Cash advance apps like MoneyLion, Dave, and Brigit have collectively attracted tens of millions of users by solving a problem banks ignored for decades: giving people access to the money they've already earned — instantly, without credit checks, without humiliation.

But here's what no one tells you clearly: how much does it actually cost to build one?

If you've been searching for a definitive answer, you've likely landed on pages that give you a range so wide — $10,000 to $500,000 — that it's practically useless for budgeting.

This guide is different. Shivisha Patel, VLink's Global Delivery Manager with hands-on experience delivering financial software for insurance and banking clients globally, breaks down every cost variable so you can plan your investment with confidence.

What Is MoneyLion - And Why Is It the Benchmark?

MoneyLion is a US-based fintech super-app that launched in 2013. What began as a simple cash advance service has evolved into a full financial services wellness platform with over 7 million users (Idea Usher, 2024). It's the benchmark because it's done something rare in fintech: it combined five revenue-generating services into one seamless experience.

MoneyLion's Core Feature Set

- Instacash: Interest-free cash advances up to $500 (up to $1,000 with RoarMoney direct deposit)

- RoarMoney: Managed checking account with cashback debit card

- Credit Builder Plus: Secured credit-builder loan reported to all 3 bureaus

- MoneyLion Invest: Automated micro-investing with managed portfolios

- Financial Insights: AI-powered spending analysis and personalised alerts

The reason founders benchmark against MoneyLion isn't that they want to clone it — it's because MoneyLion has proven the market, defined user expectations, and set the compliance and technical standards that any competitive product must meet.

How Much Does It Cost to Build a Cash Advance App Like MoneyLion? (2026 Breakdown)

The answer depends on three variables: feature scope, your development team's location, and US regulatory compliance requirements. Here's the definitive 2026 cost breakdown across three tiers:

App Tier Cost Overview:

| App Tier | Core Features Included | Est. Cost (USD) | Timeline |

| MVP / Basic | Cash advance, user auth, basic UI, account link | $40,000 – $80,000 | 3 – 5 months |

| Standard / Mid-Market | MVP + budgeting, credit monitoring, notifications | $80,000 – $150,000 | 5 – 8 months |

| Enterprise / MoneyLion-Level | Full suite: AI eligibility, investment tools, EWA, open banking | $150,000 – $350,000+ | 9 – 14 months |

Note: Costs above reflect full-cycle development, including design, development, QA, and first-year compliance setup. Ongoing maintenance costs an additional $1,500–$5,000 per month.

Development Phase Cost Breakdown

Understanding where your budget goes helps you negotiate smarter and avoid scope creep. Here's how a cash advance mobile app development budget typically distributes across phases:

| Development Phase | Key Activities | Cost Range (USD) | Timeline |

| 1. Discovery & Planning | Market research, feature list, compliance roadmap, and architecture design | $8,000 – $18,000 | 3 – 4 weeks |

| 2. UI/UX Design | Wireframes, prototypes, user testing, accessibility review | $12,000 – $28,000 | 4 – 6 weeks |

| 3. Core Development | Front-end, back-end, API integrations (Plaid, Stripe, eKYC) | $40,000 – $120,000 | 10 – 20 weeks |

| 4. Security & Compliance | PCI DSS, SOC 2 prep, pen testing, state licensing review | $10,000 – $25,000 | 4 – 6 weeks |

| 5. QA & Testing | Functional, regression, performance, device testing | $8,000 – $18,000 | 3 – 4 weeks |

| 6. Launch & Deployment | App Store submission, cloud infrastructure setup, and monitoring | $5,000 – $12,000 | 2 – 3 weeks |

| 7. Post-Launch Maintenance | Bug fixes, OS updates, feature iterations, security patches | $1,500 – $5,000/month | Ongoing |

How Development Team Location Affects Your Budget

One of the most impactful cost levers in cash advance app development is where your development team is located. Hourly rates vary by a factor of 4–8x between the lowest and highest cost markets:

| Region | Hourly Rate (USD) | Full-Project Cost | Best For |

| United States | $100 – $200/hr | $250,000 – $500,000+ | On-site collaboration, regulatory compliance |

| India (VLink HQ) | $25 – $60/hr | $50,000 – $150,000 | Cost-effective, strong fintech talent pool |

| Eastern Europe | $40 – $90/hr | $80,000 – $200,000 | Quality + mid-range cost balance |

| South-East Asia | $20 – $50/hr | $40,000 – $120,000 | Budget projects with lower complexity |

VLink's engagement model gives US-based clients the governance and communication quality of a US partner with development delivered from our India team — combining cost efficiency with zero compromise on compliance expertise.

MoneyLion vs. Dave vs. Brigit: What It Costs to Build Each

Before choosing which app to benchmark yours against, understand the feature depth — and its cost implications:

| Feature | MoneyLion | Dave | Brigit |

| Max Cash Advance | Up to $500 (RoarMoney req.) | Up to $500 | Up to $500 |

| Monthly Fee | $0 basic / $19.99 Plus | $1/month | $9.99/month |

| Credit Building | Yes | No | Yes |

| Investing Tools | Yes | No | No |

| Credit Check Required | No | No | No |

| Dev Cost to Replicate | $150,000 – $350,000+ | $80,000 – $150,000 | $60,000 – $120,000 |

Key insight: Dave's simplicity ($80K–$150K to replicate) makes it the most accessible starting point for first-time fintech founders. MoneyLion's full suite ($150K–$350K+) requires a Series A-level budget but delivers the strongest user retention and monetisation potential.

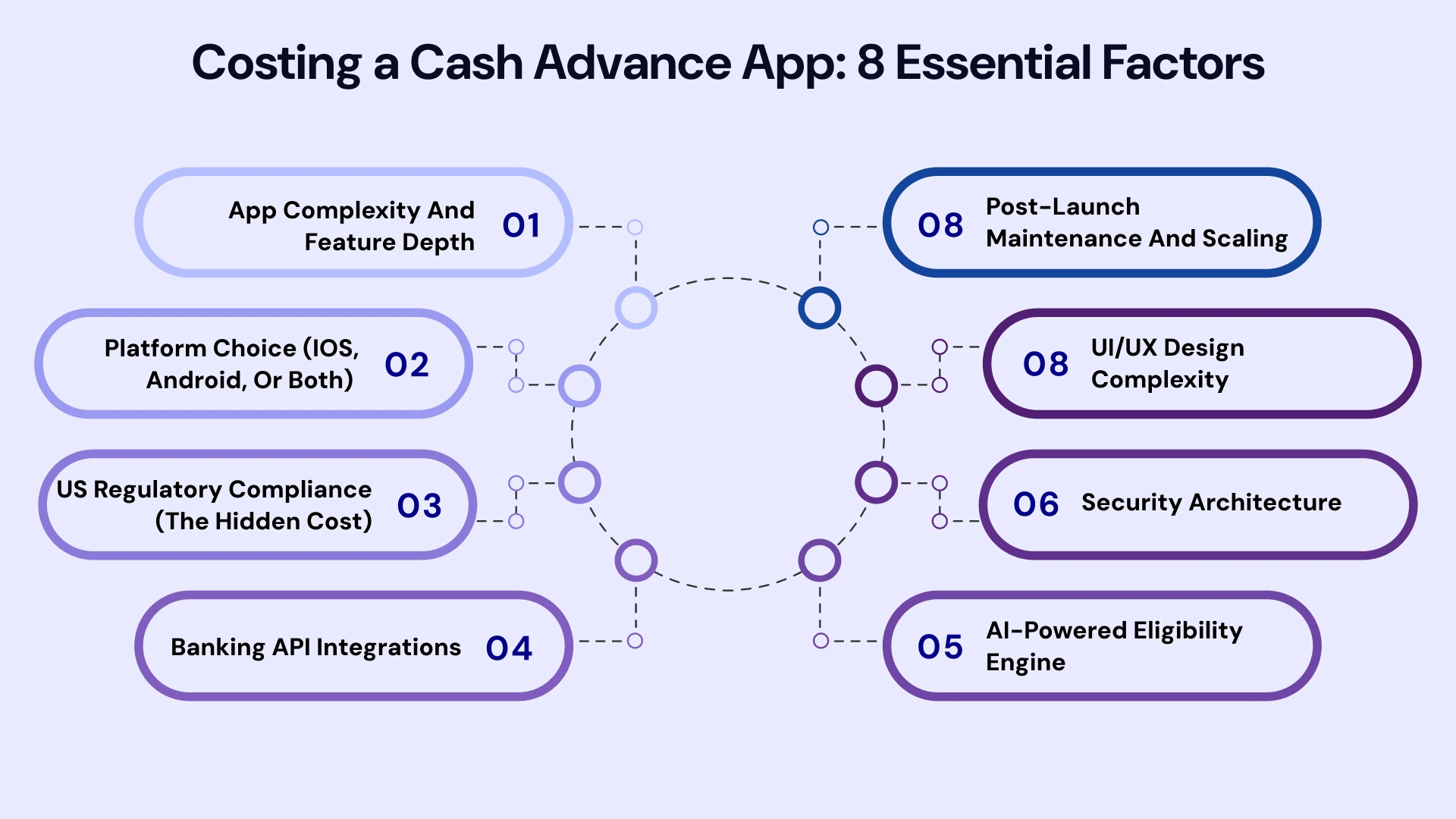

8 Factors That Directly Impact Your Cash Advance App Development Cost

Here are the 8 primary factors that directly impact your development budget:

1. App Complexity and Feature Depth

The biggest cost driver is your feature list. A basic MVP with cash advance disbursement, user authentication, and bank account linking costs $40,000–$80,000. Adding AI-powered eligibility scoring, credit monitoring, and investment tools can triple that figure.

Rule of thumb: every major feature category (budgeting, investing, EWA, credit building) adds $20,000–$50,000 to your development budget.

2. Platform Choice (iOS, Android, or Both)

Building for a single platform (iOS or Android) costs 30–40% less than building natively for both. Cross-platform frameworks like React Native or Flutter reduce this gap significantly — delivering near-native performance on both platforms from a single codebase at roughly 60% of the native dual-platform cost.

3. US Regulatory Compliance (The Hidden Cost)

This is the line item most budget guides ignore. Building a cash advance app for the US markets requires compliance with:

- Consumer Financial Protection Bureau (CFPB) regulations — particularly the Earned Wage Access guidance updated in 2024

- State money transmitter licenses — required in most states where you offer cash advances (average cost: $1,000–$5,000 per state application)

- PCI DSS compliance — mandatory for any card or payment processing

- SOC 2 Type II certification — increasingly required by banking partners

Total compliance setup cost: $10,000–$25,000 in development + $15,000–$50,000 in legal/licensing fees, depending on target states.

4. Banking API Integrations

A cash advance app lives or dies by its bank connectivity. The primary integration cost centres include:

- Plaid API: $500–$2,000/month in production; integration dev time 80–120 hours

- MX (alternative to Plaid): Similar pricing, often preferred for credit union clients

- Dwolla or Stripe for ACH disbursement: $0.25–$0.50 per transfer + integration dev time

- eKYC providers (Jumio, Onfido): $0.50–$3 per verification

Integration complexity for a MoneyLion-equivalent app: 400–600 development hours across all third-party services.

5. AI-Powered Eligibility Engine

MoneyLion's competitive moat is its risk assessment model — it evaluates users based on banking behaviour, spending patterns, and income stability rather than credit scores. Building a comparable AI eligibility engine adds $30,000–$70,000 to your budget and requires ongoing model training and monitoring.

An alternative for the MVP stage: use rule-based eligibility (income threshold + account age) and migrate to ML-based scoring at Series A.

6. Security Architecture

Fintech apps handle some of the most sensitive user data that exists. Your security build must include:

- End-to-end encryption (AES-256) for all financial data

- Multi-factor authentication (MFA) and biometric login

- Regular penetration testing ($5,000–$15,000 per engagement)

- Fraud detection layer — rule-based at MVP, ML-driven at scale

Security is not a phase — it's a design principle that runs through every layer of your application stack.

7. UI/UX Design Complexity

Financial apps live in a high-anxiety user context. Users are dealing with money stress when they open your app. UI/UX Design investment directly impacts conversion rates, trust, and retention.

Budget $12,000–$28,000 for professional UI/UX developers for a cash advance app. This should include user testing with real target users — ideally millennials and Gen Z in the sub-$50K household income bracket, who are your core addressable market.

8. Post-Launch Maintenance and Scaling

The launch is not the finish line. Cash advance apps require continuous investment in:

- iOS and Android OS updates (Apple and Google release major updates annually)

- Bank API version updates (Plaid alone releases breaking changes multiple times per year)

- Feature iterations based on user feedback

- Security patches and compliance updates

Budget $1,500–$5,000 per month for ongoing maintenance from day one.

Recommended Tech Stack for a Cash Advance App in 2026

The technology choices you make at the architecture stage will define your app's scalability, security posture, and ongoing cost. Here's the stack VLink recommends for a MoneyLion-scale cash advance application:

| Layer | Recommended Technology | Purpose |

| Frontend (Mobile) | React Native / Flutter | Cross-platform iOS + Android from single codebase |

| Backend | Node.js / Python (Django) | API services, business logic, loan engine |

| Database | PostgreSQL + Redis | Transactional data + session caching |

| Cloud Infrastructure | AWS / Google Cloud | Scalable compute, SOC 2 compliance readiness |

| Bank Connectivity | Plaid API / MX | Account verification, income analysis |

| Payments | Stripe / Dwolla | ACH transfers, instant disbursements |

| eKYC / Identity | Jumio / Onfido | User onboarding, fraud prevention |

| AI / Risk Scoring | TensorFlow / custom ML model | Creditworthiness prediction, eligibility engine |

How to Build a Cash Advance App Like MoneyLion: 8-Step Process

Here is the end-to-end development process VLink follows for fintech app builds:

1. Market Research and Regulatory Mapping: Define your target US states, identify money transmitter licensing requirements, and map the competitive landscape. This phase determines your compliance roadmap.

2. Feature Definition and MVP Scoping: Resist the urge to build everything on day one. Define the minimum feature set that delivers core value. A cash advance app MVP needs: user onboarding with eKYC, bank account linking via Plaid/MX, eligibility checking, cash advance disbursement, and repayment scheduling.

3. UI/UX Design and Prototyping: Create wireframes and high-fidelity prototype designs. Test with real users — particularly your ICP of credit-limited millennials and gig workers. A well-tested design saves 20–30% in development rework costs.

4. Tech Stack Selection and Architecture Design: Choose your framework (React Native recommended for MVP), cloud provider (AWS, Azure, or GCP), database structure, and API integration sequence. This phase defines your entire technical roadmap.

5. Core Development - Front-End and Back-End: Build in sprints.

Front-end: user flows, cash advance request interface, notifications. And Back-end: loan engine, eligibility logic, bank integration, payment processing. Plan for 10–20 weeks of active development.

6. Security Implementation and Compliance Review: Conduct penetration testing, implement PCI DSS controls, and set up SOC 2 audit readiness. Engage a fintech compliance counsel to review your advance terms, fee disclosures, and state-by-state regulatory requirements.

7. QA and Multi-Device Testing: Test on iOS and Android across 20+ device configurations. Load test your backend to 10x projected user volume. Test all bank integration failure scenarios.

8. App Store Submission, Launch, and Monitoring: Submit to Apple App Store and Google Play (allow 1–2 weeks for review). Set up real-time monitoring for transaction failures, fraud patterns, and API downtime. Launch with a beta user group before full public release.

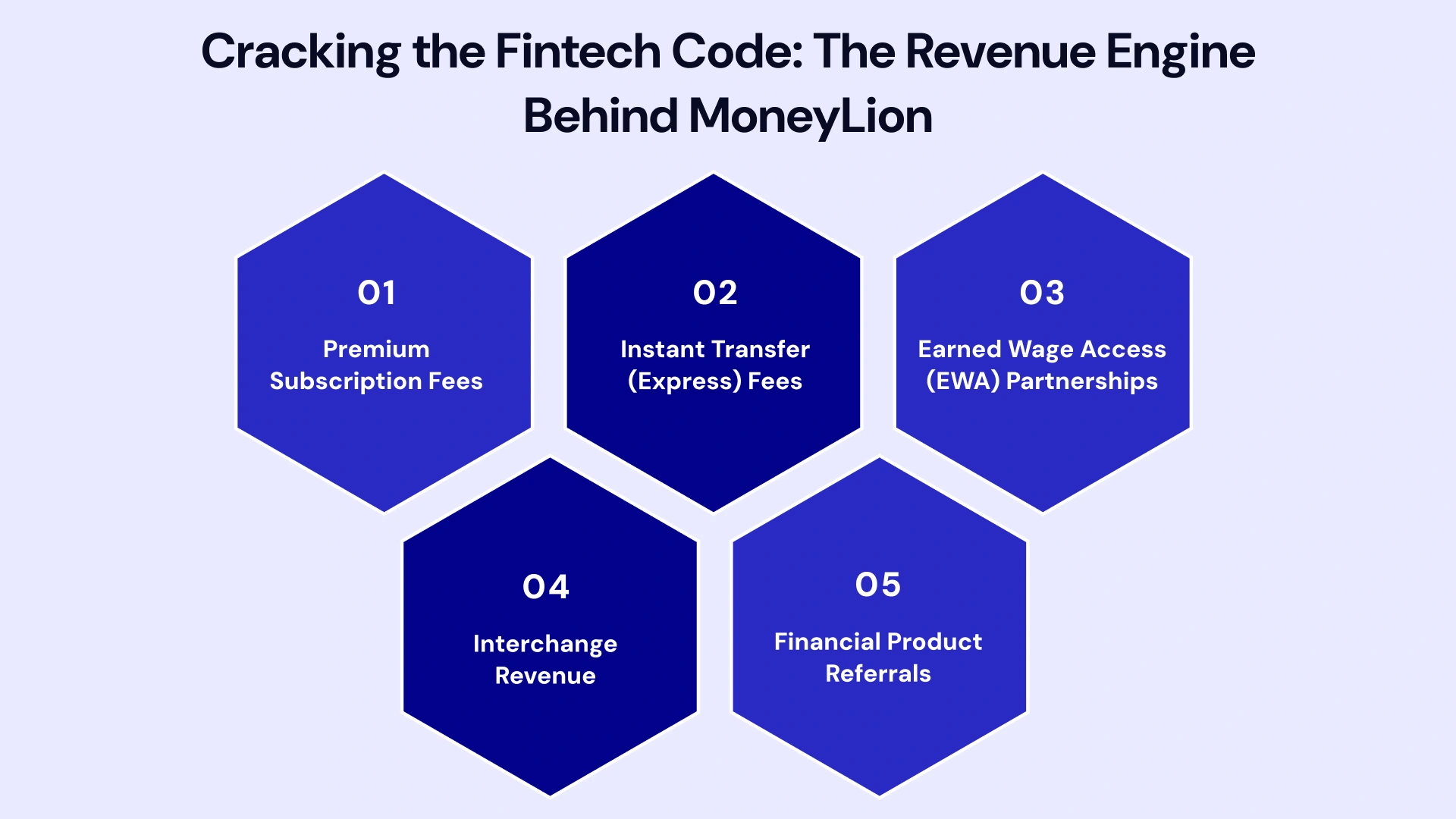

How a Cash Advance App Like MoneyLion Makes Money

Understanding the revenue model is essential before you build — it shapes your feature priorities and compliance requirements. Here are the primary monetisation streams:

1. Premium Subscription Fees

MoneyLion's $19.99/month Plus membership unlocks higher advance limits, investment tools, and credit monitoring. Subscription revenue is predictable and high-margin. A 2023 study found that over 60% of cash advance app revenue comes from subscription and premium feature fees.

2. Instant Transfer (Express) Fees

Standard ACH disbursements take 1–3 business days. Users pay $2–$9 for same-day or instant transfers. This fee is optional but widely used — most users in a financial digital transformation roadmap emergency choose the paid option.

3. Earned Wage Access (EWA) Partnerships

B2B revenue stream: partner with employers to offer EWA as an employee benefit. The employer or employee pays a small per-advance fee. This model has a lower CAC than B2C and a higher lifetime value.

4. Interchange Revenue

If your app includes a debit card (like MoneyLion's RoarMoney card), you earn interchange revenue — typically 1.2–1.5% of every card transaction — from the card network.

5. Financial Product Referrals

Referring users to personal loans, insurance products, or investment accounts generates affiliate commissions. MoneyLion's marketplace model generates significant revenue from this channel.

US Regulatory Compliance: The Non-Negotiable Cost of Building in America

This is the section most competitors' blog posts skip — and it's the one that will determine whether your app can legally operate in the United States.

CFPB Earned Wage Access Guidance

In 2024, the Consumer Financial Protection Bureau (CFPB) issued new guidance treating many Earned Wage Access products as consumer credit. This means your app's terms, fee disclosures, and repayment mechanisms must comply with truth-in-lending standards. Engage a fintech attorney before writing a single line of code.

State Money Transmitter Licenses

If your app transfers money — which cash advance apps inherently do — you likely need a money transmitter license in each state where you operate. Licensing takes 3–12 months per state and costs $1,000–$5,000 in application fees plus surety bonds of $10,000–$500,000, depending on the state.

Strategy: Launch in states with simpler licensing first (Texas, Wyoming, Montana), then expand. Use a licensed partner (like a bank sponsor) to accelerate multi-state launch.

PCI DSS Compliance

Any app that processes, stores, or transmits cardholder data must comply with PCI DSS standards. Level 4 compliance (under 20,000 transactions/year) can be achieved for $5,000–$15,000. As you scale, Level 1 compliance (over 6 million transactions/year) requires a full Qualified Security Assessor (QSA) audit.

The MoneyLion Legal Precedent

In April 2025, the New York Attorney General sued MoneyLion, alleging effective APRs exceeding 350% when fees and tips were factored in (Finder.com, 2026). This case is a critical warning for any fintech founder: your fee structure and disclosure language carry real legal risk. Build your compliance architecture before your product architecture.

How VLink Approaches Fintech App Development

Shivisha Patel, Global Delivery Manager at VLink, has led the delivery of complex financial software projects for insurance carriers and banking clients across the US and Southeast Asia.

Her team's experience with enterprise middleware (WebSphere MQ, IIB), system integration, and regulatory compliance directly informs VLink's fintech software development methodology.

What Makes VLink Different for Cash Advance App Development

- US Compliance-First Architecture: Every fintech engagement begins with a compliance review — not as an afterthought, but as the foundational constraint that shapes the entire system design.

- Agile Delivery with Banking-Grade Security: VLink's sprint-based delivery model includes dedicated security review cycles, ensuring your app maintains PCI DSS alignment through every feature iteration.

- Deep API Expertise: VLink's integration engineers have worked extensively with financial middleware and third-party banking APIs, reducing integration risk on Plaid, Stripe, and eKYC provider connections.

- Transparent Cost Estimation: Unlike development shops that provide a single number and bill overages, our dedicated team provides phase-by-phase cost visibility so your budget never encounters a surprise.

Ready to Build Your Cash Advance App? Here's Your Next Step

The cash advance app market is growing fast — but the window for building a differentiated, compliance-ready product is competitive. The founders and product leads who win in this space are those who invest in building correctly from day one: the right feature scope, the right compliance architecture, and the right development partner.

VLink has delivered custom financial software for US enterprises, insurance carriers, and banking clients for over a decade. Our team understands the regulatory environment your app needs to operate in, the API ecosystem it needs to connect to, and the user experience standards it needs to meet to earn trust in a competitive market.

Get a Free Cash Advance App Development Estimate — Tell us your feature requirements and target launch date. Simply contact us to get started; VLink's fintech team will deliver a detailed, phased cost estimate within 48 hours.

Global Delivery Manager, VLink Inc.

Shivisha Patel serves as the Global Delivery Manager at VLink Inc., bringing a wealth of experience in program delivery and management, particularly in the insurance and banking sectors. She has a robust technical background with deep expertise in WebSphere MQ, WTX, IIB, middleware, and enterprise system integration.

Shivisha Patel

Shivisha Patel