The Banking, Financial Services, and Insurance (BFSI) sector stands at a critical inflection point. Traditional loan processing methods—characterized by lengthy paperwork, manual verification, and weeks-long approval cycles—are rapidly becoming obsolete in an era where customers expect instant gratification.

Enter the loan processing AI chatbot, a transformative technology that's reshaping how financial institutions handle everything from application intake to final disbursement.

For BFSI leaders evaluating digital transformation initiatives, loan processing chatbots represent more than incremental improvement—they offer exponential gains in efficiency, customer satisfaction, and competitive positioning. This comprehensive guide explores how AI-powered chatbots are revolutionizing loan origination, the tangible benefits they deliver, implementation considerations, and the future of conversational AI in lending.

What is a Loan Processing AI Chatbot?

A loan processing AI chatbot is an intelligent virtual assistant that automates and streamlines the entire loan lifecycle—from initial inquiry and application submission through document verification, eligibility assessment, approval, and ongoing servicing. Unlike basic rule-based chatbots that follow predetermined scripts, AI-powered loan chatbots leverage natural language processing (NLP), machine learning, and integration with core banking systems to deliver sophisticated, contextual interactions.

These chatbots operate across multiple channels—website chat widgets, mobile banking applications, WhatsApp, SMS, and even voice-enabled platforms—providing borrowers with seamless, omnichannel experiences. They serve as the digital front door to your lending operations, handling thousands of simultaneous conversations while maintaining personalized engagement with each applicant.

Core Capabilities of Modern Loan Processing Chatbots

- Intelligent Application Intake: Modern AI development services guide applicants through loan applications using conversational interfaces that feel natural and intuitive. Rather than confronting borrowers with lengthy forms, the chatbot asks relevant questions in sequence, explains requirements in plain language, and adapts the conversation flow based on the loan type and applicant responses.

- Document Collection and Verification: AI chatbots can request, receive, and preliminarily verify supporting documentation, including income statements, identity proofs, credit reports, and collateral details. Using optical character recognition (OCR) and document analysis capabilities, they can extract key data points and flag inconsistencies for human review.

- Real-Time Eligibility Assessment: By integrating with credit bureaus, internal databases, and decision engines, chatbots can perform instant pre-qualification checks. They evaluate factors like credit score, debt-to-income ratio, employment stability, and existing relationships to provide immediate feedback on loan eligibility and potential terms.

- Status Tracking and Updates: Borrowers consistently cite a lack of transparency as a major frustration in traditional lending. AI chatbots address this by providing real-time status updates that explain the application's current stage, pending actions, and expected timelines for the next steps.

- Query Resolution and Support: From explaining different loan products to clarifying documentation requirements and addressing specific concerns about terms and conditions, chatbots serve as knowledgeable assistants available around the clock.

The Business Case: Why BFSI Leaders Are Investing in Loan Chatbots

The adoption of loan processing chatbots isn't driven by technological curiosity—it's fueled by compelling business imperatives that directly impact the bottom line and competitive positioning.

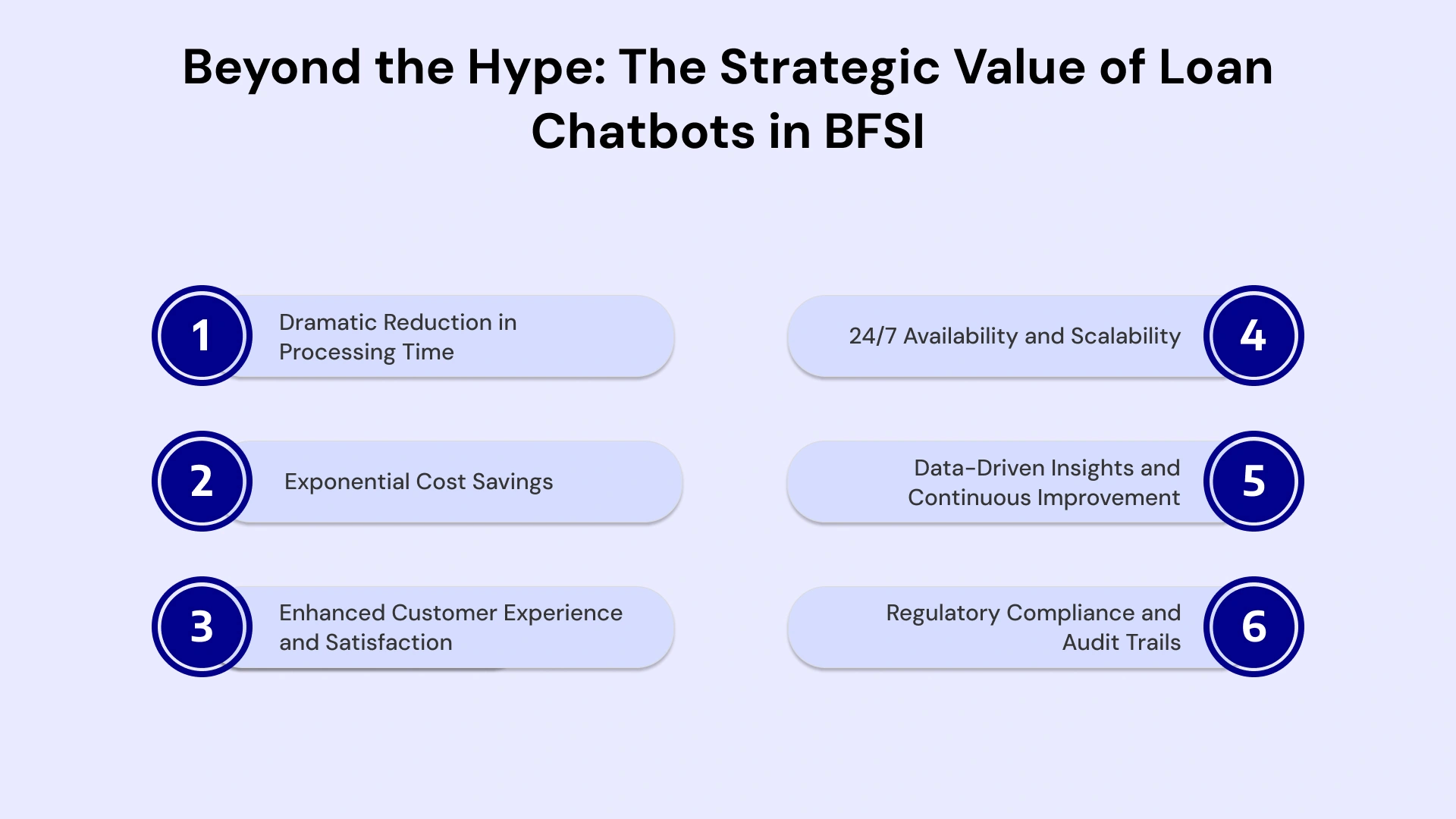

Dramatic Reduction in Processing Time

Traditional loan processing can take anywhere from several days to weeks, involving multiple touchpoints, manual data entry, and sequential handoffs between departments. AI chatbots compress these timelines dramatically. By automating initial screening, document collection, and data validation, chatbots can reduce loan processing time by 60-80% for straightforward applications.

For small business lending, where speed often determines whether an entrepreneur can seize a time-sensitive opportunity, this acceleration provides tremendous value. Personal loan applicants, too, increasingly expect instant or same-day decisions that only automation can deliver at scale.

Exponential Cost Savings

The economics of chatbot deployment are compelling. While a human loan officer can handle 10-15 applications daily, a single chatbot can manage thousands of concurrent conversations without fatigue, errors, or variation in service quality. Industry data suggests that chatbots can reduce customer service costs by up to 30%, with even greater savings in high-volume consumer lending segments.

Beyond direct labor savings, chatbots reduce costs associated with errors and rework. Manual data entry mistakes, missing documentation, and incomplete applications create significant operational drag. Automated validation and guided data collection minimize these inefficiencies.

Enhanced Customer Experience and Satisfaction

Today's borrowers, particularly millennials and Gen Z customers who will dominate the market for decades to come, have been conditioned by experiences with companies like Amazon, Netflix, and Uber to expect frictionless, instant service. A loan application process requiring branch visits, physical paperwork, and opaque waiting periods feels archaic by comparison.

Chatbots meet customers where they are—on their smartphones, at times convenient to them—and provide immediate engagement. The conversational interface reduces intimidation factor, especially for first-time borrowers who may feel overwhelmed by financial jargon and complex requirements. Real-time guidance and instant feedback create a sense of progress and control that traditional processes lack.

24/7 Availability and Scalability

Branch-based and phone-based lending operations face inherent constraints—business hours limit when customers can initiate applications. Seasonal demand surges—such as year-end consumer lending spikes or agricultural loan cycles—require costly staffing adjustments. Chatbots eliminate these limitations, providing consistent service quality regardless of time, day, or volume.

This availability particularly benefits working professionals who can't easily visit branches during business hours, as well as customers in different time zones or rural areas with limited branch access.

Data-Driven Insights and Continuous Improvement

Every chatbot interaction generates valuable data—where applicants struggle, which questions confuse them, at what point they abandon applications, and what objections they raise. This intelligence allows continuous refinement of both the chatbot experience and underlying loan products.

Machine learning capabilities mean chatbots become progressively more effective at understanding intent, providing relevant information, and guiding successful applications.

Regulatory Compliance and Audit Trails

Financial services operate under stringent regulatory frameworks requiring complete documentation, consistent application of policies, and protection of consumer data. Properly designed chatbots excel at compliance.

They apply decisioning criteria uniformly, create comprehensive audit trails of every interaction, ensure required disclosures are delivered consistently, and flag potential fair lending concerns.

Key Use Cases: How Loan Processing Chatbots Add Value Across the Lending Lifecycle

The versatility of AI chatbots allows them to deliver value across multiple touchpoints in the lending journey.

Loan Origination and Application

This is the most impactful use case. Chatbots guide prospective borrowers from initial inquiry through completed application submission. They qualify leads by asking relevant questions, explaining different loan products, and helping customers select the best fit, collecting required information and documentation, performing preliminary eligibility checks, and providing instant feedback on the likelihood of approval.

For banks offering multiple loan products—mortgages, auto loans, personal loans, business loans—a single chatbot can intelligently route conversations and adjust its approach based on the product type and customer profile.

Pre-Qualification and Eligibility Assessment

Before customers invest time in full applications, chatbots can perform quick pre-qualification assessments. By asking a few key questions—such as income, employment status, credit score range, and existing debts—the bot can provide immediate guidance on eligibility and likely terms.

This transparency prevents wasted effort on applications unlikely to succeed and allows customers to take corrective actions (like paying down debts or disputing credit report errors) before formally applying.

Document Collection and Verification

Gathering complete, accurate documentation represents a significant bottleneck in traditional lending. Chatbots streamline this by clearly explaining what documents are needed and why, providing secure upload mechanisms directly within the chat interface, using OCR to extract data from uploaded documents and pre-fill application fields, flagging missing or illegible documents immediately rather than after days of processing, and integrating with e-signature platforms for required authorizations.

Loan Status Tracking and Communication

Once an application is submitted, customers want transparency about progress. Chatbots serve as always-available status dashboards, answering questions like "What stage is my application at?" and "When can I expect a decision?" They proactively notify customers when additional information is needed, when approvals are granted, and when funds will be disbursed. This reduces the volume of status inquiry calls, alleviating contact center overload while increasing customer satisfaction.

Loan Servicing and Payment Management

The chatbot's value doesn't end at origination. Throughout the life of the loan, chatbots can answer questions about payment schedules and outstanding balances, process payment arrangements and extensions, explain payoff amounts and early repayment options, assist with refinancing inquiries, and handle routine service requests like statement generation or payment confirmation.

Cross-Sell and Upsell Opportunities

By analyzing customer data and conversation context, chatbots can identify relevant cross-sell opportunities. A customer checking their auto loan balance might be a good prospect for insurance products. Someone who successfully paid off a personal loan might be ready for a higher credit limit or mortgage pre-qualification. The chatbot can introduce these opportunities naturally without the pressure of a sales conversation.

Technical Architecture: What Powers a Loan Processing Chatbot

Understanding the technical foundations helps BFSI leaders make informed decisions about chatbot platforms and implementation approaches.

Natural Language Processing and Understanding

At the heart of any effective chatbot lies sophisticated NLP that enables the system to comprehend user intent despite variations in phrasing, spelling errors, or incomplete information. Modern NLP engines can understand that "How much can I borrow?", "What's my loan limit?", and "Maximum loan amount?" all express the same intent.

They can extract entities such as loan amounts, property values, and income figures from natural language and handle contextual nuances in which the meaning of "it" or "that" depends on prior exchanges.

Machine Learning and Continuous Improvement

Initial chatbot training requires substantial effort—defining intents, creating training phrases, and building conversation flows. However, machine learning services enable the system to improve continuously.

As the chatbot encounters new phrasings, edge cases, and user behaviors, it can either automatically incorporate this learning or flag them for human trainers to review and add to the training corpus. Over time, accuracy and effectiveness improve substantially.

Integration with Core Banking Systems

A chatbot disconnected from your loan origination system, core banking platform, and document management system provides limited value. Robust integrations are essential for pulling customer data to personalize conversations, submitting completed applications directly into loan processing workflows, retrieving real-time application status and decisioning outcomes, and updating records based on chatbot interactions.

APIs typically facilitate these integrations, though some financial institutions use middleware platforms to orchestrate connections between chatbots and legacy systems that lack modern API capabilities.

Security and Compliance Frameworks

Financial services chatbots must meet rigorous security standards. This includes end-to-end encryption of all conversations and data transmission, secure authentication mechanisms to verify customer identity, role-based access controls that limit what data the chatbot can access, comprehensive logging and audit trails of all interactions, and compliance with regulations such as GDPR, CCPA, and financial services-specific requirements.

Many financial institutions deploy chatbots in private cloud or on-premises environments rather than public cloud to maintain greater control over sensitive data.

Multi-Channel Deployment Capabilities

Modern customers interact with financial institutions across multiple channels. Leading chatbot platforms support deployment across website chat widgets, mobile banking applications, messaging platforms like WhatsApp and Facebook Messenger, SMS for text-based interactions, and voice assistants for hands-free engagement. The underlying AI remains consistent while the interface adapts to each channel's unique characteristics.

Implementation Roadmap: How to Successfully Deploy a Loan Processing Chatbot

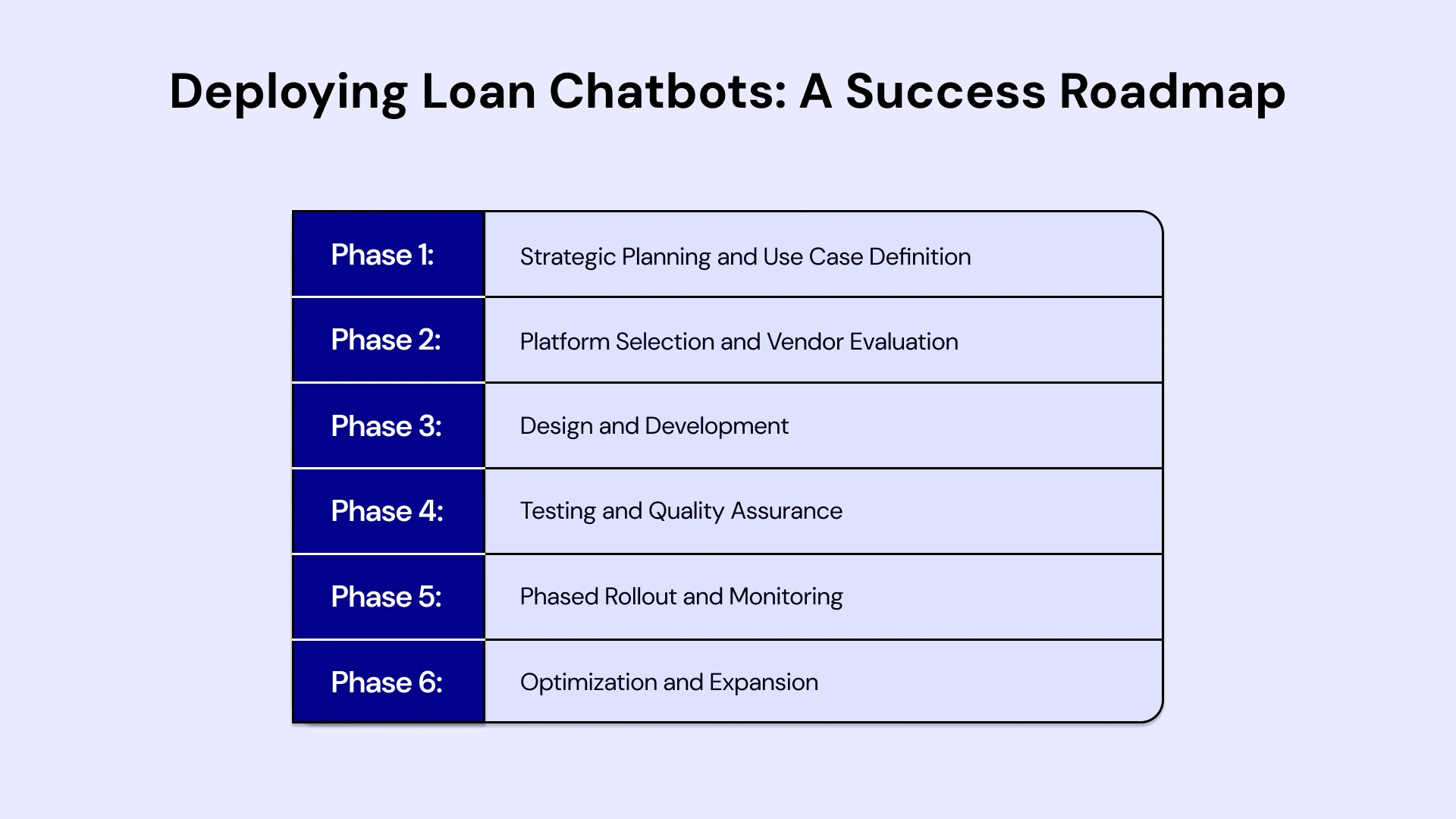

Deploying an AI-powered loan processing chatbot requires a balance between user speed and the institution's strict compliance requirements. A successful rollout typically comprises six distinct phases.

Phase 1: Strategic Planning and Use Case Definition

Begin by identifying the specific problems you're solving and outcomes you're targeting. Are you primarily focused on reducing processing time, improving customer experience, or handling volume growth without proportional staff increases? Different priorities suggest different initial use cases.

Conduct stakeholder interviews across loan operations, customer service, IT, compliance, and marketing to understand pain points and requirements. Map current loan processing workflows to identify bottlenecks and opportunities where automation can deliver maximum impact.

Define success metrics upfront—application completion rates, time to decision, customer satisfaction scores, cost per loan originated, and containment rates (percentage of inquiries resolved without human intervention).

Phase 2: Platform Selection and Vendor Evaluation

The chatbot platform market offers numerous options, from comprehensive enterprise platforms to specialized lending solutions. Evaluation criteria should include NLP capabilities and accuracy for financial services terminology; pre-built integrations with banking systems and document verification services; security and compliance certifications; scalability to handle your anticipated conversation volumes; customization flexibility to match your brand voice and processes; analytics and reporting capabilities; and vendor stability and support quality.

Consider whether to build using a platform-as-a-service approach, partner with a specialized chatbot development company, or leverage solutions from existing technology vendors in your ecosystem.

Phase 3: Design and Development

Effective chatbot design balances automation with recognition of when human intervention adds value. Best practices include creating conversation flows that feel natural rather than robotic, building in empathy, especially when delivering disappointing news like application denials, providing clear escalation paths to human agents when needed, designing for inclusion, considering users with different literacy levels and language preferences, and incorporating your brand personality while maintaining professionalism.

Development typically follows agile methodologies with iterative sprints, allowing continuous testing and refinement. Extensive training of the NLP engine using realistic customer phrases and questions is critical.

Phase 4: Testing and Quality Assurance

Rigorous testing before launch prevents embarrassing failures and compliance breaches. Test scenarios should include functional testing of all conversation paths and integrations, stress testing to ensure performance under high concurrent load, security penetration testing, compliance review to verify required disclosures and fair lending practices, and user acceptance testing with actual customers or representative users.

Create a "red team" that deliberately tries to confuse the chatbot, extract inappropriate information, or trigger errors to identify and fix vulnerabilities.

Phase 5: Phased Rollout and Monitoring

Rather than immediately exposing the chatbot to all customers, consider a phased approach: a limited pilot with friendly customers or internal users; gradual expansion to broader customer segments while monitoring performance; concurrent operation with existing channels initially rather than replacement; and progressive handover of additional use cases as confidence grows.

Establish real-time monitoring dashboards that track key metrics and alert teams to anomalies. Create feedback mechanisms allowing users to rate chatbot interactions and escalate issues.

Phase 6: Optimization and Expansion

Post-launch optimization should be continuous, not a one-time activity. Regularly analyze conversation logs to identify confusion points, frequently asked questions the chatbot handles poorly, and opportunities to expand capabilities. Refine NLP training based on real user language patterns. Measure business outcomes against initial success criteria and adjust as needed.

As initial use cases mature, expand the chatbot's scope to additional loan products, deeper functionality, or related processes such as customer onboarding or account management.

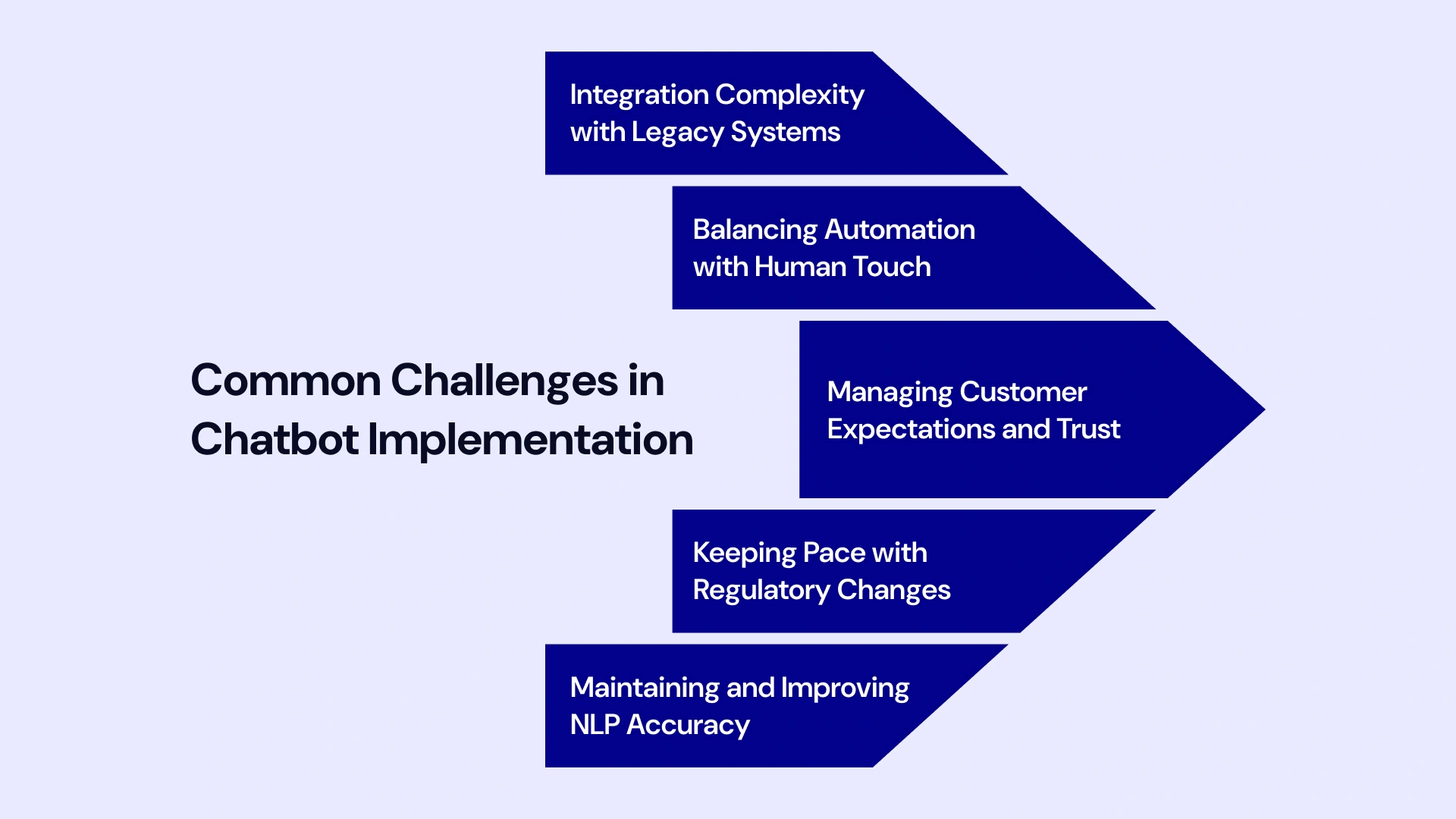

Overcoming Common Challenges in Chatbot Implementation

Despite the compelling benefits, chatbot projects can stumble. Understanding common pitfalls allows proactive mitigation.

Integration Complexity with Legacy Systems

Many financial institutions operate on decades-old core banking systems never designed for modern API-based integrations. Establishing reliable, secure connections between chatbots and these legacy platforms can be technically challenging and time-consuming.

Solutions include implementing middleware or integration platforms, using screen scraping or robotic process automation as interim bridges, prioritizing systems modernization initiatives, and designing chatbots that can provide value even with limited initial integration.

Balancing Automation with Human Touch

Over-automation can create frustrating experiences when customers need empathy, complex problem-solving, or exceptions to standard policies. Conversely, excessive reliance on human handoffs negates much of the chatbot's value.

The optimal balance involves defining clear escalation triggers, ensuring seamless handoffs with full context transfer, empowering human agents with AI-assisted recommendations, and continuously refining which interactions benefit most from automation versus human judgment.

Managing Customer Expectations and Trust

Customers may be skeptical about interacting with AI for something as important as loan applications. Building trust requires transparency about when they're interacting with a bot versus a human, demonstrating competence through accurate, helpful responses, providing easy access to human support when needed, protecting privacy and explaining how data is used, and showcasing security measures protecting their information.

Keeping Pace with Regulatory Changes

Financial services regulations evolve constantly. Chatbots must adapt quickly to new disclosure requirements, fair lending standards, and consumer protection rules. Strategies include building compliance review into the chatbot governance process, maintaining flexibility to update conversation flows rapidly and disclosures, documenting chatbot decision logic for regulatory examination, and establishing clear accountability for ongoing compliance monitoring.

Maintaining and Improving NLP Accuracy

Even well-trained chatbots occasionally misunderstand user intent, especially with ambiguous phrasing, domain-specific jargon, or emotional language. Continuous improvement requires dedicated resources to analyze misclassifications and edge cases, expand training data with real customer language patterns, implement confidence thresholds that trigger clarifying questions, and provide feedback mechanisms that allow customers to correct misunderstandings.

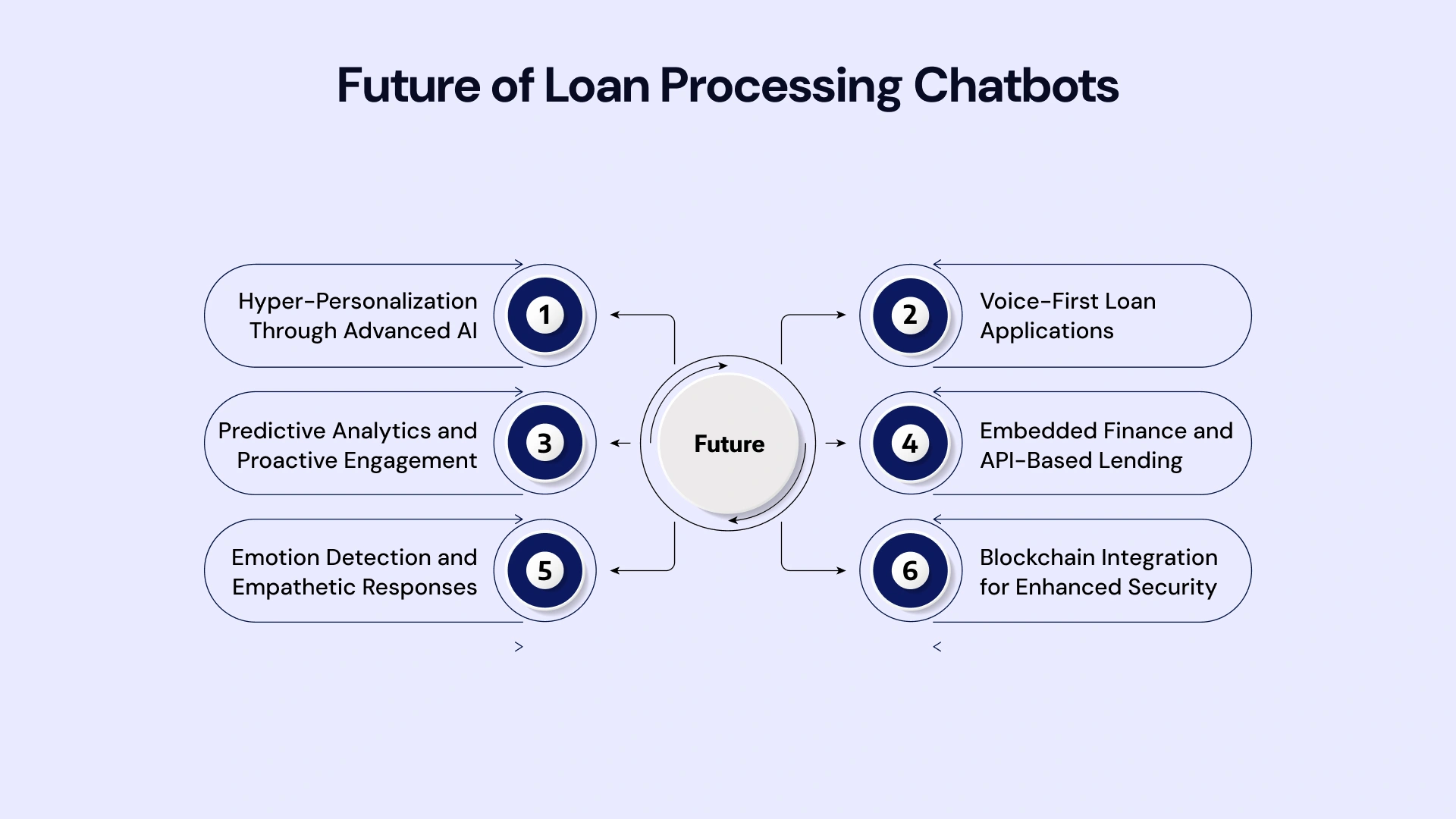

The Future of Loan Processing Chatbots: Emerging Trends

The chatbot landscape continues evolving rapidly. Forward-thinking BFSI leaders should monitor several emerging trends.

Hyper-Personalization Through Advanced AI

Next-generation chatbots will leverage comprehensive customer data—transaction history, life events, financial goals, interaction patterns—to deliver unprecedented personalization. Rather than generic loan recommendations, chatbots will proactively suggest financing options aligned with the customer's specific circumstances and timing.

Voice-First Loan Applications

As voice assistants like Alexa and Google Assistant become ubiquitous, voice-enabled loan chatbots will allow customers to initiate and complete applications entirely through conversational speech. This dramatically lowers barriers for customers who find typing on mobile devices cumbersome.

Predictive Analytics and Proactive Engagement

Rather than waiting for customers to inquire about loans, AI chatbots will identify signals of borrowing needs—such as upcoming major purchases, business expansion indicators, and seasonal cash flow patterns—and proactively reach out with relevant offers. This shifts lending from reactive to anticipatory.

Embedded Finance and API-Based Lending

Chatbots will increasingly appear not just on bank websites but embedded in e-commerce platforms, accounting software, and other contexts where customers naturally encounter financing needs. A small business owner using QuickBooks might interact with a chatbot offering working capital loans without leaving their accounting software.

Emotion Detection and Empathetic Responses

Advanced sentiment analysis will enable chatbots to detect frustration, confusion, or anxiety in customer messages and adjust their tone and approach accordingly. A customer expressing stress about potential loan denial might receive more empathetic language and information about alternative options or financial counseling resources.

Blockchain Integration for Enhanced Security

Some financial institutions are exploring blockchain-based identity verification and document attestation integrated with chatbot workflows. This could dramatically reduce fraud while streamlining verification processes.

Real-World Success Stories

Examining how peers have successfully deployed loan chatbots provides valuable insights. Let’s explore a few case studies.

Case Study: Regional Bank Reduces Loan Processing Time by 65%

A mid-sized regional bank serving small businesses implemented an AI chatbot to streamline commercial loan applications. Previously, the initial application and document collection process took an average of 11 days. The chatbot automated initial qualification, guided business owners through application completion, and collected financial documents and verification.

Results after six months showed application completion time reduced to four days on average, customer satisfaction scores increased by 28 percentage points, loan officers freed to focus on relationship building and complex applications, and application volume increased by 40% with no staff additions.

Case Study: Digital Lender Achieves 24/7 Personal Loan Availability

An online personal lending platform deployed a WhatsApp chatbot that allows customers to apply for loans entirely via messaging. The conversational interface asked questions about employment, income, and loan purpose while explaining eligibility criteria and required documentation.

Outcomes included 78% of applications completed entirely through the chatbot without human intervention, an average application time of 12 minutes compared to 45 minutes for web forms, 60% of applications initiated outside business hours, and a Net Promoter Score improvement from 42 to 68.

Scale Your Business with Custom AI Chatbots by VLink

VLink delivers tailored AI chatbot development solutions designed specifically for the complex landscape of banking and financial services (BFSI). We combine deep industry knowledge with technical excellence to automate your lending operations.

Why Choose VLink?

- BFSI Domain Expertise: Proven experience with banks, credit unions, and fintechs, ensuring compliance with strict regulatory requirements.

- End-to-End Development: We manage the entire lifecycle—from initial strategy and natural language processing (NLP) training to core banking integration and security architecture.

- Custom-Built Solutions: We avoid "off-the-shelf" limitations, building chatbots tailored to your specific loan products and brand voice.

- Measurable Results: Our implementations typically deliver a 60–75% reduction in processing time and a 2–3x increase in application completion rates.

Our Streamlined Process

1. Discovery: Identifying high-impact use cases and success metrics.

2. Design: Mapping conversational flows and integration architecture.

3. Agile Development: Iterative building with frequent functional updates.

4. Integration & Testing: Connecting to credit bureaus and core systems with rigorous security audits.

5. Deployment & Optimization: Seamless launch followed by continuous NLP refinement based on real-world data.

Partner with VLink to Transform Your Operations

AI chatbots are no longer a novelty; they are a strategic necessity for financial institutions. By delivering 24/7, frictionless loan experiences, early adopters are already achieving significant cost savings, faster processing, and higher customer satisfaction.

To remain competitive, BFSI leaders should:

- Act Now: Identify high-impact use cases, such as personal or small business lending, for a focused pilot.

- Partner Wisely: Work with expert partners like VLink who balance technical innovation with strict banking security and compliance.

- Focus on Growth: Transition from manual processes to scalable, conversational AI services to capture market share and deepen customer loyalty.

Ready to reduce loan processing times, delight customers with instant service, and scale your lending operations efficiently? Contact VLink today to discuss your vision and see how our expertise can turn your chatbot strategy into a reality.

Vice President, Strategy – VLink Inc.

Sambhavi Gopalakrishnan is the Vice President of Strategy at VLink Inc., bringing over a decade of experience in IT leadership, project implementation, and strategic growth. She possesses a strong foundation in technical project management and pre-sales, driving innovation and business transformation at VLink.

Shivisha Patel

Shivisha Patel