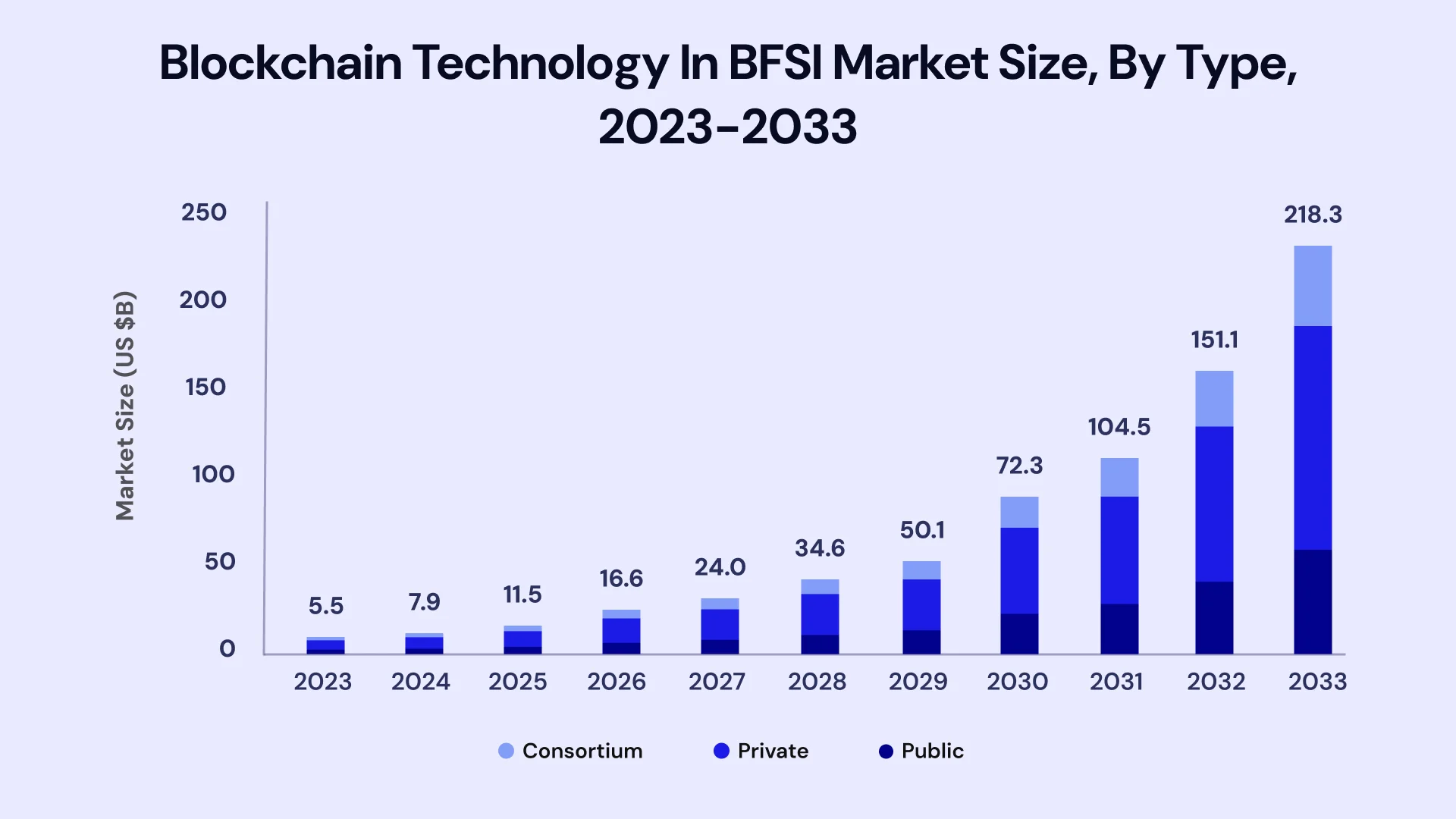

Blockchain technology has emerged as a transformative force in various industries, and the banking sector is no exception. The Global Blockchain in BFSI (Banking, Financial Services, and Insurance) Market is projected to grow from USD 5.5 Billion in 2023 to USD 218.3 Billion by 2033, at a CAGR of 44.5%.

With its promise of enhanced security, transparency, and efficiency, blockchain presents many opportunities for banks to innovate and improve their operations. But the path to integrating blockchain into the banking ecosystem is fraught with challenges.

In this blog, we'll explore the key opportunities and challenges associated with blockchain in banking, examine its use cases, review real-world examples, and discuss the future of this groundbreaking technology.

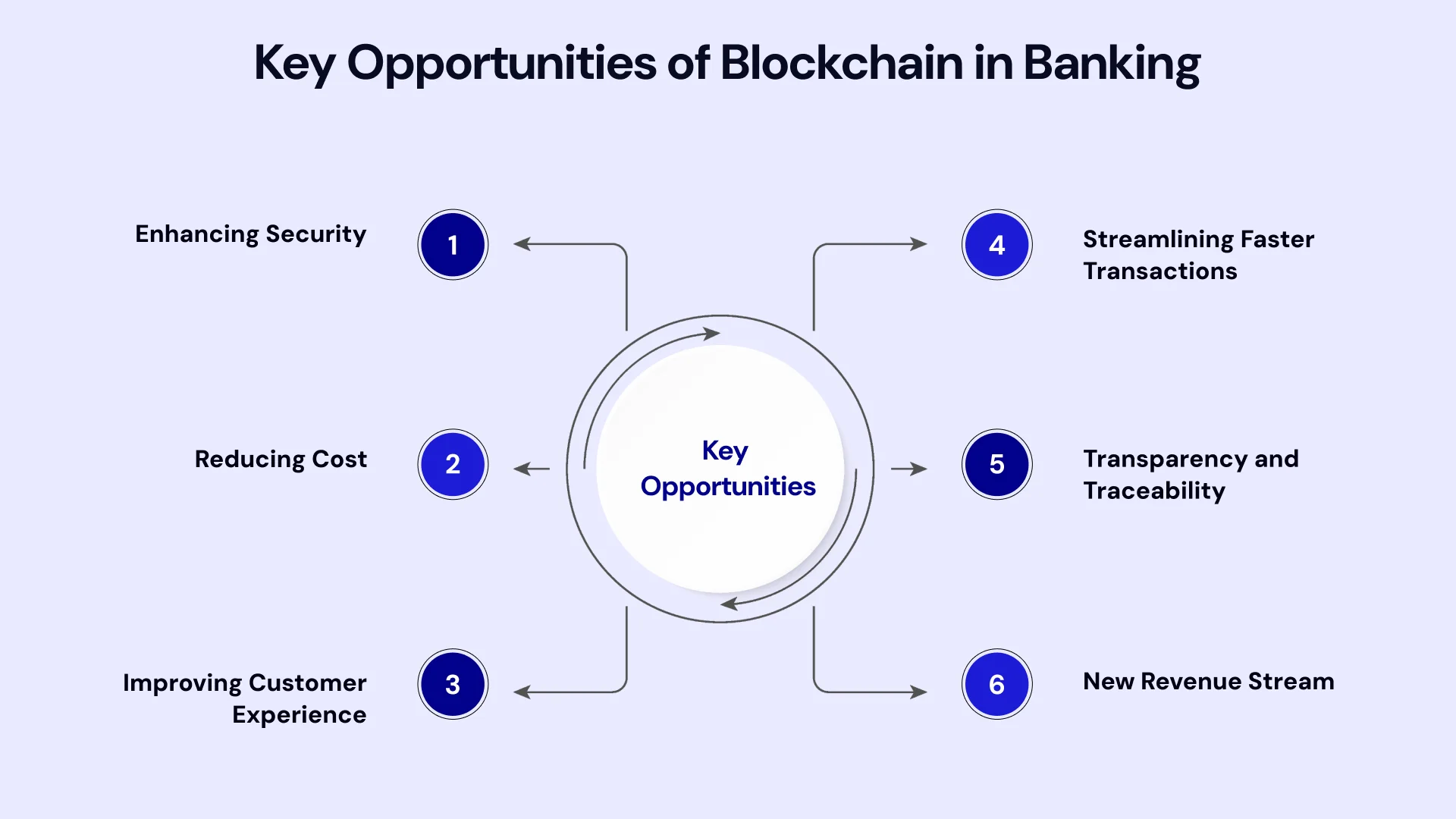

Key Opportunities of Blockchain for the Banking Sector

Implementing Blockchain offers several key opportunities to the banking sector with a competitive edge:

#1 - Enhanced Security

Banks often encounter technical glitches, cyberattacks, and human errors that put users’ data at risk. Blockchain's decentralized nature ensures higher security, reducing the risk of fraud and cyberattacks.

Transactions are encrypted and linked to previous transactions, making it difficult for malicious entities to alter data. Smart contracts, under the latest blockchain trends, also offer automated transactions, adding another layer of security.

#2 - Faster Transactions

Traditional banking transactions, especially cross-border ones, can take days to settle. Blockchain facilitates real-time transactions, improving cash flow and reducing delays in the payment process.

Banks can now bypass intermediaries, enabling customers to complete transactions more quickly. This improvement allows both customers and banks to handle and process a higher volume of transactions efficiently.

#3 - Cost Reduction

By eliminating intermediaries, blockchain reduces transaction costs, leading to significant savings for businesses. Smart contracts also automate processes, minimizing the need for manual intervention and further cutting costs.

Banks can also lower transaction costs for interbank transactions.

#4 - Transparency and Traceability

Banks will also benefit from blockchain with transparency and traceability. Blockchain provides an immutable record of all transactions, enhancing transparency. This traceability is crucial for businesses in regulated industries, ensuring compliance with legal and regulatory standards.

It means banks can detect suspicious transactions and streamline auditing processes more effectively. Financial industry and fintech firms can now offer easily accessible digital information, save time and simplifying the auditing process.

#5 - Improved Customer Experience

By leveraging blockchain, banks can streamline and expedite processes that traditionally involve lengthy procedures.

For example, blockchain simplifies loan approvals by providing transparent, immutable records of creditworthiness. Identity verification becomes more efficient with blockchain’s decentralized and secure digital identity solutions.

Payment processes are accelerated, reducing transaction times from days to minutes. These enhancements contribute to a more seamless and user-friendly banking experience, leading to higher customer satisfaction and increased loyalty.

#6 - New Revenue Stream

Blockchain technology fosters the development of innovative financial products, such as decentralized finance (DeFi) solutions. These platforms offer services like lending, borrowing, and trading without traditional intermediaries, creating new revenue streams for financial institutions.

Additionally, blockchain enables the creation of tokenized assets and digital currencies, expanding investment opportunities and potentially increasing profitability.

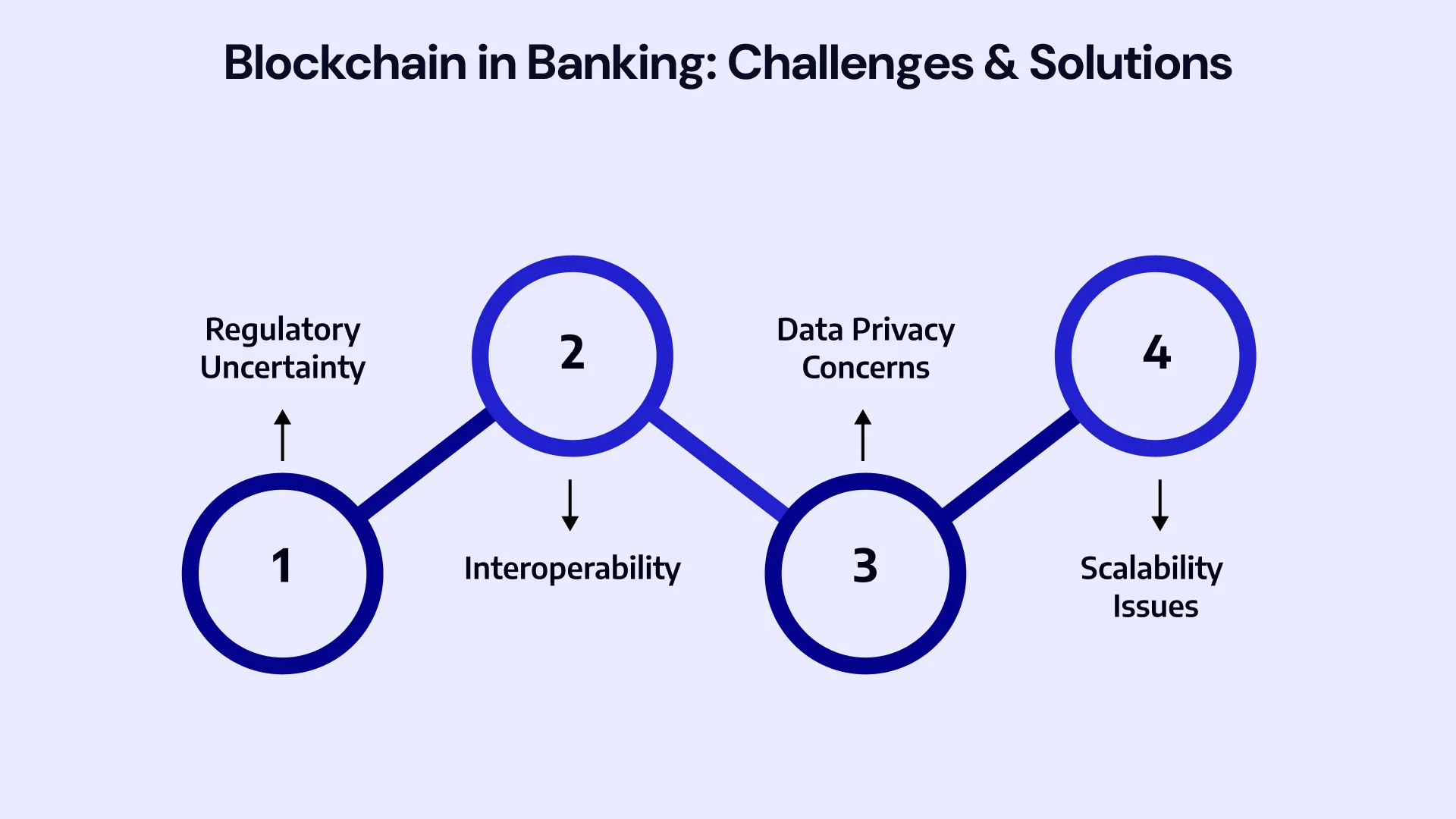

Challenges in Implementing Blockchain Within the Banking Ecosystem

Blockchain technology has the potential to revolutionize the banking industry by enhancing security, transparency, and efficiency. But, its integration into banking systems comes with several challenges. So, it’s essential to select the best blockchain solution for your bank.

Here are the main five challenges of implementing blockchain in banking and providing solutions to overcome them.

Challenge #1 - Regulatory Uncertainty

One of the biggest hurdles for blockchain in banking is the lack of clear and consistent regulations. Different countries have varying legal frameworks, making it difficult for banks to adopt blockchain technology across borders. The absence of standardized regulations creates uncertainty, which can hinder investment and innovation.

Solution:

Banks can collaborate with regulators, policymakers, and industry stakeholders to create a cohesive regulatory framework. Establishing a global standard for blockchain regulations can help banks confidently adopt the technology. Additionally, banks should stay informed about regulatory changes and be proactive in compliance to mitigate risks.

Challenge #2 - Interoperability

The banking industry relies on a complex network of systems and platforms, many of which are not compatible with blockchain technology. The lack of interoperability between traditional banking systems and blockchain networks can create friction, leading to inefficiencies and higher operational costs.

Solution:

Adopting standardized protocols and APIs can facilitate interoperability between blockchain and legacy systems. Banks can also participate in industry consortia that focus on creating interoperable blockchain solutions. In addition, investing in middleware solutions that bridge the gap between different systems can help banks integrate blockchain more seamlessly.

Challenge #3 - Data Privacy Concerns

While blockchain is known for its transparency, this feature can also be a drawback in the banking sector, where data privacy is paramount. The immutable characteristic of blockchain ensures that once data is recorded, it cannot be changed or erased. This permanence can sometimes clash with data privacy regulations such as GDPR.

Solution:

Banks can implement permissioned blockchain networks where access to sensitive information is restricted to authorized parties. Zero-knowledge proofs and other cryptographic techniques can be used to protect sensitive data while still maintaining the transparency benefits of blockchain.

In addition, banks should work closely with legal experts to ensure their blockchain implementations comply with data privacy laws.

Challenge #4 - Scalability Issues

Blockchain networks, particularly public ones, struggle with scalability. As the number of transactions increases, the system can become slow and inefficient. This limitation is a significant concern for banks, which require high-speed transaction processing to handle large volumes of data.

Solution:

Banks can explore hybrid blockchain solutions that combine the benefits of both public and private blockchains. Implementing Layer 2 scaling solutions, such as off-chain transactions and sharding, can also enhance the scalability of blockchain networks.

Additionally, banks can collaborate with blockchain developers to innovate new technologies that address scalability concerns.

Note: Businesses evaluating Challenges in Implementing Blockchain Within the Banking Ecosystem should also consider selecting the best blockchain solution for your bank to improve execution quality, scalability, and long-term operational resilience.

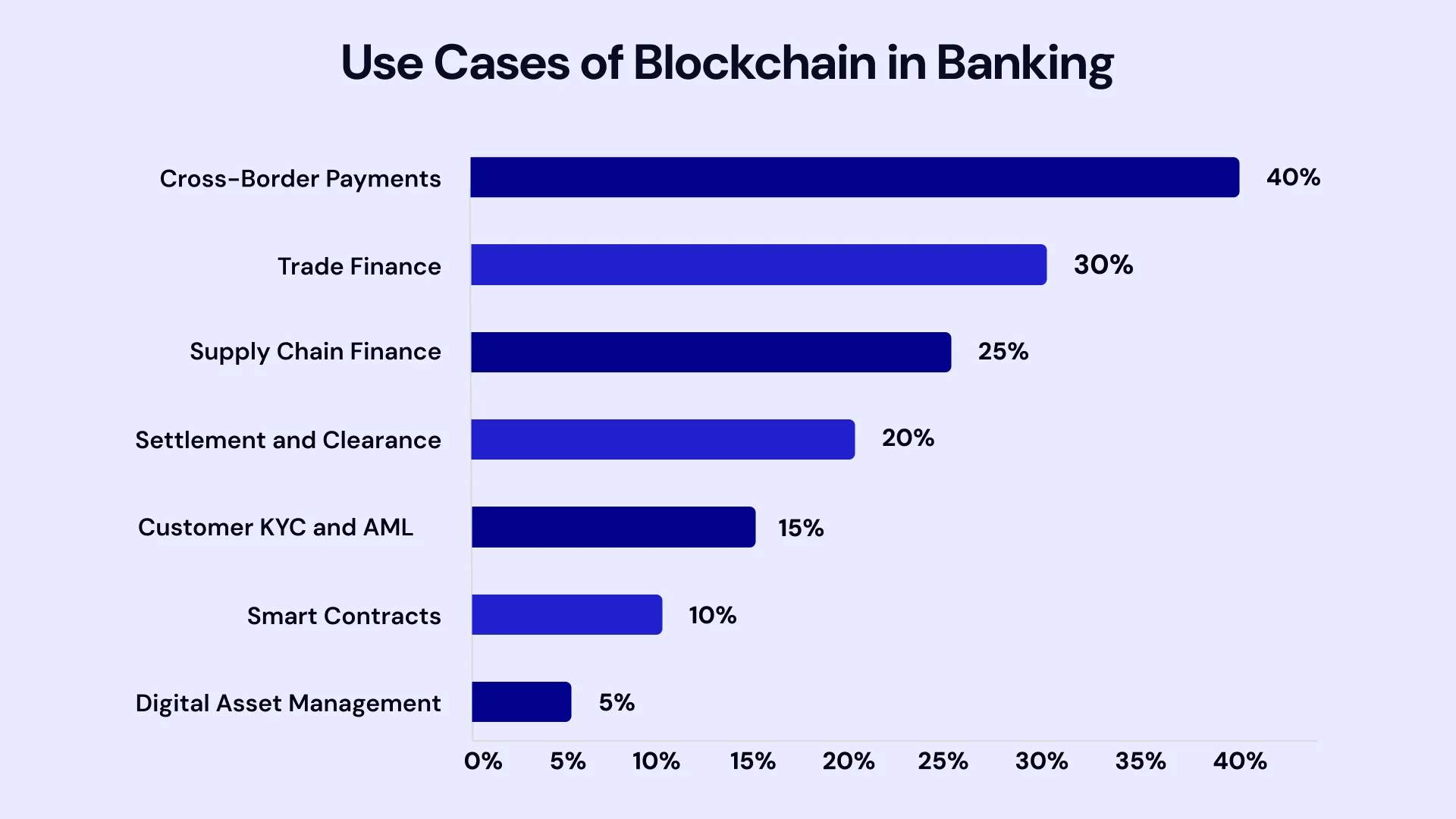

Different Use Cases of Blockchain in Banking

Here's a look at some of the key use cases of blockchain in banking:

Use Case #1 - Cross-Border Payments

Cross-border payments have traditionally been slow, and prone to errors. Blockchain revolutionizes this by enabling real-time, secure, and low-cost transactions across borders.

By eliminating the need for intermediaries, blockchain reduces transaction times from days to minutes and significantly lowers fees. Banks can also offer enhanced transparency, allowing customers to track their payments in real-time.

Use Case #2 - Trade Finance

Trade finance involves complex processes and multiple intermediaries, often leading to delays and increased costs. You can build a blockchain app to simplify trade finance by digitizing the entire process, from issuing letters of credit to verifying shipping documents.

Smart contracts automate these processes, reducing the risk of fraud and errors and ensuring that transactions are completed faster and more securely.

Use Case #3 - Supply Chain Finance

Supply chain services in finance involves multiple parties, including suppliers, manufacturers, and financial institutions. Blockchain provides a transparent and immutable record of all transactions within the supply chain, ensuring that all parties have access to the same information.

This transparency reduces disputes, enhances trust, and enables faster financing decisions, as banks can easily verify the authenticity of transactions.

Use Case #4 - Smart Contracts

In banking, smart contracts can automate various processes, such as loan agreements, insurance claims, and compliance checks.

By executing automatically when predefined conditions are met, smart contracts reduce the need for intermediaries, lower operational costs, and minimize the risk of human error or fraud.

Use Case #5 - Customer KYC and AML

Know Your Customer (KYC) and Anti-Money Laundering (AML) regulations are crucial for preventing financial crimes but can be time-consuming and costly for banks. Blockchain streamlines KYC and AML processes by allowing secure, decentralized storage of customer information.

Banks can share verified customer data on a blockchain network, reducing duplication of efforts and ensuring compliance while enhancing customer onboarding efficiency.

Use Case #6 - Settlement and Clearance

The settlement and clearance of financial transactions can take several days, involving multiple intermediaries and increasing the risk of errors. Blockchain enables near-instantaneous settlement and clearance by providing a single, shared ledger that all parties can access.

It reduces the time and cost associated with traditional settlement processes and minimizes the risk of discrepancies or fraud.

Use Case #7 - Digital Asset Management

Blockchain provides a secure and transparent platform for managing digital assets, such as cryptocurrencies, tokens, and other digital securities. Banks can offer digital asset custody services, enabling customers to store and manage their assets securely.

Blockchain’s immutability ensures that digital assets are protected from tampering or unauthorized access, providing customers with greater confidence in the security of their investments.

Use Case #8 - Loan Syndication

Loan syndication involves multiple lenders coming together to finance a single borrower. The process can be complex and time-consuming, requiring extensive coordination between the parties involved. Blockchain simplifies loan syndication by providing a single platform for all parties to collaborate and share information.

Smart contracts can automate the distribution of funds, interest payments, and other loan-related activities, reducing the administrative burden and enhancing transparency.

Real-World Examples of Implementing Blockchain in Banks

Here are real-world examples of how blockchain is being implemented in the banking sector.

JPMorgan Chase: Interbank Information Network (IIN)

JPMorgan Chase, one of the largest banks in the United States, has developed the Interbank Information Network (IIN) on its proprietary blockchain platform, Quorum. The IIN aims to solve the issues of interbank payments by reducing delays and ensuring secure and transparent information exchange between banks.

More than 400 banks globally are part of the network, benefiting from faster processing times and reduced fraud risks.

HSBC: Digital Vault

HSBC has implemented blockchain in its Digital Vault, a platform designed to digitize and store records of private investments. By using blockchain, HSBC can offer clients secure and instant access to their investment records, reducing the time and cost associated with manual processes.

This innovation has also enhanced the transparency and security of asset ownership records.

Deutsche Bank: Blockchain in Trade Finance

Deutsche Bank has been exploring blockchain solutions for trade finance, mainly through its participation in the Marco Polo Network. This network uses blockchain to digitize the trade finance process, making it more efficient, transparent, and secure.

By reducing the reliance on paper-based documentation, Deutsche Bank has streamlined trade transactions, cut costs, and mitigated risks.

Wells Fargo: Blockchain for International Payments

Wells Fargo has been exploring the use of blockchain for international payments, focusing on reducing the time and cost of cross-border transactions. The bank has conducted successful pilot programs using blockchain to settle payments between its branches in different countries, demonstrating the potential for blockchain to revolutionize global financial transactions.

Barclays: Blockchain for Compliance

Barclays has been using blockchain technology to streamline compliance processes, particularly in the area of know-your-customer (KYC) and anti-money laundering (AML) regulations. By implementing blockchain, Barclays can securely and efficiently verify the identities of clients and monitor transactions in real time, reducing the risk of financial crime and ensuring regulatory compliance.

Future of Blockchain in Banking

The future of blockchain in banking is promising, with ongoing advancements and increasing adoption. As blockchain technology continues to advance in the banking and finance sectors, we can expect a notable rise in Central Bank Digital Currencies (CBDCs). These digital currencies will facilitate faster transactions and promote greater financial inclusion.

Also, the adoption of enhanced security features, such as zero-knowledge proofs and smart contracts, will bolster the protection of customer data and transactions while ensuring compliance with industry regulations like GDPR and PCI-DSS.

Additionally, the growth of decentralized finance (DeFi) platforms, blockchain wallets, and asset tokenization will create new opportunities for liquidity and investment. This evolution will drive banks to embrace innovation, improve efficiency, and enhance financial accessibility.

Elevate Your Blockchain Experience in Banking with VLink!

At VLink, we specialize in helping businesses navigate the complexities of blockchain technology. Our expertise can assist you in implementing innovative blockchain development solutions tailored to your needs.

Whether you're looking to implement blockchain for payments, trade finance, or digital identity verification, VLink has the expertise to guide you through every step of the process.

Contact us today to elevate your blockchain experience in banking!

Global Delivery Manager, VLink Inc.

Shivisha Patel serves as the Global Delivery Manager at VLink Inc., bringing a wealth of experience in program delivery and management, particularly in the insurance and banking sectors. She has a robust technical background with deep expertise in WebSphere MQ, WTX, IIB, middleware, and enterprise system integration.

Shivisha Patel

Shivisha Patel