This is where IBM Integration Bus (IIB) and IBM MQ emerge as gamechangers.

For IT Heads and technology decision-makers in Indian banks and Public Sector Units (PSUs), implementing robust IIB/MQ integration isn't just about connecting systems—it's about building a resilient, scalable, and secure foundation that can support everything from real-time payment processing to regulatory compliance initiatives like the Reserve Bank of India's digital lending guidelines. IIB and MQ enable integration—enterprise IBM integration solutions connect systems across the enterprise.

The stakes are extraordinarily high. A single point of failure in your integration architecture can cascade into transaction delays, data inconsistencies, and compliance violations, eroding customer trust and impacting your bottom line. Yet many Indian banks continue to struggle with fragmented integration landscapes, point-to-point connections that become unmanageable at scale, and middleware configurations that can't handle peak transaction volumes during festival seasons or salary disbursement periods.

IBM Cloud's infrastructure capabilities, combined with IIB/MQ's enterprise-grade messaging and integration features, offer Indian financial institutions a proven pathway to modernization. These technologies have successfully supported major banking transformations across public and private sector banks, enabling them to reduce deployment times from days to hours, improve system availability to 99.99%, and process millions of transactions daily without compromising security or performance.

This comprehensive guide explores the proven best practices, architectural patterns, and strategic considerations that successful Indian banks have leveraged to implement IIB/MQ integration at scale. Whether you're planning a complete legacy system modernization, implementing new digital banking services, or optimizing existing integration workflows, you'll discover actionable insights that address the unique challenges of the Indian banking environment.

Understanding IBM IIB/MQ Integration in Banking

IBM Integration Bus (now evolved into IBM App Connect Enterprise) and IBM MQ form the backbone of enterprise integration for financial institutions worldwide. For Indian banks specifically, these technologies address several critical requirements that are non-negotiable in today’s banking landscape—often implemented and optimized by skilled IBM MQ developers to ensure seamless and resilient system communication.

But what specifically makes the IIB/MQ stack indispensable for the subcontinent’s financial leaders? Let’s dive into the core drivers.

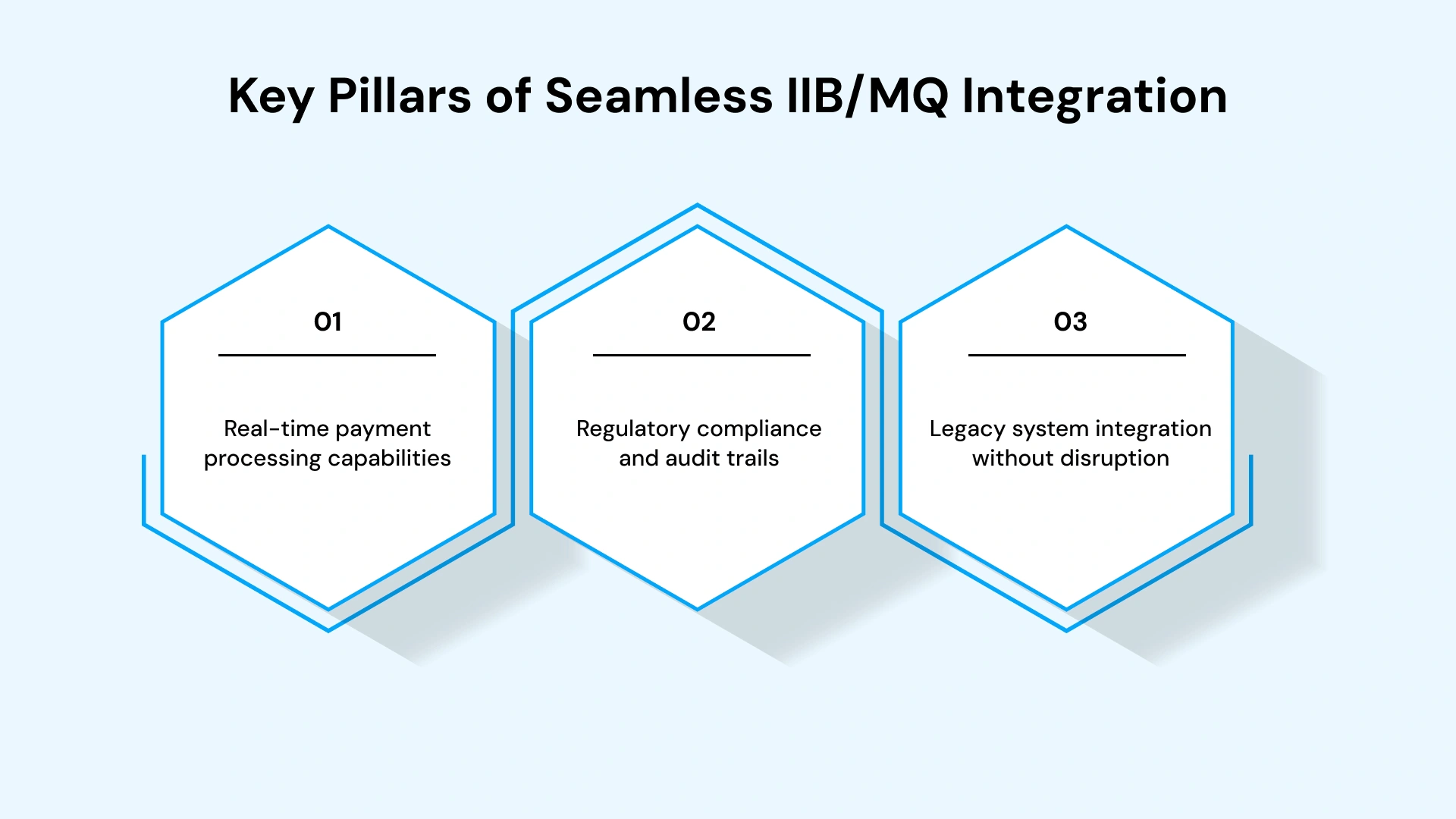

- Real-time payment processing capabilities have become essential with the explosive growth of UPI, IMPS, and NEFT transactions. IBM MQ's guaranteed message delivery ensures that payment instructions never get lost in transit, even during network disruptions. The message queue architecture provides exactly-once delivery semantics, which is crucial when you're moving money between accounts—you can't afford duplicate transactions or lost payment instructions.

- Regulatory compliance and audit trails represent another compelling reason for IIB/MQ adoption. The Reserve Bank of India mandates comprehensive logging and monitoring of all financial transactions.IBM IIB’s built-in audit capabilities automatically capture message flows, transformation details, and system interactions, creating an immutable audit trail that satisfies regulatory requirements. Experienced IBM IIB developers can further configure and optimize these capabilities to align with enterprise-specific compliance and governance needs—without requiring extensive custom development.

- Legacy system integration without disruption addresses perhaps the most pressing concern for Indian banks. Most PSU banks operate core banking systems that are 15-20 years old, running on mainframes or proprietary platforms. Direct modernization carries catastrophic risk. IIB acts as an integration layer, connecting legacy systems to modern applications via standardized interfaces, enabling incremental modernization while maintaining business continuity.

The Architecture of Enterprise-Grade Banking Integration

A well-designed IIB/MQ architecture for banking follows specific patterns that have proven effective across multiple implementations in Indian financial institutions.

- Message-oriented middleware architecture places IBM MQ at the center of all system-to-system communication. Instead of point-to-point connections between applications, all systems communicate through message queues. This decoupling means that if your core banking system needs maintenance, other applications can continue operating, queuing messages that will be processed once the core system returns online. For a bank processing 5 million transactions daily, this architecture prevents cascading failures.

- Enterprise Service Bus implementation leverages IIB to create a centralized integration layer. Your ESB handles message routing, protocol transformation, data mapping, and business rule execution. When a mobile banking app initiates a fund transfer, the ESB routes the request to the core banking system, transforms data formats, validates business rules, logs the transaction for compliance, and routes confirmation messages to all relevant systems—all without the mobile app needing to know anything about your backend infrastructure.

- High availability and disaster recovery configurations are non-negotiable for banking operations. Leading Indian banks implement multi-datacenter IIB/MQ deployments with active-active configurations. If your primary datacenter experiences an outage, message processing automatically fails over to the secondary datacenter within seconds. IBM MQ's clustering capabilities ensure that messages are replicated across locations, guaranteeing zero data loss even during disaster scenarios.

Configuration Management Strategy for Banking Environments

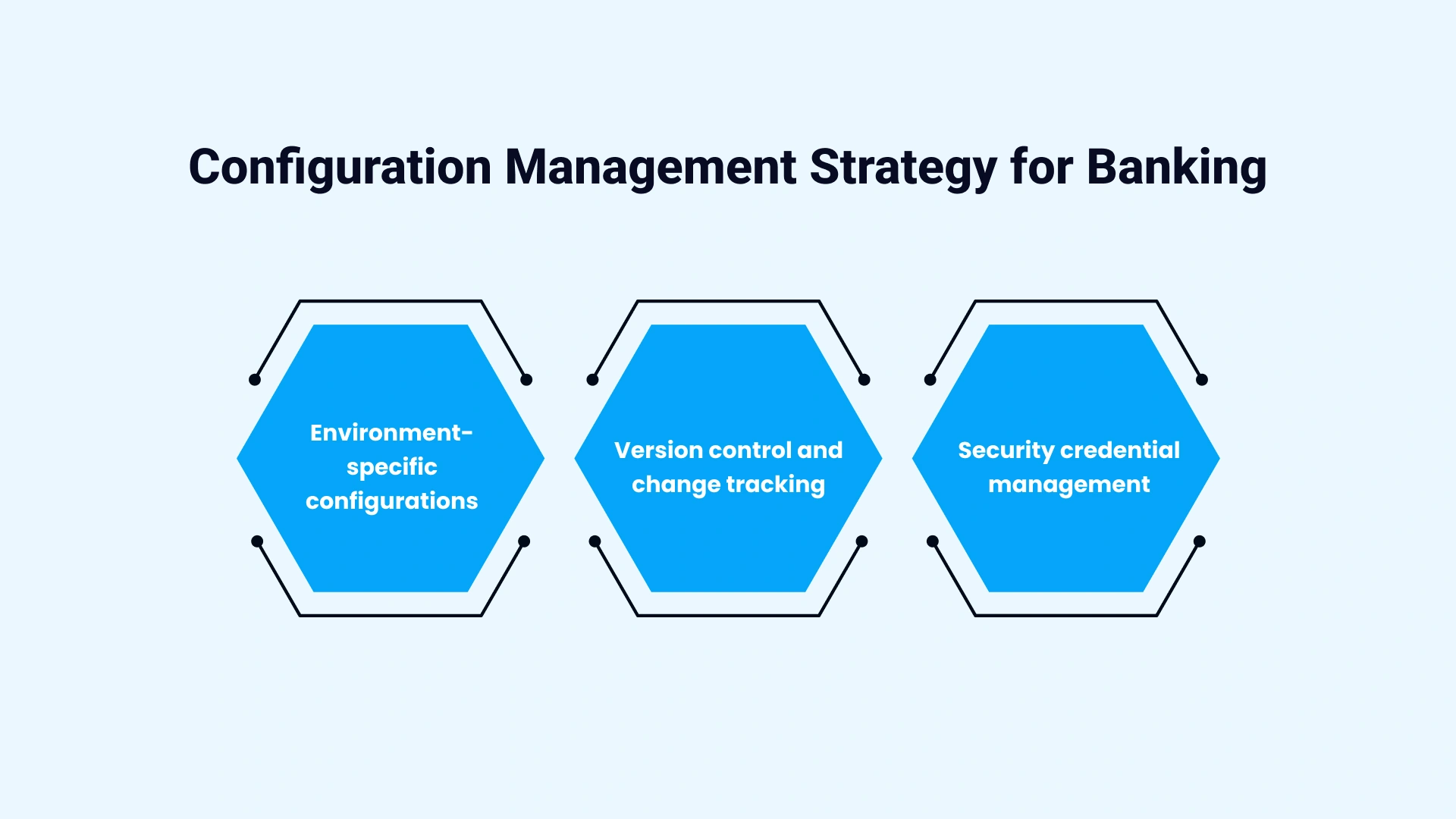

Configuration management separates successful implementations from problematic ones. Indian banks operate under strict change control requirements, making configuration discipline critical.

- Environment-specific configurations must be externalized from your integration flows. Development, UAT, and production environments have different endpoint URLs, credentials, timeout values, and processing rules. By externalizing these configurations into property files or configuration repositories, you enable the same integration code to deploy across environments without modification, reducing deployment errors and accelerating release cycles.

- Version control and change tracking through tools like Git or IBM's Configuration Management provide complete visibility into what changed, when, and by whom. When a production issue occurs at 2 AM during month-end processing, your team can immediately identify recent configuration changes and roll back if necessary. This capability has saved multiple Indian banks from extended outages during critical processing windows.

- Security credential management deserves special attention. Your IIB flows connect to dozens of systems, each of which requires authentication credentials. Hardcoding credentials in integration flows creates security vulnerabilities and operational nightmares when passwords expire. Leading implementations leverage IBM's security exit mechanisms and integration with enterprise key management systems to centralize credential management and enable automated credential rotation.

Critical Best Practices for IBM IIB/MQ Integration in Banking

In the banking sector, where data integrity, regulatory compliance (e.g., PCI-DSS, Basel III), and "always-on" availability are non-negotiable, integrating IBM Integration Bus (IIB/App Connect Enterprise) with IBM MQ requires a specialized set of best practices.

Below is a breakdown of critical strategies organized by operational domain.

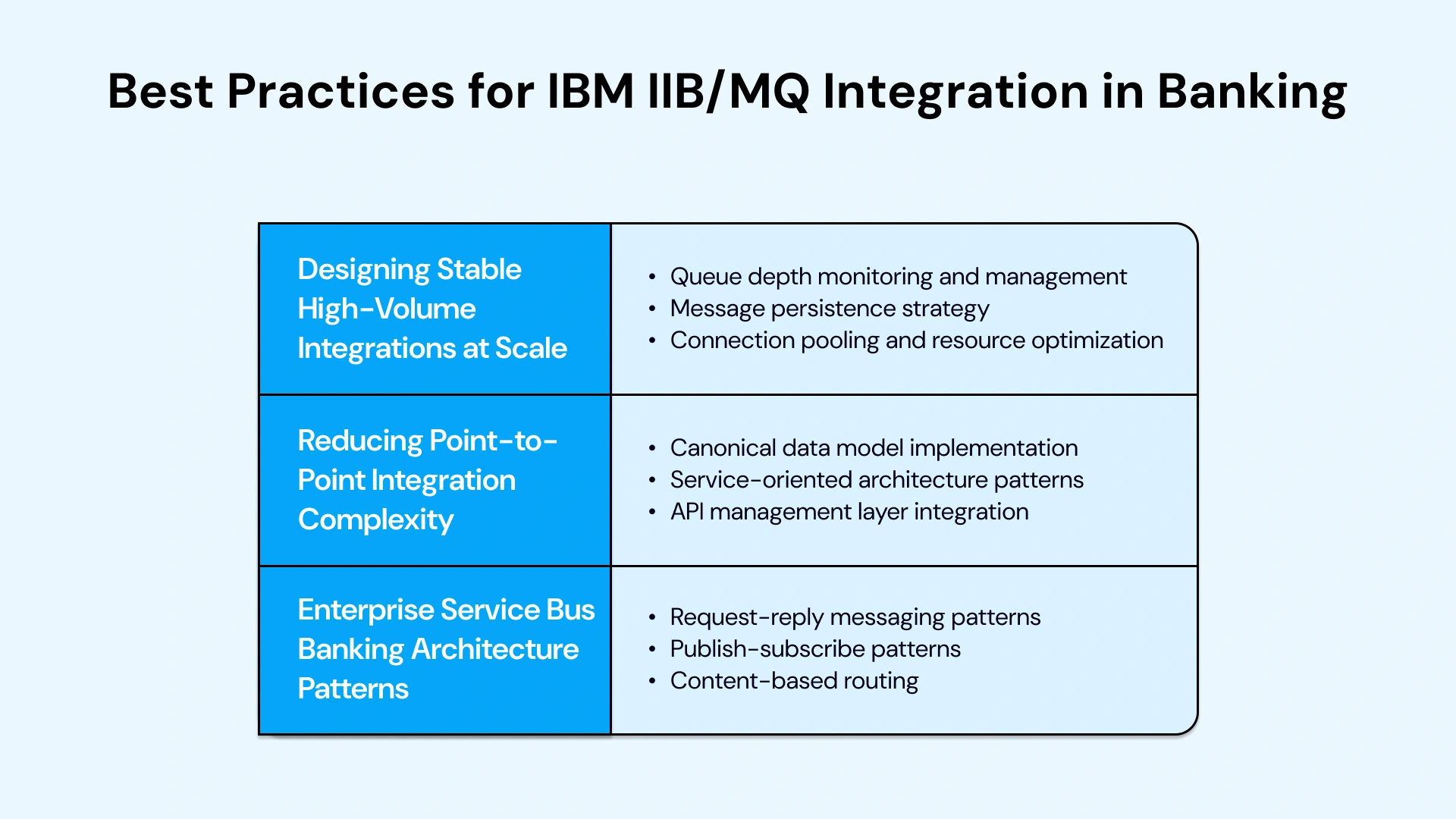

Designing Stable High-Volume Integrations at Scale

Indian banks during festival seasons or salary cycles experience transaction volumes that can spike 300% above normal levels. Your integration architecture must handle these peaks without degradation.

- Queue depth monitoring and management prevent bottlenecks before they impact operations. Set up automated monitoring that triggers alerts when queue depths exceed thresholds. A queue consistently at 80% capacity indicates that your consumers can't keep pace with message production. Leading banks implement dynamic software maintenance & support services (for consumer scaling)—automatically starting additional message processing instances when queue depths rise and shutting them down during low-volume periods to optimize resource utilization.

- Message persistence strategy balances performance against reliability. Persistent messages guarantee delivery even if IBM MQ crashes, but they're slower due to disk I/O. Non-persistent messages are faster but can be lost during failures. For banking, analyze each message type: high-value payment instructions must be persistent, while account balance inquiries might use non-persistent messaging. This nuanced approach optimizes performance while maintaining reliability where it matters.

- Connection pooling and resource optimization dramatically impact throughput. Creating a new connection to IBM MQ for each message is expensive in terms of CPU and time. Connection pools maintain reusable connections that integration flows can borrow and return. Properly configured connection pools have enabled Indian banks to process 10,000+ messages per second on modest hardware, compared to a few hundred without pooling.

Reducing Point-to-Point Integration Complexity

The complexity explosion from point-to-point integration is one of the most common problems in banking IT landscapes. When each system connects directly to every other system it needs to communicate with, you create an unmaintainable web of connections.

- Canonical data model implementation establishes a standard message format used internally within your ESB. External systems send data in their native formats. IIB transforms inbound messages to your canonical model, processes the message using business rules, and then transforms outbound messages to whatever format the destination system requires. This pattern means that adding a new system requires creating just two transformations (inbound and outbound) rather than connecting to every existing system.

- Service-oriented architecture patterns expose integration capabilities as reusable services. Instead of creating custom integration flows for each new digital initiative, you build a library of banking services—such as Customer Lookup, Account Validation, Payment Processing, etc. New applications invoke these services through standard interfaces, dramatically reducing development time and ensuring consistency across all channels.

- API management layer integration connects IIB with API management platforms to expose banking services to external developers and partners. When you launch a new mobile app or enable third-party integrations under RBI's account aggregator framework, the API layer handles authentication, rate limiting, and developer management. In contrast, IIB handles the actual integration complexity behind the scenes.

Enterprise Service Bus Banking Architecture Patterns

Successful ESB implementations in Indian banks follow proven architectural patterns that address specific banking requirements.

- Request-reply messaging patterns support synchronous operations in which the calling application requires an immediate response. When a customer checks their account balance through mobile banking, the app sends a request message via IBM MQ. IIB processes it by calling the core banking system and returns the response, all typically within 200-300 milliseconds. This pattern requires careful timeout configuration and exception handling to manage scenarios where backend systems don't respond promptly.

- Publish-subscribe patterns enable event-driven architectures in which multiple systems need to be notified of banking events. When a significant transaction occurs, your fraud detection system, compliance monitoring system, customer notification system, and reporting system all need to know immediately. Rather than your core banking system calling each system individually, it publishes a single event to IBM MQ. Subscribing systems independently consume the event and take appropriate action, enabling parallel processing and system decoupling.

- Content-based routing directs messages to different processing paths based on message content. Payment transactions above Rs 2 lakhs might be routed through additional fraud checks and manual approval workflows, while smaller transactions flow through straight-through processing. IIB's routing capabilities let you implement complex business rules without hardcoding them in individual applications, making it easy to adjust thresholds and routing logic as business requirements evolve.

Security and Compliance in IIB/MQ Banking Integration

In the banking sector, the integration between IBM Integration Bus (IIB)—now evolved into IBM App Connect—and IBM MQ forms the backbone of critical payment processing and core banking communication. Security and compliance in this stack are not just features but regulatory mandates (e.g., PCI-DSS, GDPR, DORA).

Zero Data Loss During Migration Cutover

Migration from legacy integration platforms to IIB/MQ represents one of the highest-risk activities for bank IT teams. The cutover period—when you switch from old to new systems—must be executed flawlessly.

- Parallel run strategies operate old and new integration platforms simultaneously during transition periods. Messages flow through both platforms, allowing you to validate that IIB/MQ produces identical results to your legacy system before cutting over completely. Several Indian banks have successfully used parallel runs lasting 2-4 weeks to build confidence before decommissioning legacy platforms.

- Message replay capabilities provide insurance against cutover problems. IBM MQ's dead letter queues and message journaling capture messages that fail processing. If your cutover encounters unexpected issues, you can roll back to the legacy platform and replay captured messages through the old system, ensuring zero transaction loss. This capability has saved multiple implementations from data loss during problematic cutovers.

- Phased migration approaches reduce risk by migrating one integration flow or banking channel at a time. Start with non-critical integrations, such as report generation or inquiry services, gain operational experience with IIB/MQ, then progressively migrate more critical flows, such as payment processing. This approach extends migration timelines but dramatically reduces risk compared to big-bang cutovers.

Detecting and Responding to Security Threats in Real-Time

Security threats targeting banking integration layers have become increasingly sophisticated. Your IIB/MQ implementation must actively detect and respond to security anomalies.

- Anomaly detection in message patterns uses behavioral analysis to identify suspicious activity. If an integration suddenly starts processing 10x the normal message volume from an unusual source IP address, this could indicate a compromised credential or an injection attack. Leading implementations integrate IIB/MQ logs with Security Information and Event Management (SIEM) systems that apply machine learning to detect anomalies and trigger automated responses.

- End-to-end message encryption protects sensitive financial data as it flows through integration layers. While IBM MQ supports channel encryption, truly sensitive data like account numbers and transaction amounts should be encrypted at the application level before entering the integration layer. This ensures that even privileged users with access to IBM MQ administration tools cannot view sensitive customer data in plaintext.

- Integration security patterns specific to banking include message-level digital signatures to prove non-repudiation, token-based authentication to secure service invocations, and message validation against schemas to prevent injection attacks. These patterns must be consistently applied across all integration flows to avoid creating security gaps that attackers can exploit.

Recommended DevOps Pipeline for Banking Integration Projects

Traditional waterfall development cycles that take months from design to production deployment are incompatible with the pace of digital banking innovation. Modern DevOps best practices, adapted to banking regulatory requirements, enable rapid, reliable deployments.

- Continuous integration for IIB flows automatically builds and tests integration flows whenever IIB developers commit code changes. Your CI/CD pipeline compiles message flows, runs unit tests to validate transformation logic, executes integration tests against mock backend systems, and performs security scans to identify vulnerable configurations. Automated testing catches errors during development rather than in production.

- Automated deployment pipelines move tested integration flows from development through UAT to production with minimal manual intervention. IBM App Connect Enterprise supports BAR file deployment automation through command-line interfaces and REST APIs. Leading banks deploy integration changes multiple times per week using automated pipelines, compared to monthly release cycles under manual deployment processes.

- Environment provisioning automation uses infrastructure-as-code tools to create consistent IIB/MQ environments on demand. When your team needs a new UAT environment for testing a major release, automated provisioning creates a complete environment—IBM MQ queue managers, IIB integration nodes, supporting databases, and monitoring tools—in hours rather than weeks. This capability dramatically accelerates project timelines and ensures environmental consistency.

Performance Optimization and Monitoring for IBM IIB/MQ Integration

In banking, where milliseconds can impact high-frequency trading or real-time payment settlement (like ISO 20022), performance optimization is as much about predictability as it is about speed. This includes:-

Reducing Deployment Time from Days to Hours

Deployment speed directly impacts your ability to respond to competitive pressures and regulatory changes. Traditional bank deployment processes, taking 2-3 days, create a business disadvantage.

- Zero-downtime deployment strategies allow you to deploy new integration flow versions without stopping message processing. IBM App Connect Enterprise supports hot deployment, where new flow versions activate without restarting integration servers. Messages in flight complete processing under the old version while new messages are processed under the latest version, enabling seamless transitions during business hours.

- Rollback capabilities provide confidence for aggressive deployment schedules. Every deployment should include an automated rollback procedure that can restore the previous version within minutes if problems emerge. Leading implementations maintain the last three production versions readily deployable, with monitoring dashboards showing real-time metrics that help teams quickly identify whether a new deployment is performing as expected.

- Blue-green deployment patterns eliminate risk for major releases. You deploy the new integration version to a parallel "green" environment while the current "blue" environment continues handling production traffic. After validating green environment functionality, you switch traffic from blue to green instantly using the load balancer configuration. If problems emerge, you switch back to blue immediately. This pattern has enabled several Indian banks to deploy complex integration changes during business hours with zero customer impact.

Pro TIp: When internal capacity is limited, IBM App Connect integration developers can help teams add specialized expertise faster without slowing delivery momentum.

Integration Patterns That Reduce Cascading Failures

Banking systems are highly interconnected. A failure in one system can cascade through the integration layer, creating widespread outages. Specific patterns prevent cascade failures.

- Circuit breaker pattern implementation protects your integration layer from failing backend systems. When IIB detects that a backend system is failing repeatedly—for example, your card management system is timing out—the circuit breaker opens, immediately failing new requests without attempting backend calls. This prevents thread exhaustion in IIB while allowing other integrations to function normally. After a configured timeout, the circuit breaker attempts a test request; if successful, it closes and resumes standard processing.

- Bulkhead isolation patterns separate integration flows and place different banking functions into isolated resource pools. Payment processing flows run on dedicated integration servers separate from inquiry processing flows. If inquiry processing experiences a resource leak that consumes all available memory, payment processing continues unaffected. This pattern has proven critical during incident response scenarios in multiple Indian banking implementations.

- Timeout and retry strategies must be carefully tuned for banking operations. Aggressive retry logic can overwhelm failing systems, preventing their recovery. Leading implementations use exponential backoff—the first retry occurs after 1 second, the second after 2 seconds, the third after 4 seconds, and so on. This gives failing systems time to recover while ensuring that transient errors don't cause permanent failures.

Middleware Performance Tuning for Banking Operations

Performance tuning separates adequate implementations from exceptional ones. Indian banks, which process millions of daily transactions, require optimization at every level.

- JVM tuning for IIB execution groups significantly impacts throughput and stability. Default JVM settings rarely suit the characteristics of a banking workload. Leading implementations allocate 8-16GB of heap memory for integration servers handling high volumes, tune garbage collection for low latency, and configure thread pools that match their workload patterns. Proper JVM tuning has improved message processing throughput by 200-300% in several implementations.

- IBM MQ channel tuning optimizes message transfer between queue managers. Default channel batch sizes and heartbeat intervals suit general use cases but not high-volume banking operations. Increasing batch sizes reduces network overhead for high-volume channels, while adjusting heartbeat intervals prevents false failure detection during peak processing when systems are heavily loaded.

- Message processing parallelism determines how many messages your integration flows process simultaneously. IIB's additional instances feature allows multiple flow instances to process messages from the same queue in parallel. Banks processing payment files containing thousands of transactions use parallel processing to reduce batch processing times from hours to minutes, enabling faster funds availability for customers.

Legacy System Modernization Through IIB/MQ Integration

A significant majority of Indian Public Sector Undertaking (PSU) banks rely on mainframe-based core banking systems (CBS). Exposing these legacy backends directly to high-velocity digital channels introduces critical security vulnerabilities and performance bottlenecks.

By implementing an IBM Integration Bus (IIB) and MQ framework, banks can establish a robust abstraction layer. This ensures seamless protocol transformation and asynchronous decoupling, protecting the mainframe's integrity while enabling modern, agile digital services.

- Mainframe integration patterns leverage IBM MQ for z/OS to enable secure, high-performance communication between the mainframe and other systems. Your digital banking applications send requests to IBM MQ queues, IIB processes, and routes messages to mainframe queues; mainframe applications process transactions using CICS or IMS, and responses flow back through the same queue architecture. This pattern provides mainframe isolation while enabling modern channel access.

- Synchronous-to-asynchronous transformation addresses performance mismatches between responsive digital channels and batch-oriented mainframe operations. Mobile apps expect responses in milliseconds, but complex mainframe transactions might take seconds. IIB implements facade services that immediately acknowledge digital requests, queue them for mainframe processing, and notify digital channels when processing completes. This pattern provides a responsive user experience while working within the constraints of the mainframe.

- Data format transformation bridges the gap between modern JSON/REST interfaces used by digital channels and traditional formats like COBOL copybooks used by mainframes. IIB's extensive transformation capabilities convert between formats without requiring modifications to the mainframe. This has enabled multiple Indian banks to launch modern digital banking services without touching legacy mainframe code.

Core Banking Modernization Without Service Disruption

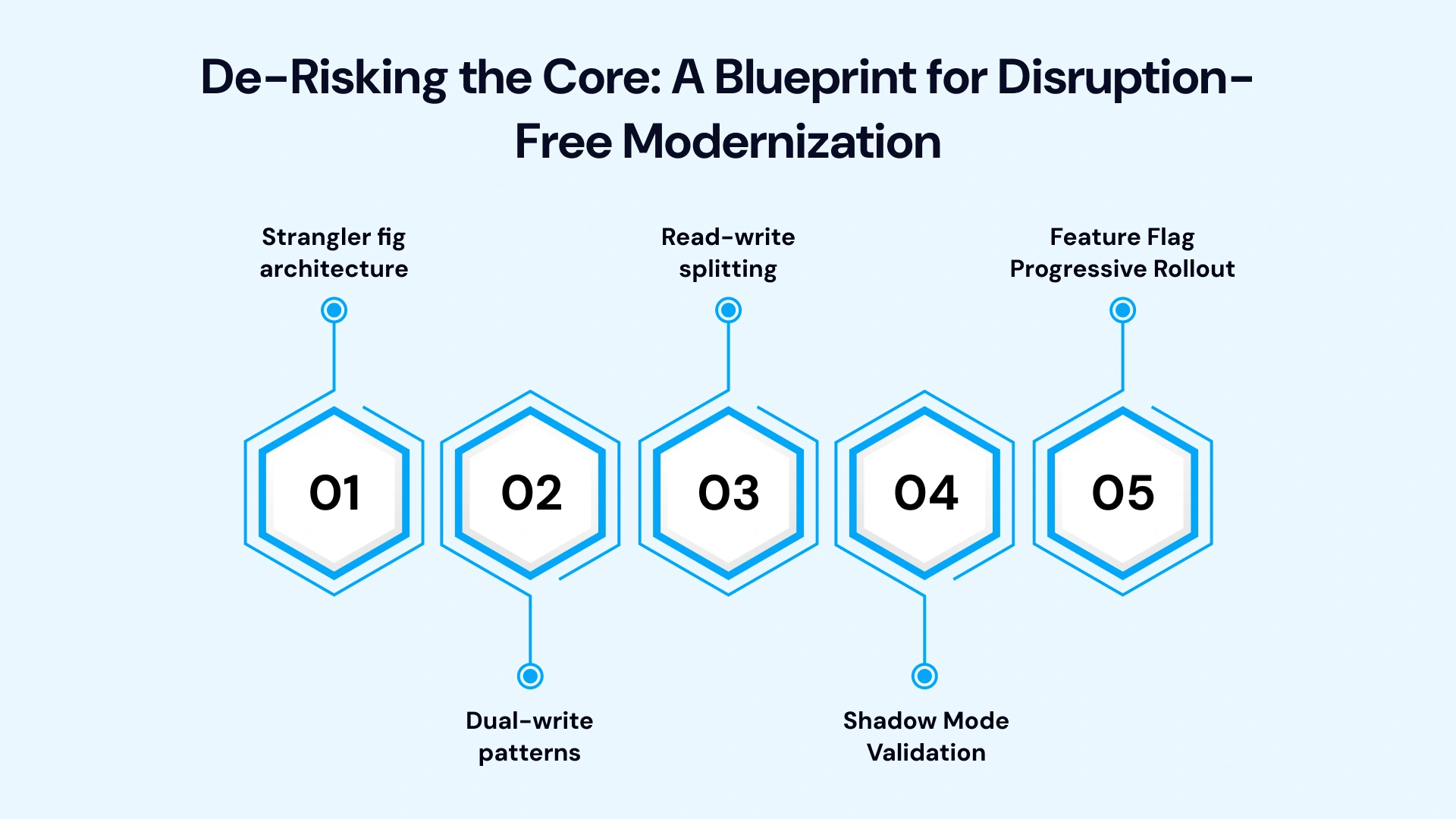

Replacing entire core banking systems carries existential risk for banks. Gradual modernization through strangler fig patterns offers a safer path. This includes: -

Strangler fig architecture

Gradually replaces legacy functionality with modern services. You build new capabilities on modern platforms (such as cloud-native microservices). At the same time, IIB intelligently routes transactions—new account types process on the contemporary platform while existing accounts continue on legacy systems. Over time, as you migrate account types and functionality, the modern platform handles increasing transaction volumes until the legacy system can be retired.

Dual-write patterns

Maintain data consistency across legacy and modern systems during transition periods. When account data is updated, IIB writes to both legacy and modern databases to ensure consistency. This pattern enables you to build and validate modern systems using real production data before a complete cutover, reducing migration risk.

Read-write splitting

Directs read and write transactions to modern systems while routing updates to legacy systems during early modernization phases. This pattern lets you offload query traffic from legacy systems (often the majority of transactions) to modern, scalable platforms while maintaining legacy systems as the single source of truth for transactional operations until modern platforms are fully validated.

Shadow Mode Validation

Runs modern and legacy systems in parallel using IIB to duplicate live transactions. This allows for automated reconciliation and performance benchmarking against 200M+ real-world transactions without customer risk, ensuring 99.97% consistency before cutover.

Feature Flag Progressive Rollout

Uses IIB routing logic to migrate segments incrementally (e.g., 1% to 100%) with instant rollback capability. This transforms high-risk "big-bang" migrations into managed waves, allowing for real-time monitoring and automated reversion if quality thresholds are breached.

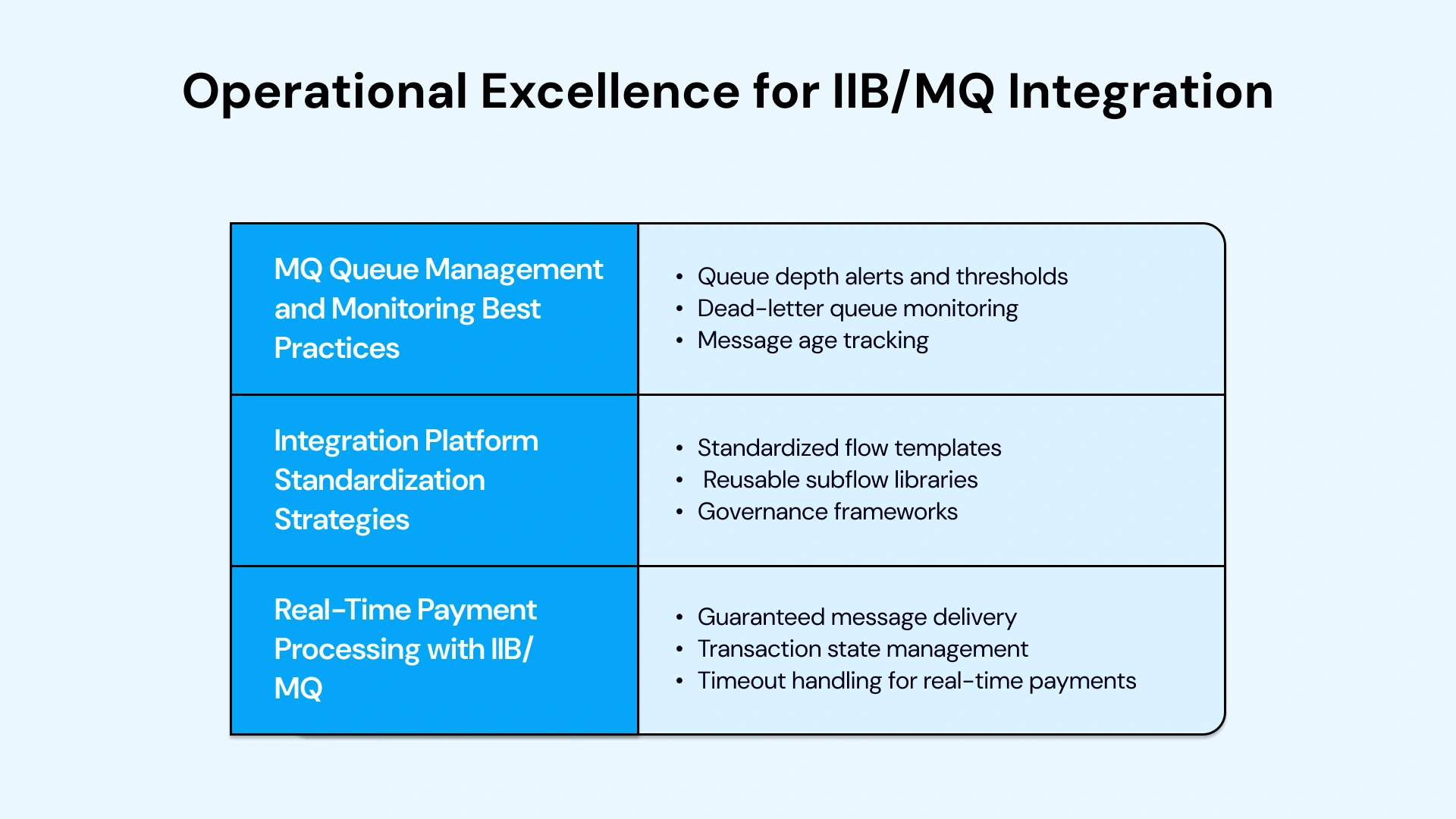

Operational Excellence for IIB/MQ Banking Integration

Achieving operational excellence in a core banking environment requires moving beyond basic connectivity to a state of "Invisible Infrastructure. This

MQ Queue Management and Monitoring Best Practices

Effective queue management prevents small issues from becoming major incidents. Proactive monitoring and management practices have proven essential across multiple banking implementations.

- Queue depth alerts and thresholds provide early warning of processing bottlenecks. Configure monitoring to trigger escalating alerts as queues fill—informational alert at 50% capacity, warning at 75%, critical at 90%. These alerts enable operations teams to investigate and resolve issues before queue capacity is exhausted and message processing stops completely.

- Dead-letter queue monitoring identifies integration failures that require attention. When messages repeatedly fail to be processed, IBM MQ moves them to dead-letter queues. Effective operations include daily dead letter queue reviews, analysis of failure patterns, and systematic resolution. Leading banks maintain zero dead letter queue backlogs through disciplined monitoring and rapid issue resolution.

- Message age tracking ensures that time-sensitive banking transactions are processed promptly. Configure monitoring to alert on messages exceeding age thresholds—for example, alert if payment messages remain unprocessed for more than 5 minutes. This monitoring has prevented customer-impacting delays in multiple scenarios where backend system slowdowns went unnoticed by traditional tracking.

Integration Platform Standardization Strategies

Standardization reduces complexity, improves operational efficiency, and accelerates development. Indian banks with standardized integration platforms report 40-60% faster project delivery compared to fragmented environments.

- Standardized flow templates provide pre-built integration patterns for common banking scenarios. When developers need to implement a new account inquiry service, they start with a standard template that includes error handling, logging, security, and monitoring, rather than building from scratch. This ensures consistency across integration flows and reduces development time from weeks to days.

- Reusable subflow libraries capture common integration logic that appears across multiple flows. Authentication, data validation, error handling, and audit logging are implemented once as reusable subflows that all integration flows invoke. When security requirements change, you update the authentication subflow once rather than modifying hundreds of individual flows.

- Governance frameworks establish standards for integration design, naming conventions, error handling approaches, and operational procedures. Leading banks operate integration centers of excellence that define standards, review new integration implementations for compliance, and provide training to ensure consistent practices across development teams.

Real-Time Payment Processing with IIB/MQ

Real-time payment systems like UPI and IMPS have transformed Indian banking. IIB/MQ architectures must support instant payment processing with complete reliability.

- Guaranteed message delivery for payment instructions is non-negotiable. IBM MQ's persistent messaging with Quality Assurance Services guarantees that once a payment message enters the integration layer, it will be delivered to the destination system exactly once, even if system failures occur during processing. This reliability foundation has enabled Indian banks to process billions of UPI transactions without payment loss.

- Transaction state management tracks payment processing across multiple systems. A single customer payment might touch 5-10 systems—fraud checking, AML screening, account validation, core banking, switch routing, etc. IIB's built-in transaction coordination and compensating transaction capabilities ensure that if any step fails, the previous steps are rolled back, maintaining data consistency across systems.

- Timeout handling for real-time payments balances customer experience against processing reliability. UPI mandates response times under 10 seconds. If your core banking system doesn't respond within this window, your integration must make intelligent decisions—return a timeout error to the customer, queue the transaction for later processing, or route to a backup processing path. Proper timeout handling has prevented thousands of failed transactions in production implementations.

Leverage VLink's Expertise for IIB/MQ Integration

Implementing enterprise-grade IBM IIB/MQ integration for banking operations requires specialized expertise that combines deep technical knowledge with a practical understanding of banking operations, regulatory requirements, and Indian market dynamics. VLink's dedicated team of certified support engineers and specialists brings 15+ years of proven experience delivering mission-critical integration solutions for leading Indian banks and financial institutions.

Our integration specialists hold advanced certifications in IBM Integration Bus, IBM MQ, and IBM App Connect Enterprise, with hands-on experience implementing complex banking integration landscapes. We've successfully delivered integration modernization projects for PSU banks, private sector banks, and NBFCs across India, processing transaction volumes exceeding 50 million messages daily with 99.99% availability.

VLink’s Advantages: -

- VLink's legacy system modernization services help Indian banks navigate the treacherous path from decades-old mainframe systems to modern, API-driven architectures without disrupting critical banking operations. We've pioneered strangler fig approaches that enable gradual modernization, implementing IIB/MQ integration layers that safely bridge legacy and modern systems during multi-year transformation journeys. Our methodologies have enabled banks to launch new digital services in months rather than years while maintaining complete operational continuity.

- Our 24/7 support engineering teams provide round-the-clock coverage that Indian banking operations demand. When integration issues occur during critical processing windows—month-end closing, salary disbursement cycles, and festival shopping peaks—our support engineers respond within minutes with deep expertise to diagnose and resolve them quickly. We maintain support partnerships with several Indian banks where our engineers serve as extensions of their internal teams, providing expertise for complex issues while enabling knowledge transfer.

- VLink ensures your IIB/MQ integration infrastructure remains optimized, secure, and compliant with evolving regulatory requirements. Our support includes proactive monitoring, performance optimization, security patch management, and regular health assessments that identify potential issues before they impact operations. Banks leveraging our maintenance services report a 60-70% reduction in integration-related incidents compared to self-managed environments.

- For banks facing skills gaps in specialized integration technologies, VLink's IT staff augmentation services provide experienced integration developers, architects, and administrators who seamlessly integrate with your internal teams. Our augmentation model provides flexible scaling—ramping up during major integration projects and scaling down during steady-state operations—while ensuring knowledge transfer to build internal capabilities over time.

- Our quality assurance services, specifically designed for banking integration, include comprehensive testing frameworks that validate functional correctness, performance under load, security configurations, and disaster recovery capabilities. We've prevented costly production issues across multiple implementations through rigorous pre-production testing that simulates real-world banking scenarios, including peak load and failure conditions.

VLink's approach combines technical excellence with practical business understanding. We recognize that successful integration isn't just about connecting systems—it's about enabling business capabilities that drive competitive advantage while managing risk in highly regulated banking environments.

Our consulting services help IT Heads and technology leaders develop integration roadmaps aligned with business strategy, evaluate build-versus-buy decisions for integration capabilities, and optimize integration portfolios for cost and performance.

Conclusion: Building the Integration Foundation for Banking Success

IBM IIB/MQ integration represents far more than middleware deployment—it's the foundation enabling Indian banks to compete in an increasingly digital financial services landscape while managing the complexity of legacy system modernization, regulatory compliance, and operational scale. The best practices outlined in this guide reflect hard-won lessons from real-world banking implementations across India's diverse financial services sector.

Success in IIB/MQ integration requires balancing multiple competing concerns: performance versus reliability, innovation speed versus operational stability, and modernization ambition versus risk management. Indian banks that excel in this balancing act share common characteristics—they treat integration as a strategic capability rather than an infrastructure expense, invest in specialized skills and expertise, implement disciplined operational practices, and partner with experienced specialists who understand banking's unique requirements.

The journey from fragmented point-to-point integration landscapes to elegant, scalable ESB architectures powered by IIB/MQ is neither quick nor easy. It requires sustained commitment from technology leadership, investment in skills development, and patience to implement best practices thoroughly rather than seeking shortcuts that create technical debt. However, banks that complete this journey achieve remarkable benefits: 10x faster time-to-market for new digital services, 99.99% availability for critical payment processing, 60% reduction in integration maintenance costs, and the architectural flexibility to pursue ambitious modernization strategies without unacceptable risk.

As India's banking sector continues its digital transformation—driven by regulatory initiatives, competitive pressures from fintech disruptors, and rising customer expectations—robust integration capabilities will increasingly separate winners from strugglers. The banks that invest today in world-class IIB/MQ integration capabilities will possess the agility and resilience to seize opportunities and navigate challenges in India's dynamic financial services market.

Ready to elevate your banking integration capabilities? Contact VLink today to discuss how our support engineers' expertise can accelerate your digital transformation while maintaining the operational excellence Indian banking demands.

Global Delivery Manager, VLink Inc.

Shivisha Patel serves as the Global Delivery Manager at VLink Inc., bringing a wealth of experience in program delivery and management, particularly in the insurance and banking sectors. She has a robust technical background with deep expertise in WebSphere MQ, WTX, IIB, middleware, and enterprise system integration.

Shivisha Patel

Shivisha Patel