Cost to Develop a BNPL App Like Tabby

Writing code is only one aspect of developing a BNPL application. A number of crucial variables affect the cost to develop a BNPL app like Tabby. Understanding these elements helps with smart planning and accurate fintech app development budget estimation.

1. Features and App Complexity

The more features your app has, the more it will cost. A basic app might only let users split payments. But a full-featured solution like Tabby includes:

- User onboarding with secure KYC checks

- Merchant dashboards

- Credit score assessment

- Payment tracking and reminders

- Purchase history and spending analytics

Building a Tabby-like app development in Dubai means adding trusted financial tools and local integrations, which increases both time and cost. Expect a higher budget if you want a smooth, secure user experience.

2. Technology Stack Used

The choice of technology stack plays a major role in your app’s performance and cost. Most BNPL apps use:

- Frontend: Flutter or React Native for building Android and iOS apps together

- Backend: Node.js or Django to handle complex user data and transactions

- Database: PostgreSQL or Firebase for real-time data

- Cloud: AWS or Google Cloud for scalability

Choosing the right tools improves speed and security, but advanced tech may raise the cost to develop a BNPL app in Dubai.

3. Design and User Experience

Users in Dubai expect apps to be clean, fast, and easy to use. Investing in UI/UX design services—like mobile-friendly screens, user-friendly flows, and brand consistency—improves user trust. But that also adds to your budget.

Better design usually means more development hours. Still, it plays a major role in customer retention and satisfaction.

4. Regulations and Legal Compliance

BNPL apps must follow the UAE's financial regulations. This includes secure user verification (e.g., Emirates ID or UAE Pass) and data protection rules. Legal and compliance-related costs can include:

- Secure authentication systems

- Privacy policy and terms drafting

- Advice from local fintech lawyers

Ignoring this step can lead to fines. So, budgeting for compliance is a must in any fintech app development budget estimation.

5. Team Location and Experience

Where and whom you hire makes a difference. Hiring developers in Dubai offers local market insights, but it comes at a higher hourly rate. Offshore developers from India or Eastern Europe may lower your cost of an MVP for a BNPL app Dubai, but could require more communication effort.

For best results, work with a team experienced in financial apps and compliance.

6. Post-Launch Support and Scaling

After launch, ongoing app updates and maintenance, bug fixes, and user support will add to long-term costs. You may also need to scale the app to handle more users or merchants. Keeping some budget aside for maintenance ensures your app stays competitive in the fast-growing BNPL space. Typically, it costs 15-20% of the initial development annually.

Choosing the Right Pricing Model for Your BNPL App

Building a Buy Now, Pay Later (BNPL) app like Tabby is exciting, but picking the right pricing model can make or break your budget. A Mobile App Development Company in Dubai will offer different ways to charge for their work.

Each model has its perks and pitfalls, so let’s break them down in a simple, human way to help you decide what’s best for your BNPL app development agency Dubai project.

| Pricing Model | What It Means | Best For | Pros | Cons |

| Fixed Price | You agree on a set cost for the entire project, based on clear and final requirements | Best when your BNPL app has a well-defined scope and no major changes are expected. | Easy to manage budget Low financial risk | Hard to make changes once the project starts May limit flexibility for scaling later |

| Time and Materials | You’re billed for hours and resources used. Great if the scope might evolve | Ideal for developing complex or Sharia-compliant BNPL app development in Dubai, where features are added in stages | Highly flexible Adapts to new ideas and user feedback | Costs can increase if the scope isn’t tightly managed |

| Dedicated Team | You hire a full-time team (developers, designers, QA) on a monthly basis | Perfect for long-term projects that require continuous development and updates | Full control over the project Team grows with your needs | Higher upfront cost Needs strong project management from your side |

| Hybrid Model | A combination of a fixed price for basic features and time/materials for extras | Great when you want a balance, predictable budget with room for changes | Best of both worlds Ideal for phased rollouts | Slightly more complex to manage Needs good communication with your agency |

Tips to Save Money on BNPL App Development Like Tabby

Building a sophisticated Buy Now, Pay Later application similar to Tabby doesn't have to drain your entire budget. While understanding the cost to develop a BNPL app like Tabby is important, knowing how to optimize these expenses can make the difference between a successful launch and a financial burden.

The good news? Smart entrepreneurs in Dubai's thriving fintech scene have discovered numerous ways to reduce the BNPL app development cost in Dubai without sacrificing quality or functionality.

1. Start Smart with an MVP Approach

The biggest mistake many founders make is trying to build everything at once. Instead, focus on creating a minimum viable product (MVP) that captures the essence of what makes Tabby successful. For those wondering how much does it cost to create a BNPL app in Dubai, starting with an MVP can reduce initial expenses by 40-60%.

Your MVP should include core features like user registration, basic credit assessment, simple installment splitting (3-4 payments), and essential merchant integration. Skip the fancy AI-powered spending insights, advanced analytics, and premium customer support features for now. A well-planned MVP for BNPL app development services typically costs between AED 180,000-350,000, compared to AED 500,000+ for a full-featured platform.

This approach allows you to test market demand, gather real user feedback, and secure initial funding before investing in advanced features. Many successful fintech companies in Dubai have used this strategy to validate their concepts before scaling up.

2. Choose Your Development Team Wisely

One of the most effective ways to reduce the cost of BNPL app development agency in Dubai through strategic outsourcing. Building an app like Tabby entirely with an in-house team in Dubai can cost AED 200-400 per hour, pushing your total budget well beyond AED 500,000-800,000.

Outsourcing Benefits:

- Cost Reduction: Offshore development teams charge AED 75-150 per hour, offering 50-70% savings on development costs

- Access to Global Talent: Tap into specialized fintech expertise from regions with strong technical capabilities

- Faster Time-to-Market: Round-the-clock development cycles across different time zones

- Scalability: Easily scale your team up or down based on project phases

Smart Hybrid Outsourcing Strategy: Rather than full outsourcing, adopt a hybrid approach to maximize savings while maintaining quality:

- Keep critical functions local: Partner with a mobile app development for fintech Dubai company for regulatory compliance, payment gateway integration, and project management (20-30% of total work)

- Outsource routine tasks: Backend development, UI implementation, testing, and documentation to experienced offshore teams (70-80% of total work)

This strategic outsourcing approach can reduce your overall development costs by 35-50% compared to an entirely local team, while ensuring compliance with UAE financial regulations. When selecting outsourcing partners, prioritize those with proven Financial Software Development Services experience and robust security protocols - the initial savings from choosing the cheapest option often disappear due to quality issues, security vulnerabilities, and project delays.

3. Leverage Existing Payment Infrastructure

One of the most expensive components of any BNPL app is the payment processing system. Instead of building everything from scratch, smart developers focus on BNPL payment gateway integration UAE using established providers like Network International, PayTabs, or Checkout.com.

These platforms already handle the complex regulatory requirements, fraud detection, and multi-currency processing that would cost hundreds of thousands to develop independently. By integrating existing solutions, you can reduce payment system development costs from AED 150,000-250,000 to just AED 40,000-70,000 for integration and customization.

Additionally, many payment providers offer favorable terms for promising fintech startups, including reduced transaction fees during the initial growth phase and technical support for integration challenges.

4. Embrace Open-Source Technologies

The fintech world has embraced open-source technologies, and for good reason. Using proven frameworks like React Native for mobile development, Node.js for backend services, and PostgreSQL for database management can dramatically reduce licensing costs and development time.

For BNPL app development services, consider these cost-effective technology choices:

- Frontend: React Native or Flutter for cross-platform mobile development

- Backend: Node.js with Express or Python with Django

- Database: PostgreSQL or MongoDB for flexible data management

- Cloud Infrastructure: AWS or Google Cloud with startup credits

These technologies are not only cost-effective but also widely supported, making it easier to find skilled developers and ensuring long-term maintainability of your application.

5. Navigate Sharia Compliance Smartly

For those developing Sharia-compliant BNPL app development Dubai solutions, compliance doesn't have to be prohibitively expensive. Instead of hiring expensive Islamic finance consultants from day one, start by researching existing Sharia-compliant fintech frameworks and consulting with local Islamic scholars during the design phase.

Many successful Sharia-compliant BNPL platforms have built their compliance framework incrementally, starting with basic profit-sharing models and gradually adding more sophisticated Islamic finance features. This approach can reduce initial compliance costs from AED 100,000+ to AED 30,000-50,000 while ensuring your product meets religious requirements.

6. Smart UI/UX Investment Strategy

User experience is crucial for BNPL apps, but you don't need to spend a fortune on custom designs. Start with proven UI/UX patterns from successful fintech apps, then hire UI UX designers to customise them to fit your brand identity and target audience.

Many mobile app development for BNPL Dubai agencies offer design packages that include user research, wireframing, and basic prototyping for AED 50,000-80,000, compared to AED 150,000+ for completely custom designs. Focus your design budget on critical user journeys like onboarding, payment processing, and account management.

Consider using design systems like Material Design or Apple's Human Interface Guidelines as your foundation, then add custom elements that differentiate your app from competitors.

7. Regulatory Compliance Strategy

Compliance with UAE financial regulations is non-negotiable, but it doesn't have to break your budget. Instead of hiring expensive legal firms from the start, begin with thorough research of existing regulations and successful BNPL companies' compliance strategies.

Consider partnering with fintech-focused legal advisors who understand the cost to develop a BNPL app like Tabby and can provide practical, cost-effective compliance guidance. Many offer fixed-fee packages for startup compliance reviews, which can save 30-50% compared to traditional hourly billing.

Hidden Costs of BNPL App Development Like Tabby

When entrepreneurs ask about the cost to develop a BNPL app like Tabby, they typically focus on the obvious expenses: development team salaries, basic infrastructure, and initial compliance requirements. However, the real financial challenge lies in the hidden costs that can inflate your custom BNPL app development cost in Dubai by 40-60% beyond initial estimates.

These unexpected expenses have caught many fintech startups off guard, turning what seemed like a manageable Tabby app development cost into a budget-busting nightmare.

Understanding these hidden costs upfront is crucial for anyone serious about Tabby-like app development Dubai projects. Let's dive into the often-overlooked expenses that can make or break your BNPL venture in the UAE's competitive fintech landscape.

1. Ongoing Maintenance and Technical Debt

The biggest shock for most entrepreneurs comes after launch when they discover that building the app was just the beginning. A successful BNPL platform requires constant maintenance, security updates, and feature enhancements to remain competitive against established players like Tabby.

Annual maintenance typically consumes 20-25% of your initial cost to develop a BNPL app in Dubai, which means if you spent AED 400,000 on development, expect to pay AED 80,000-100,000 annually just to keep your app running smoothly. This includes server maintenance, bug fixes, security patches, and compliance updates as UAE regulations evolve.

The challenge intensifies when you consider that mobile app development for BNPL Dubai requires constant adaptation to iOS and Android updates, payment gateway changes, and emerging security threats. Many startups underestimate these Tabby app development costs, leading to technical debt that becomes increasingly expensive to resolve.

2. Third-Party Integration and API Fees

Building a scalable tech stack for BNPL platforms means relying heavily on third-party services, each with its own pricing structure that can quickly add up. Payment processing fees alone can consume 2-4% of every transaction, while additional services create a complex web of recurring expenses.

Credit scoring APIs from providers like Experian or local UAE credit bureaus can cost AED 8,000-15,000 monthly for high-volume operations. SMS and email notification services, essential for payment reminders and account updates, typically run AED 2,000-5,000 monthly. Identity verification services, crucial for KYC compliance, add another AED 3,000-8,000 to monthly operational costs.

When planning your cost of MVP for the BNPL app Dubai, factor in AED 15,000-30,000 monthly for essential third-party services once you reach moderate transaction volumes. These costs scale with your success, meaning higher user engagement directly translates to higher operational expenses.

3. Regulatory Compliance and Legal Oversight

The UAE's financial regulatory environment is constantly evolving, and staying compliant requires ongoing legal and compliance investments that many entrepreneurs overlook when calculating custom BNPL app development costs in Dubai. Initial compliance setup is just the tip of the iceberg.

Annual compliance audits, required for maintaining your financial services license, typically cost AED 25,000-50,000, depending on your app's complexity and transaction volume. Legal reviews for terms of service updates, privacy policy changes, and new feature compliance can add another AED 15,000-30,000 annually.

The Central Bank of UAE regularly updates regulations affecting BNPL operators, requiring immediate compliance adjustments that can cost AED 10,000-25,000 per major regulatory change. These aren't optional expenses – they're mandatory for continued operation in Dubai's regulated fintech environment.

4. Customer Acquisition and Marketing Warfare

Competing with Tabby's established market presence requires substantial marketing investment that extends far beyond initial app store optimization. The cost to develop a BNPL app like Tabby must include realistic customer acquisition costs, which can be surprisingly high in Dubai's competitive market.

Digital marketing campaigns targeting UAE consumers typically cost AED 15-25 per acquired user, while conversion rates for financial apps average 2-4%. This means acquiring 10,000 active users might require AED 150,000-250,000 in marketing spend, not including influencer partnerships, content creation, and brand-building activities.

Merchant acquisition presents another hidden cost challenge. Convincing retailers to integrate your BNPL solution requires dedicated sales teams, technical support, and often revenue-sharing agreements that reduce profitability. Budget AED 5,000-15,000 per major merchant integration, including technical setup and ongoing support.

5. Advanced Security and Fraud Prevention

Financial apps face constant security threats, making advanced fraud prevention systems a necessity rather than a luxury. While basic security measures are included in initial development costs, sophisticated fraud detection systems represent a significant ongoing expense.

Machine learning-based fraud detection platforms typically cost AED 8,000-20,000 monthly, depending on transaction volume and complexity. Regular security audits, required for maintaining customer trust and regulatory compliance, add AED 20,000-40,000 annually to operational costs.

Cybersecurity insurance, essential for protecting against data breaches and fraud losses, can cost AED 15,000-35,000 annually for a mid-sized BNPL operation. These expenses are often overlooked when calculating mobile app development for BNPL Dubai budgets but become critical as your platform grows.

6. Scalability Infrastructure Costs

Success brings its own financial challenges. As your user base grows, infrastructure costs can escalate rapidly beyond initial projections. A scalable tech stack for BNPL platforms requires careful planning for unexpected growth spurts and seasonal traffic variations.

Cloud hosting costs can jump from AED 5,000 monthly for a startup to AED 25,000-50,000 monthly as transaction volumes increase. Database scaling, essential for handling millions of payment calculations and user interactions, often requires expensive enterprise solutions that weren't included in the initial Tabby app development cost estimates.

Content delivery networks (CDNs), load balancers, and backup systems become essential as your app gains popularity, adding AED 8,000-20,000 monthly to operational costs. These infrastructure investments are crucial for maintaining the performance standards that users expect from financial applications.

7. Talent Retention and Team Expansion

Building a successful BNPL platform requires retaining top talent in Dubai's competitive fintech job market. Initial development costs often assume current team salaries, but market rates for experienced fintech developers increase rapidly, especially for those with UAE regulatory experience.

Annual salary increases for key technical team members typically range 15-25% in Dubai's fintech sector, while hiring additional developers for new features and maintenance can cost AED 120,000-200,000 annually per senior developer. These human resource costs compound over time, significantly impacting long-term project budgets.

Specialized roles like compliance officers, risk analysts, and fraud prevention specialists become necessary as your platform grows, each commanding salaries of AED 150,000-300,000 annually. These positions weren't needed during initial development, but have become essential for continued operation and growth.

8. Digital Wallet Integration Complexity

Modern consumers expect seamless integration with digital wallets and alternative payment methods. The cost to build a digital wallet app like Payit integration adds complexity that many BNPL startups underestimate. Each wallet integration requires custom development, testing, and ongoing maintenance.

Supporting popular wallets like Apple Pay, Google Pay, Samsung Pay, and local options like Payit typically costs AED 15,000-30,000 per integration, with ongoing maintenance fees of AED 2,000-5,000 monthly per wallet. These integrations are essential for user convenience but represent hidden costs of BNPL app development that impact overall project budgets.

How to Make Your BNPL App Superior to Tabby: Outshining the Competition in Dubai's Fintech Arena

Creating a BNPL app that surpasses Tabby in Dubai's competitive fintech landscape requires understanding what makes competitors tick and where opportunities for innovation lie. While Tabby dominates with 3+ million users across the UAE, there's still room to carve out a superior position with the right strategy.

1. Hyper-Personalized Credit Limits

While Tabby offers standard credit assessments, your app can implement dynamic, behavior-based credit scoring that adjusts limits based on seasonal spending, salary increases, or life events. Imagine a system that automatically increases a user's limit during Ramadan shopping or before back-to-school season – this level of personalization requires sophisticated Tabby-like app development in Dubai but creates genuine user value.

2. Community-Driven Financial Wellness

Go beyond Tabby's basic spending insights by creating a social financial wellness platform. Users can join spending challenges, share budgeting tips, and earn rewards for responsible payment behavior. This gamification approach transforms BNPL from a mere payment tool into a financial education platform – something no current competitor offers comprehensively.

3. Micro-Investment Integration

While users wait between payments, offer them the opportunity to invest spare change or earn interest on their account balance. This feature turns your BNPL platform into a wealth-building tool, directly addressing the criticism that BNPL apps don't help users build long-term financial health.

4. Advanced Merchant Benefits

Tabby charges merchants 2-4% per transaction. Offer dynamic pricing based on merchant performance, exclusive early payment options, or revenue-sharing models for high-performing partners. Create a merchant loyalty program that reduces fees as transaction volumes increase – this approach can help secure better partnerships while improving your BNPL app development cost in the Dubai ROI.

5. Cultural Localization Beyond Language

While Tabby offers Arabic language support, true cultural localization means understanding UAE shopping patterns, Islamic finance principles, and local celebration periods. Implement Sharia-compliant payment structures, special Eid shopping features, and UAE National Day promotional tools that resonate with local values.

Tips for Market Domination:

Focus on underserved segments Tabby hasn't fully captured – students, expatriate communities, or specific age demographics. The cost to develop a BNPL app like Tabby may seem high initially, but targeting niche markets can provide faster user acquisition and stronger brand loyalty before expanding to mass market competition.

How to Make Money from Your BNPL App Like Tabby: Revenue Streams That Actually Work

Building a sustainable BNPL business model requires diversifying beyond simple merchant fees. Tabby's success comes from multiple revenue streams, but there's room for innovation in monetization strategies that benefit all stakeholders.

1. Merchant Transaction Fees (40-50% of revenue)

The bread and butter of BNPL platforms involves charging merchants 2-6% per transaction. However, smart mobile app development for BNPL Dubai strategies implement tiered pricing: premium merchants pay higher fees for exclusive features like priority customer support, advanced analytics, or marketing co-op opportunities. Volume-based discounts encourage larger merchants while maintaining profitability on smaller transactions.

2. Late Payment and Processing Fees (25-30% of revenue)

While controversial, responsible late fee structures provide essential revenue. Unlike traditional lenders charging 25-40% APR, successful BNPL apps charge modest late fees ($5-25 AED) that encourage timely payments without creating debt traps. The key is transparency – users should understand exact fee structures before agreeing to payment plans.

3. Premium User Subscriptions (10-15% of revenue)

Tabby offers basic services free, but there's opportunity for premium tiers. Consider subscription models offering higher credit limits, exclusive merchant access, priority customer support, or financial wellness tools. A premium subscription at AED 25-50 monthly can significantly boost user lifetime value while providing genuine additional benefits.

4. Financial Product Cross-Selling

Partner with banks, insurance companies, and investment platforms to offer complementary financial products. Commission-based referrals for personal loans, credit cards, or investment accounts can generate AED 100-500 per successful referral. Users already trust your platform with payments, making them more likely to consider related financial services.

5. Affiliate Marketing and Sponsored Placements

Your app's shopping discovery feature becomes prime real estate for sponsored product placements and affiliate commissions. Merchants pay for prominent placement in search results, category features, or personalized recommendations. This revenue stream grows naturally as your user base expands, improving the long-term cost to develop a BNPL app like Tabby investment returns.

6. White-Label Platform Licensing

Once your platform proves successful, license the technology to banks, retailers, or other fintech companies wanting BNPL capabilities. This B2B2C approach provides recurring licensing revenue while expanding market reach without direct competition.

7. Data Analytics and Insights Sales

Anonymized spending data provides valuable market insights for brands and retailers. Fashion brands want to understand purchasing patterns, electronics retailers need seasonal demand forecasting, and consumer goods companies require demographic analysis. This B2B revenue stream can generate substantial income without impacting user experience – something often overlooked when calculating Tabby-like app development in Dubai profitability projections.

Revenue Optimization Tips:

Balance user experience with monetization – aggressive fee structures might provide short-term revenue, but damage long-term user retention. The most successful BNPL app development cost in Dubai calculations factor in customer lifetime value rather than immediate transaction profits. Focus on features that increase user engagement and transaction frequency rather than maximizing individual transaction margins.

How to Build an App Like Tabby Successfully: Your Complete Development Roadmap

Successfully launching a BNPL app in Dubai's competitive market requires more than just copying Tabby's features – it demands strategic planning, regulatory understanding, and flawless execution. Here's your comprehensive roadmap to building a market-competitive platform.

Phase 1: Strategic Foundation and Market Research (Months 1-2)

Before writing a single line of code, understand Dubai's unique fintech ecosystem. Tabby succeeded by deeply understanding local shopping habits, payment preferences, and regulatory requirements. Your mobile app development for BNPL Dubai project needs similar market intelligence.

Conduct extensive user interviews with potential customers from different demographics – UAE nationals, long-term expats, and recent arrivals have vastly different financial behaviors and preferences. Map competitor strengths and weaknesses: Tabby excels at merchant partnerships but lacks advanced financial wellness features; Postpay focuses on smaller transactions but has limited credit assessment capabilities.

Phase 2: Regulatory Compliance and Legal Framework (Months 2-3)

Dubai's fintech regulations aren't suggestions – they're mandatory requirements that can shut down non-compliant platforms. Engage with the Central Bank of UAE (CBUAE) early in your Tabby-like app development in Dubai process to understand licensing requirements, capital adequacy rules, and operational guidelines.

Establish relationships with legal experts specializing in UAE financial services law. Your platform must comply with consumer protection regulations, data privacy laws, and Islamic finance principles where applicable. This legal groundwork significantly impacts your cost to develop a BNPL app like Tabby, but cutting corners here risks catastrophic compliance issues later.

Phase 3: Technical Architecture and Development (Months 3-8)

Backend Infrastructure: Build for scale from day one. Tabby processes thousands of transactions daily across multiple merchants – your system architecture must handle similar volumes without performance degradation. Implement microservices architecture allowing independent scaling of payment processing, user management, and merchant services.

Choose cloud infrastructure supporting UAE data residency requirements while providing global scalability. AWS, Microsoft Azure, and Google Cloud all offer UAE-based data centers essential for regulatory compliance.

Security Implementation: Financial apps face constant security threats. Implement end-to-end encryption, multi-factor authentication, and real-time fraud detection from launch. Regular penetration testing and security audits aren't optional – they're survival requirements in Dubai's regulated environment.

Phase 4: Merchant Partnership Development (Months 6-9)

Tabby's success stems largely from extensive merchant partnerships. Start building relationships with local retailers, e-commerce platforms, and service providers before your app launches. The BNPL app development cost in Dubai should include substantial partnership development budgets – successful platforms invest 15-20% of development costs in merchant acquisition and integration.

Create compelling merchant value propositions beyond payment processing. Offer advanced analytics, customer insights, and marketing support that traditional payment processors don't provide. Develop integration tools making it easy for merchants to add BNPL options to existing checkout processes.

Phase 5: User Acquisition and Market Launch (Months 9-12)

Launch with a focused user acquisition strategy targeting specific demographics where you can provide superior value. Rather than competing directly with Tabby's mass market approach, consider focusing on underserved segments – students, specific expatriate communities, or particular age groups.

Implement referral programs, strategic partnerships with employers or universities, and targeted digital marketing campaigns. Track user acquisition costs carefully – sustainable BNPL platforms maintain customer acquisition costs below 10% of user lifetime value.

Conclusion: Building a BNPL App Like Tabby with VLink

Building a BNPL app like Tabby in Dubai represents a golden opportunity to tap into the UAE's rapidly expanding fintech ecosystem, where digital payment adoption is surging and consumer demand for flexible payment solutions continues to grow exponentially. The cost to develop a BNPL app like Tabby varies significantly based on your feature requirements and market ambitions, ranging from AED 180,000-350,000 for a robust MVP to AED 500,000-800,000 for a comprehensive platform with advanced AI credit scoring, multi-merchant integrations, and enterprise-grade security features.

Understanding the complete financial picture – including the often-overlooked hidden costs that can inflate your BNPL app development cost in Dubai by 40-60% – is crucial for long-term success. From ongoing compliance requirements and third-party API fees to customer acquisition costs and scalability infrastructure, these expenses can make or break your fintech venture if not properly planned for from the outset.

Partnering with an experienced BNPL app development agency Dubai like VLink ensures you're building on a foundation of local market expertise, regulatory compliance knowledge, and proven fintech development capabilities. Our team understands the nuances of Dubai's financial landscape, from Central Bank of UAE regulations to Sharia-compliant payment structures, giving your app the competitive edge needed to challenge established players like Tabby. Contact us today!

Global Delivery Manager, VLink Inc.

Shivisha Patel serves as the Global Delivery Manager at VLink Inc., bringing a wealth of experience in program delivery and management, particularly in the insurance and banking sectors. She has a robust technical background with deep expertise in WebSphere MQ, WTX, IIB, middleware, and enterprise system integration.

Shivisha Patel

Shivisha Patel