Artificial intelligence (AI) for lending has moved from pilot projects to production-critical infrastructure in 2026. AI in lending software is helping banks, credit unions, fintechs, and NBFCs cut loan decision times from days to minutes, reduce operational costs by up to 20–70%, and increase fraud detection accuracy by over 80% in some deployments.

This comprehensive blog explains how AI for lending is reshaping credit decisions, underwriting, and loan servicing; what trends will define AI-powered commercial lending software in 2026; and how to implement AI lending automation responsibly, with strong AI governance for lenders and fair lending AI compliance in mind.

AI streamlines mortgage processing—AI for mortgage workflows includes document verification, underwriting, and fraud detection.

For teams comparing scope and budget, Lendo-style investment app development cost offers useful direction for planning timelines, resources, and delivery expectations.

What is AI in Lending in 2026?

AI in lending refers to using machine learning, advanced analytics, and generative AI to automate and optimize credit decisioning, underwriting, loan servicing, and fraud detection across the lending lifecycle. AI in lending software can process structured and unstructured data in real time, deliver explainable credit-scoring automation, and orchestrate workflows that previously relied on manual review and siloed systems. This shift is what defines modern AI-powered lending.

Modern AI-powered lending platforms integrate a suite of advanced components:

- AI credit scoring software and AI underwriting software that analyze applicant data far beyond traditional FICO scores.

- AI loan origination system (LOS) components for intake, KYC, and rapid decisioning, enhancing the automated underwriting system's functionality.

- AI risk assessment software and robust AI fraud detection capabilities for lending.

- AI-driven loan servicing tools for collections, restructuring, and portfolio analytics.

- Agentic AI for lending that can act as an intelligent assistant or a real-time fraud-detection agent.

This new generation of AI lending software for financial inclusion enables lenders to reach new customer segments, including thin-file and underbanked borrowers, while maintaining risk, compliance, and capital efficiency. It is the core of how AI is used in lending today.

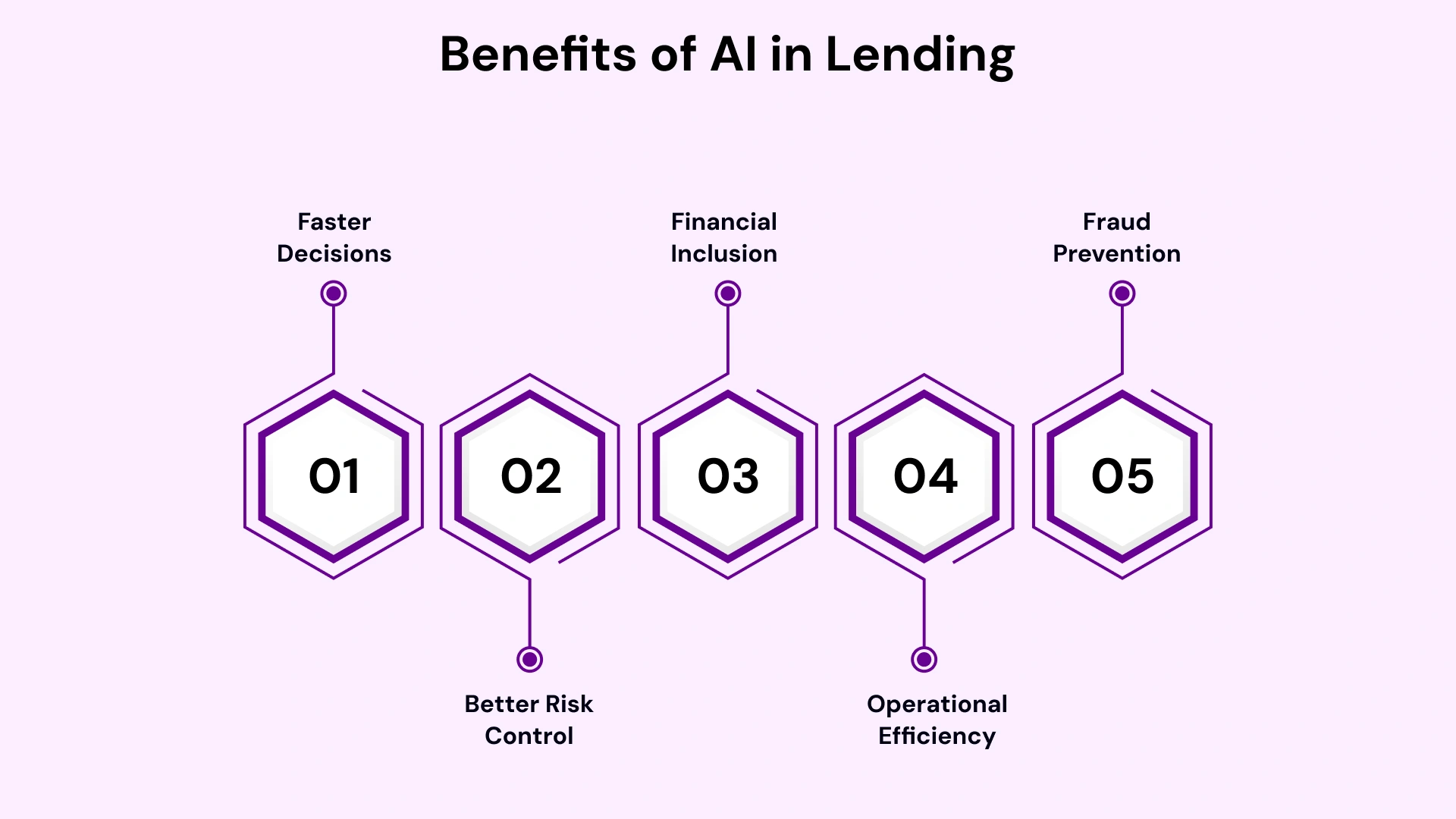

Why AI for Lending is Now Mission-Critical

For US and Canadian lenders, AI-powered lending is about three strategic priorities: speed, risk, and inclusion. The adoption of AI in fintech solutions has accelerated, turning incremental improvements into fundamental competitive advantages.

Key benefits of AI in lending and AI lending automation include:

- Faster Decisions: AI loan approval engines and automated underwriting system components can reduce decision times by 10–25x, moving from days to near-instantaneous, while maintaining or improving risk quality. This is the power of AI for loan approvals.

- Better Risk Control: AI credit-scoring models for NBFCs and banks can incorporate thousands of variables, enabling more accurate default predictions and sophisticated risk-based loan-pricing strategies. This is critical for AI risk assessment software.

- Financial Inclusion: AI-powered credit decisioning engine platforms leverage alternative data for credit underwriting to approve more creditworthy borrowers without increasing defaults, supporting the goal of AI lending software for financial inclusion.

- Operational Efficiency: AI-driven loan servicing, AI workflow automation for lending, and AI lending automation help reduce manual work by automating tasks such as document processing, lowering cost-to-serve, and enabling digital self-service.

- Fraud Prevention: AI fraud detection for lending and a real-time fraud detection agent can detect anomalies across massive datasets far faster and more accurately than traditional, rule-based systems.

In other words, the benefits of AI in lending go beyond incremental optimization. AI for digital lending allows lenders to redesign products, processes, and customer journeys for an always-on, data-driven, and highly personalized experience. The future of AI in banking rests on these foundational capabilities.

Pro Tips:-

The EU AI Act has officially categorized credit scoring as "High-Risk AI." In 2026, you cannot deploy a lending model that cannot explain its decision. This includes:

- Explainability (XAI): For every rejected loan application, generate a "Model Card" detailing the specific weights (e.g., debt-to-income vs. payment history) that led to the decision.

- Audit Trails: Institutions must maintain 10-year logs of training data to demonstrate that no "proxy variables" (e.g., location as a proxy for race) influenced the AI.

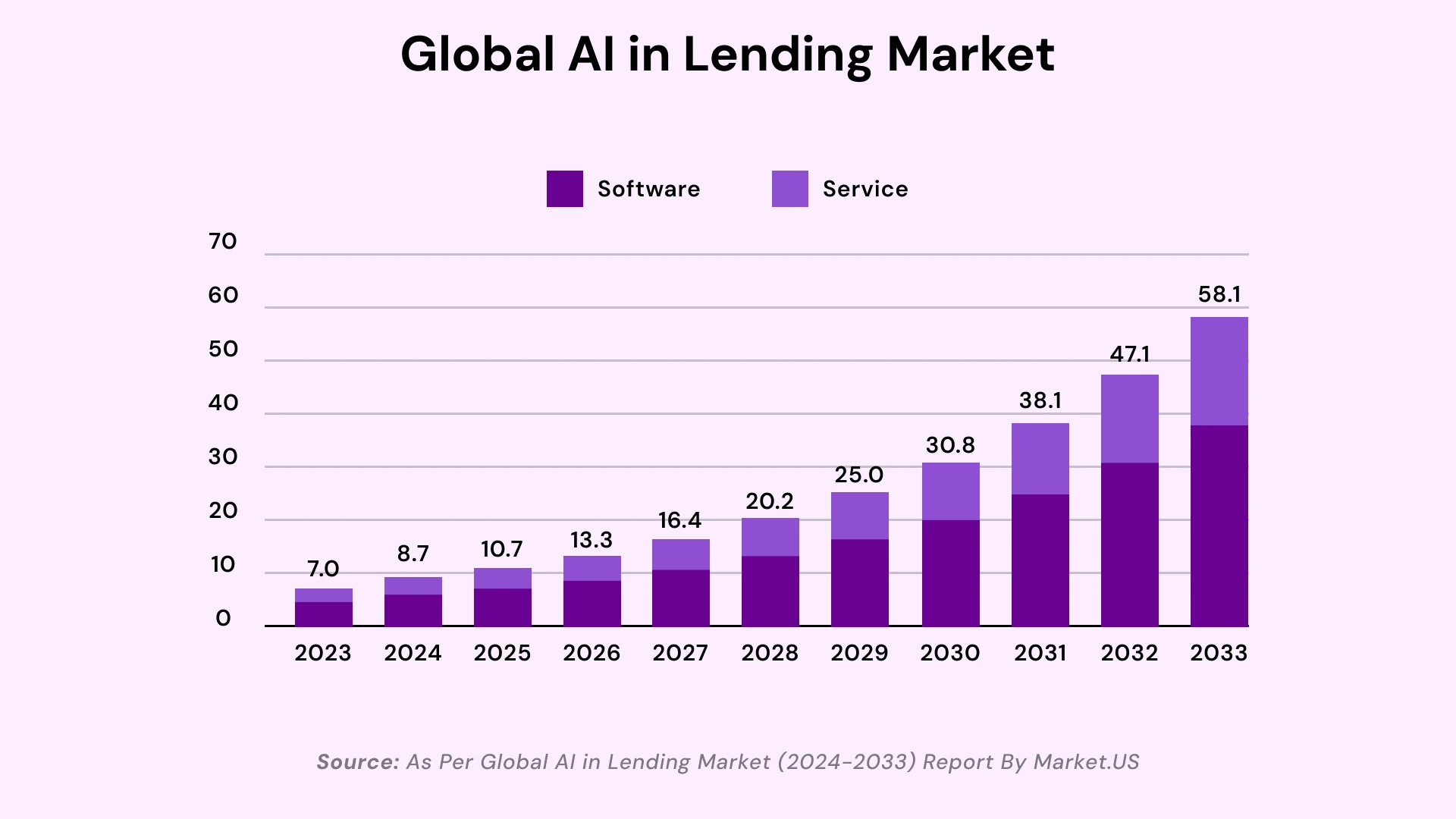

Market Outlook: AI-Powered Lending in North America

The AI in the lending market is expanding rapidly as lenders prioritize modernizing decision engines and revamping legacy loan systems. North America is at the forefront of this transformation.

These trends of AI in lending demonstrate that AI in lending and AI in banking are converging: AI in lending software is becoming a core building block in digital banking, embedded finance, and BNPL ecosystems.

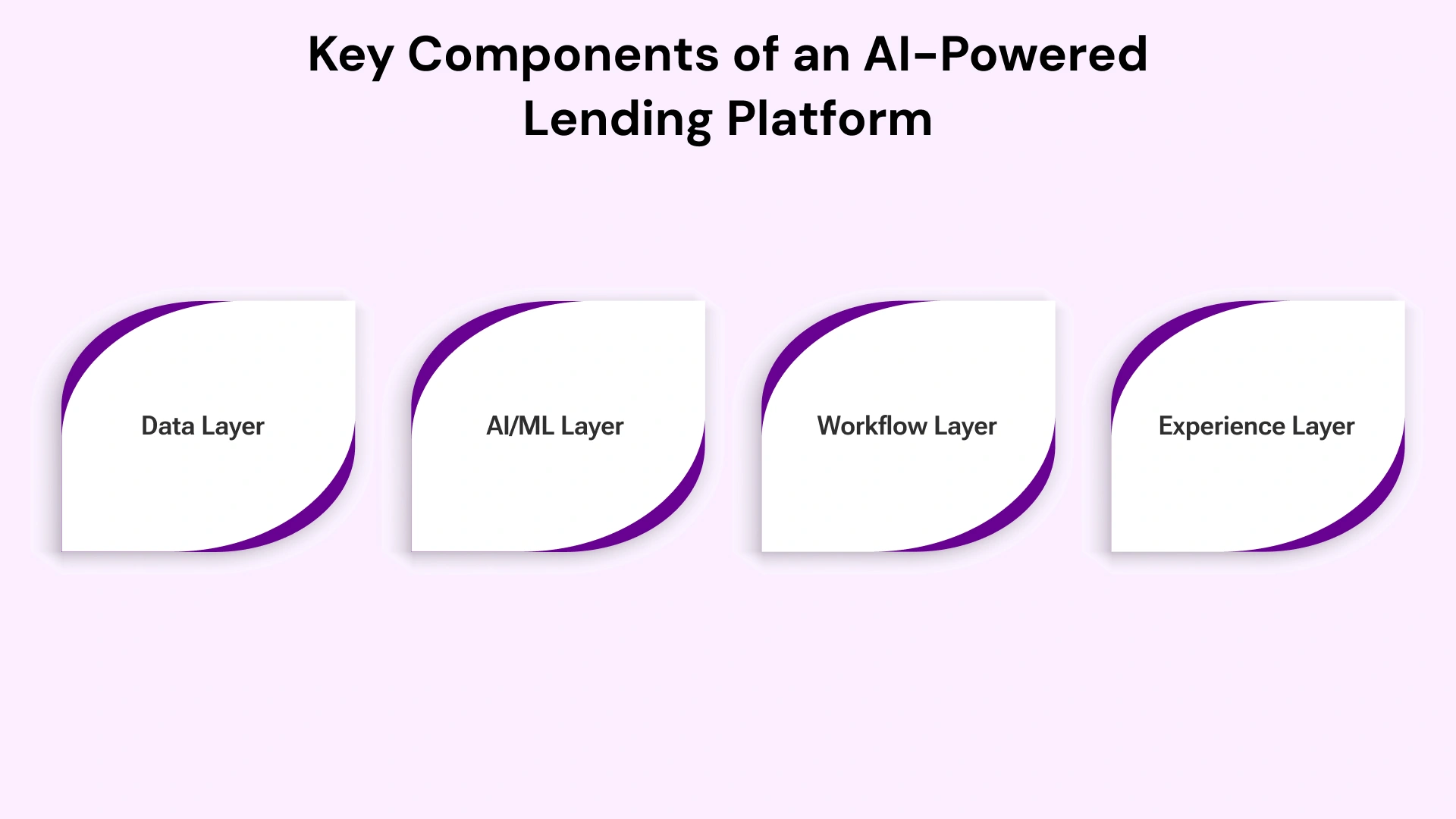

Core Components of an AI-Powered Lending Platform

An effective AI lending platform brings together multiple AI for lending modules into an end-to-end architecture. When assessing the best AI software for lending or planning decision engine modernization, focus on these critical layers:

1. Data Layer

- Function: Ingests and harmonizes data from core banking, AI loan origination systems, CRM, credit bureaus, open banking APIs, accounting systems, and diverse alternative data for credit underwriting sources. This is the fuel for every AI lending automation process.

2. AI/ML Layer

- Function: Hosts the proprietary models, including AI credit scoring software, AI underwriting software, AI risk assessment software, and the central machine learning lending platform models for default, fraud, and pricing prediction. This is where AI-powered credit decisioning engine platforms live.

3. Workflow Layer

- Function: Orchestrates AI lending automation and AI workflow automation for lending, including automated loan underwriting AI solutions, document verification, and AI-driven loan servicing workflows. It ensures straight-through processing for most applications.

4. Experience Layer

- Function: Exposes AI lending platform capabilities through customer portals, mobile apps, and Agentic AI for lending assistants for both borrowers and staff. This layer drives conversion and efficiency.

This architecture supports custom AI lending software tailored to specific products (SME, retail, mortgage) and regulatory environments. Crucially, it provides the framework for strong AI governance for lenders and AI model monitoring for credit to ensure models remain accurate, fair, and compliant over time.

Priority Use Cases of AI in Lending

There are dozens of AI use cases for lending, but some deliver robust ROI and fast implementation. These are the areas where AI in lending software provides the quickest competitive lift.

Top examples of AI for lending include:

- Accelerated Credit Decisioning: Implementing AI loan approval and sophisticated AI for loan approvals that can process an application in seconds.

- Enhanced Scoring: Deploying AI credit scoring models for NBFCs and banks that leverage alternative data for credit underwriting.

- Automated Underwriting: Utilizing automated loan underwriting AI solutions to handle high-volume, low-complexity applications with minimal human intervention.

- Proactive Servicing: Using AI-driven loan servicing and collections to predict early-stage delinquency and automate personalized outreach.

- Advanced Fraud Prevention: Integrating a real-time fraud detection agent and AI fraud detection for lending into the origination and servicing pipelines.

- Process Efficiency: Applying AI lending automation for document processing, KYC validation, and workflow triggers.

These AI lending examples can be implemented individually or as part of a broader AI-powered lending transformation program.

AI Credit Scoring and Alternative Data

Traditional credit scoring relies on a narrow set of bureau data, often leading to a conservative approach that excludes otherwise creditworthy individuals. AI credit scoring software and AI credit scoring models for NBFCs break this limitation by processing richer, more dynamic data streams.

AI in lending software can incorporate

- Cash-flow data from bank statements and accounting systems to assess stability and liquidity.

- Employment and income stability indicators derived from digital records.

- Alternative data for credit underwriting, such as utility payments, rental history, and educational achievement (subject to strict local regulations and fair lending AI compliance).

By embedding AI for lending into credit scoring automation, lenders can:

- Approve more thin-file and near-prime borrowers without increasing default rates, significantly boosting AI lending software for financial inclusion.

- Apply risk-based loan pricing AI strategies that dynamically adjust rates and limits based on a deeper understanding of risk.

In practice, AI-powered lending and AI-powered credit decisioning engines platforms have shown they can approve significantly more loans at lower average interest rates while maintaining—or even improving—risk standards.

AI Underwriting and AI Loan Origination Systems

AI underwriting software and AI loan origination system (LOS) capabilities are central to achieving straight-through processing in AI lending. They connect pre-qualification, application, and decisioning into a single, efficient, AI-powered lending pipeline.

Key capabilities in a modern AI loan origination system include:

- Automated Document Capture: Using AI to perform OCR, data extraction, and validation of documents like pay stubs and tax returns.

- AI Risk Assessment Software: Calculating granular measures like probability of default and loss given default in real time.

- Real-Time Fraud Detection Agent Logic: For real-time fraud detection agents, it instantly flags suspicious profiles, synthetic identities, or manipulated documents.

- AI for Loan Approvals: The engine automatically approves low-risk deals and routes high-risk or complex edge cases to human underwriters with a prioritized queue and necessary data packet.

For lenders asking how banks use AI for underwriting, the answer is increasingly: at every step of the process. AI in fintech platforms is merging with LOS capabilities, enabling AI-powered commercial lending software to support both new originations and subsequent actions, such as limit increases and restructuring. This is the essence of automated loan underwriting AI solutions.

AI-Driven Loan Servicing and Collections

AI-driven loan servicing is a major frontier of AI in lending. Once a loan is booked, intelligent servicing can significantly reduce delinquencies, lower cost-to-serve, and improve customer experience

AI in lending software supports:

- Behavioral Analytics: Models that predict delinquency risk early, allowing for preemptive intervention.

- Agentic AI in Lending: Automated, personalized outreach (email, SMS, chat) for payment reminders, collections, and negotiation workflows.

- Personalized Workouts: Offering tailored restructuring or hardship options via AI lending automation based on the borrower’s risk profile and communication history.

- Scaleable Support: AI-driven loan servicing at scale through intelligent chatbots and self-service portals.

By using AI lending platform analytics to segment borrowers and personalize strategies, lenders can improve recovery rates while significantly enhancing the customer experience—a key differentiator in lending's digital transformation.

AI Fraud Detection for Lending

Fraud is a persistent, evolving threat, especially with the rise of synthetic identities and sophisticated digital scams. AI fraud detection for lending combines supervised and unsupervised machine learning models to analyze applications, transactions, and behavioral patterns in real time. A key component is the real-time fraud detection agent that runs within the application flow.

Capabilities of a modern loan fraud detection solution include:

- Real-Time Fraud Detection Agent Models: Evaluating location, device fingerprints, and behavioral signals against known fraud patterns.

- Document Forgery Detection: Using computer vision and deep learning to spot manipulated identity documents or financial statements.

- Risk-Based Verification: Dynamic triggers within AI in lending to request additional verification only for genuinely high-risk cases, minimizing friction for legitimate customers.

- AI Lending Automation for Investigations: Routing high-risk cases immediately to investigation teams with a full, AI-generated summary of suspicious activity.

An AI loan company or bank using AI-powered lending fraud models can detect anomalies that rule-based systems miss and continuously adapt as criminal patterns change.

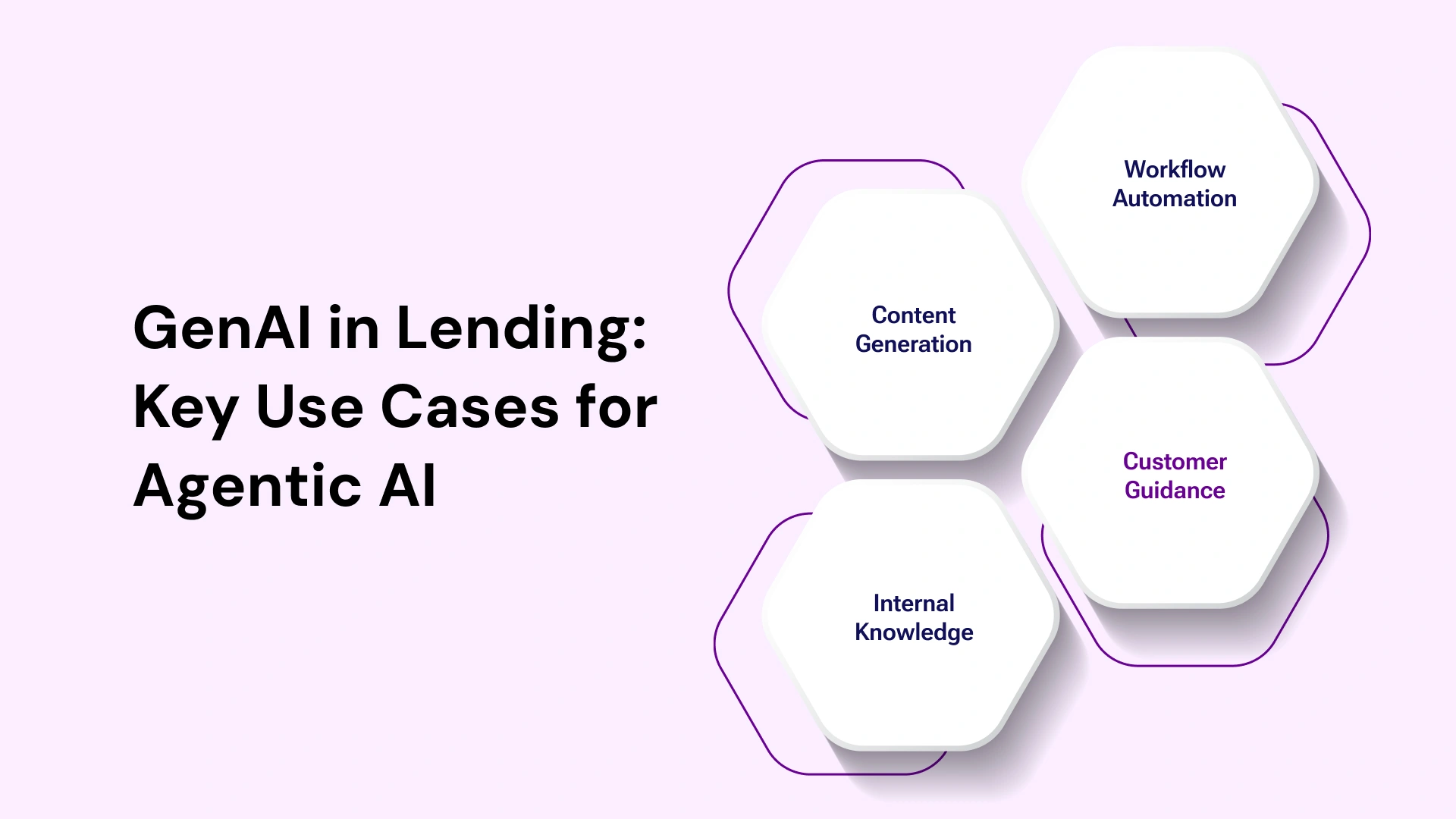

Generative AI and Agentic AI for Lending

Generative AI for lending and Agentic AI for lending are emerging as differentiators in 2026. Unlike traditional AI, which mainly scores or classifies, these models generate content, automate conversational workflows, and orchestrate complex tasks.

Use cases of AI for lending leveraging Generative and Agentic AI:

- Content Generation: Drafting credit memos, decline notices, compliance summaries, and personalized communication templates with generative AI reporting for lending.

- Internal Knowledge: Answering complex questions like "how does DeFi lending work?" or "how to build a loan management system" from internal teams via an internal, secure AI advisor.

- Customer Guidance: Guiding borrowers through complex loan applications or hardship requests as an agentic AI in a lending assistant, capable of coordinating data pulls and document submission.

- Workflow Automation: Agentic AI for lending systems sits on top of AI in lending software to orchestrate multi-step processes, such as reviewing a payment deferral request, checking policy adherence, generating the necessary documents, and updating the core system, all without human intervention.

These agentic AI in lending systems provide contextual, conversational, and action-oriented experiences that feel much closer to working with a human team member, boosting both staff productivity and customer satisfaction.

Responsible AI in Lending and AI Governance

As AI-powered lending grows, regulators in the US and Canada are sharpening expectations for AI compliance in lending and fair lending. Lenders must proactively implement strong, responsible AI in lending practices.

Key areas for compliance and oversight:

- AI Discoverability Bias in Lending: Understanding and mitigating how historical data sources and model design can lead to disparate impact or misrepresent certain protected groups.

- Explainable AI in Lending (XAI): Ensuring every AI-powered credit decision can be interpreted, rationalized, and documented for borrowers, internal risk teams, and regulators.

- AI Governance for Lenders: Defining policies, controls, audit trails, and accountability across the entire model lifecycle, which is essential for AI model governance in BFSI.

- Responsible AI in Lending: Aligning AI with fairness, privacy, and transparency principles beyond simple compliance.

AI governance in BFSI is no longer optional. Lenders need apparent oversight of their AI in fintech solutions, robust AI model monitoring for credit performance and fairness drift, and documented rationales for all AI-powered loan decisions.

Making Loan Products Machine-Readable

To unlock full AI lending automation and achieve genuine decision engine modernization, loan products themselves must become machine-readable. This means encoding terms, conditions, eligibility rules, and pricing logic in a structured, standardized way that AI-powered lending engines can interpret programmatically.

Making loan products machine-readable supports:

- AI Lending Automation: Product selection, eligibility checks, and document generation are automated based on structured product logic.

- Consistent Decisions: Ensures the same product rules are applied consistently by the AI-powered credit decisioning engine platforms every time.

- Faster Integration: Enables easier, faster integration between AI lending software, core banking, and external channels.

- Risk-Based Pricing: Enables the system to execute highly granular, risk-based loan pricing AI instantly.

For an AI banking software development company or an AI development company, this machine-readable design is a critical pattern to adopt when building custom AI lending software.

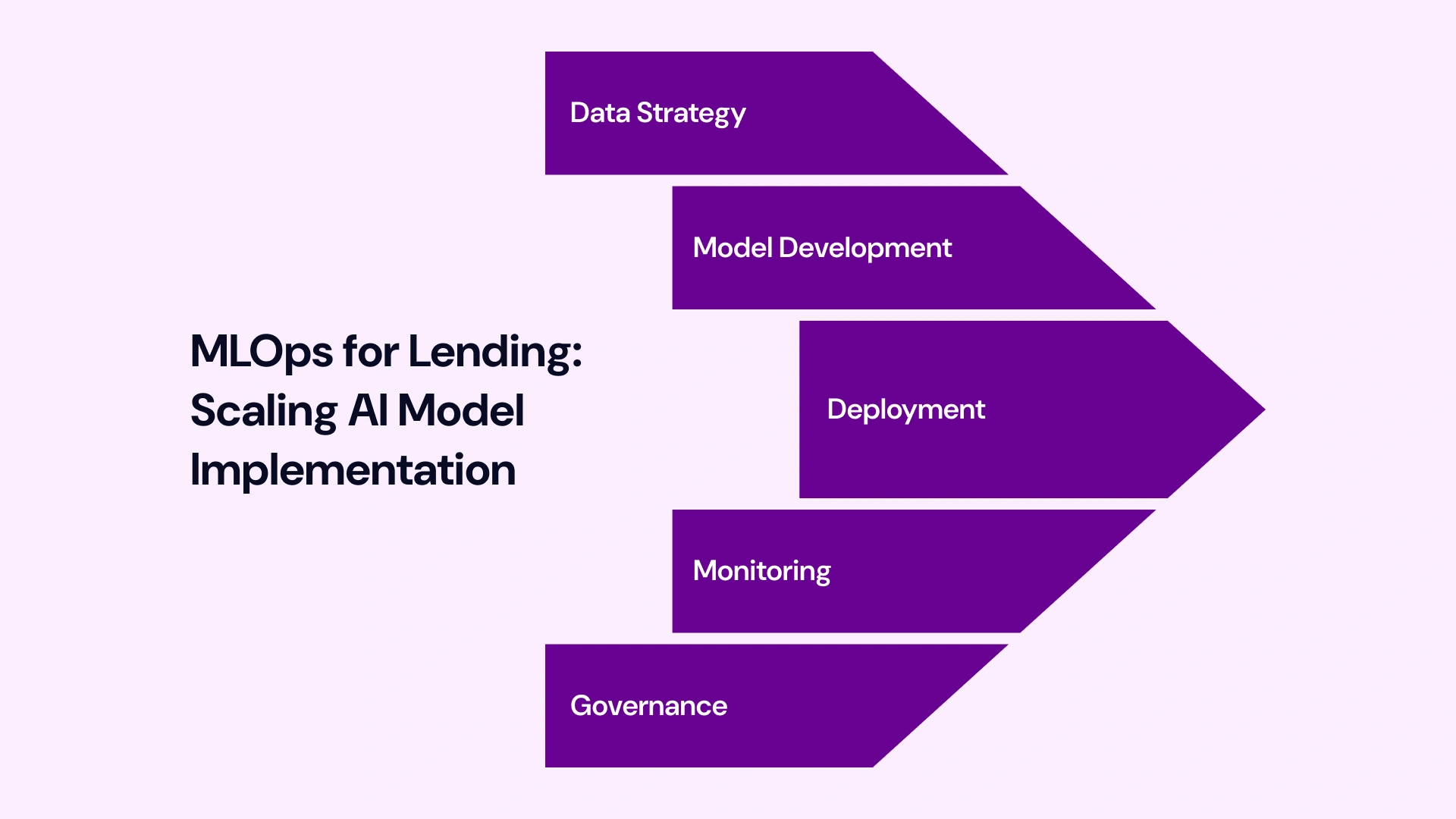

Implementing AI Lending Models and MLOps for Lending

Implementing AI lending models requires more than just training a few algorithms; it demands a robust operational framework. Successful lenders invest in MLOps for lending models to manage deployment, monitoring, and ongoing updates.

Key steps for deploying AI for lending at scale:

1. Data Strategy: Define the data your AI in lending software will use, including both internal data and alternative data for credit underwriting.

2. Model Development: Work with AI development services or an AI development company to build, test, and validate AI for lending models (scoring, fraud, pricing).

3. Deployment: Seamlessly integrate the AI lending software into your AI lending platform, core systems, and customer channels using automated MLOps pipelines.

4. Monitoring: Use AI model monitoring for credit to continuously track performance, data drift, and fairness metrics, triggering alerts if models begin to degrade or exhibit bias (AI discoverability bias in lending).

5. Governance: Embed AI governance for lenders to enforce approvals, documentation, and periodic reviews, ensuring responsible AI in lending.

This MLOps framework ensures that AI lending automation remains reliable, compliant, and aligned with the organization’s risk appetite.

Cost of Implementing AI in Lending Software

The cost of implementing AI in lending software depends heavily on scope, complexity, and whether you choose custom AI lending software or configure an off-the-shelf AI lending platform. Lenders must evaluate the total cost of ownership.

Indicative Ranges for AI in lending software projects:

| Project Scope | Estimated Cost (USD) | Focus |

| Basic Integration | $100,000 - $300,000+ | Adding targeted features like a real-time fraud detection agent or initial AI-driven loan approval on an existing system. |

| Modular Platform | $300,000 - $800,000+ | Deploying a comprehensive machine learning lending platform with multiple models (scoring, risk, collections) and integrations. |

| Custom End-to-End Stack | $800,000 - $3,000,000+ | Building a full custom AI lending software solution, including a new AI loan origination system, advanced AI risk assessment software, and deep integration with legacy core systems. |

Ongoing costs include AI development services for maintenance and upgrades, data preparation, change management, and continuous AI governance in BFSI, as well as model monitoring, which, while adding annual expense, typically delivers significant ROI when the solution is well-targeted and drives AI lending automation. Evaluate the AI lending automation strategy based on business case, not just initial cost.

Evaluating the Best AI Software for Lending

To evaluate the AI lending automation landscape and select the best AI software for lending for your institution, consider these critical factors:

- Use Case Coverage: Does the platform cover the full spectrum of AI use cases for lending (originations, servicing, collections, fraud, portfolio management)?

- BFSI Readiness: Does it support the specific workflows and regulatory requirements for AI in NBFC lending, banks, and credit unions in the US and Canada?

- Integration: How easily does it integrate with your core systems, LOS, CRM, and digital channels?

- Compliance Tools: Does it include built-in explainable AI in lending features, AI compliance in lending support, and tools to combat AI discoverability bias in lending?

- MLOps & Governance: What is the strength of its MLOps for lending models and AI model governance in BFSI tools?

Working with an experienced AI banking software development company or AI development company can help you assess build vs. buy strategies and design custom AI lending software that tightly fits your unique underwriting and risk framework.

How Banks and NBFCs Use AI in Lending: Practical Examples

Real-world AI examples in banking illustrate how AI-powered lending delivers tangible business value across sectors.

- Retail Banks: Utilizing AI loan origination systems and AI-powered credit decisioning engines platforms to pre-approve card and personal loans in minutes using machine learning and behavioral data. This is a primary driver for rapid AI loan processing automation.

- Commercial/SME Lenders: Deploying AI in lending software and specialized AI-powered commercial lending software to underwrite small businesses using cash-flow analytics, transaction data, and alternative data for credit underwriting to assess viability faster than manual review.

- NBFCs and Credit Unions: Leveraging AI credit scoring models for NBFCs and alternative data to serve thin-file customers and support AI lending software for financial inclusion initiatives, democratizing access to capital.

- AI Loan Company (Fintechs): Building entire operations around machine learning lending platform technology, offering near-instantaneous, risk-based loan pricing AI, and highly efficient AI-driven loan servicing.

These AI for digital lending examples show how AI is used in lending to expand access, accelerate processes, and drastically improve portfolio performance.

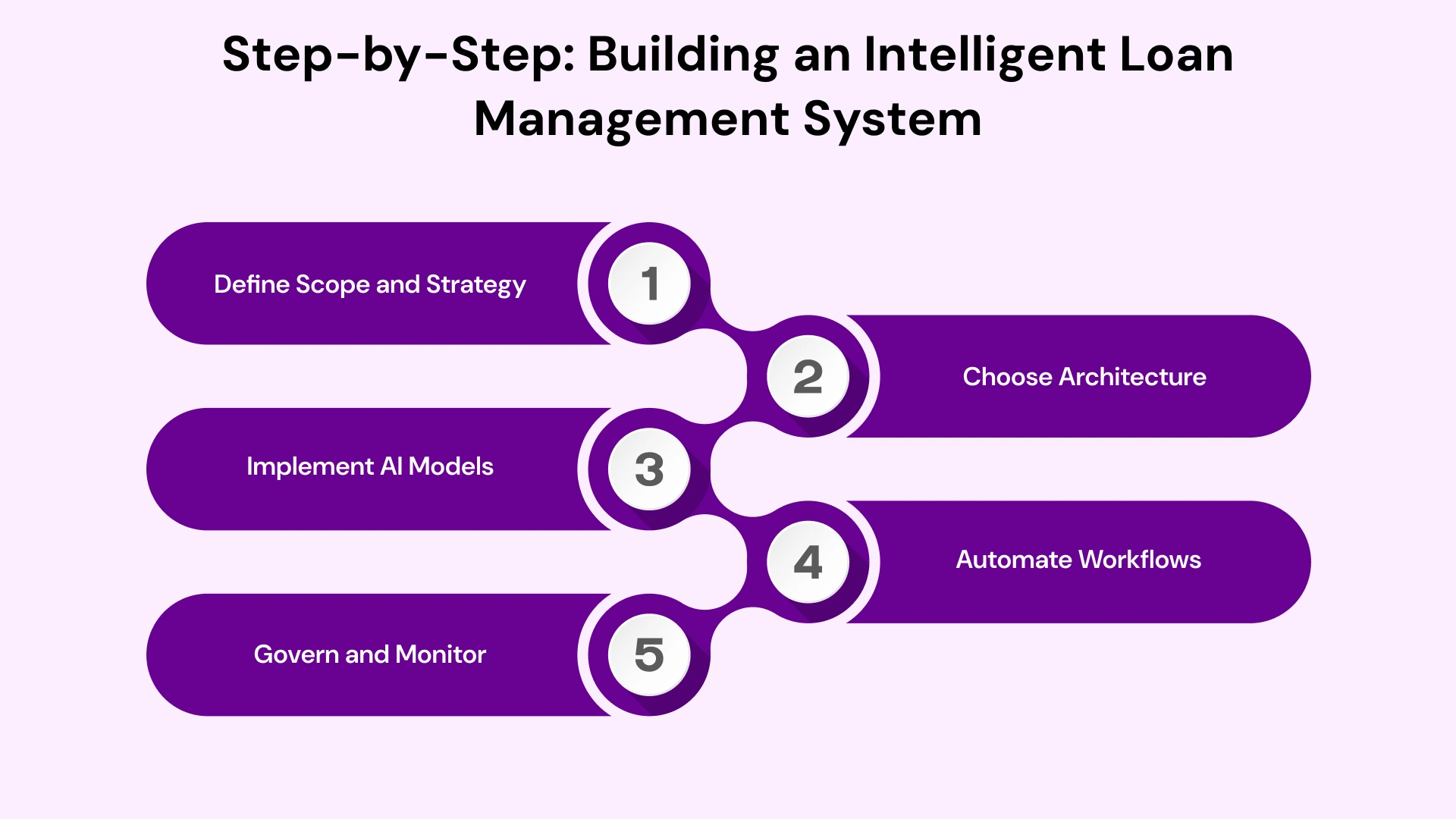

How to Build a Loan Management System with AI

For lenders considering how to build a loan management system or modernize an existing one with AI, the journey requires a structured approach centered on AI lending automation.

1. Define Scope and Strategy: Identify priority use cases for AI in lending, including AI loan processing automation, AI-driven loan servicing, AI fraud detection for lending, etc.

2. Choose Architecture: Decide whether to extend an existing AI lending platform, deploy a new machine learning lending platform, or commission custom AI lending software from an AI development company. Focus on decision engine modernization.

3. Implement AI Models: Implement AI models for scoring, underwriting, risk-based loan pricing, and fraud. Ensure these models support explainable AI in lending.

4. Automate Workflows: Use AI workflow automation for lending to orchestrate end-to-end journeys from application to payoff, leveraging Agentic AI for complex, multi-step tasks.

5. Govern and Monitor: Embed AI governance for lenders, AI compliance in lending, and AI model monitoring for credit to ensure responsible AI in lending over time. This includes making loan products machine-readable to standardize inputs.

This methodical approach ensures that AI in lending becomes a durable competitive advantage, not just a one-off pilot.

Digital Transformation in Lending with AI

AI in lending is the cornerstone of digital transformation in lending. It supports:

- Embedded Lending: Delivering instant credit decisions through AI-powered lending APIs embedded in e-commerce, payroll, and B2B platforms.

- End-to-End Digital Journeys: Enabling fully digital originations and AI-driven loan servicing.

- Decision Engine Modernization: Making loan products machine-readable and ensuring AI-powered credit decisioning engines platforms are scalable.

As more institutions adopt AI lending automation, lenders who delay implementing AI in their lending software risk falling behind in speed, personalization, and cost efficiency. The future of AI in banking is intrinsically linked to the speed and efficiency gains advanced AI enables in lending.

Many lenders are also exploring how does DeFi lending works compared to traditional AI for lending. In Decentralized Finance (DeFi), smart contracts on blockchain networks automate lending pools, collateral management, and liquidations. While DeFi lending and AI loan company models differ from bank-based AI-powered lending, both share goals around automation, transparency, and data-driven risk assessment.

Traditional financial institutions can learn from the speed and automation of DeFi lending. AI in fintech is increasingly connecting these worlds, enabling new hybrid models that blend AI's control in banking with the efficiency of modern AI lending platform technology. This can involve combining traditional credit data with real-time digital and behavioral signals to enhance risk models.

How VLink Expertise Can Help Your Business Transform Lending

In the rapidly evolving landscape of AI-powered lending in 2026, choosing the right technology partner—an expert AI banking software development company—is as critical as the technology itself. VLink provides the end-to-end expertise necessary to navigate the complexities of AI in lending regulation, data science, and secure implementation across the US and Canadian markets.

Our AI development services are specifically designed to help banks, NBFCs, and fintechs move beyond pilot projects to achieve full-scale AI lending automation and superior business results.

1. End-to-End AI Lending Platform Development (Custom AI Lending Software)

We don't just implement models; we build the foundational AI lending platform that scales with your institution. Our dedicated team specializes in custom AI lending software and decision engine modernization, ensuring seamless integration with your existing core banking systems and LOS.

- Focus Areas: Developing proprietary AI loan origination system modules, integrating AI credit scoring software that utilizes alternative data for credit underwriting, and architecting a central machine learning lending platform that supports multiple products.

2. Responsible AI and Compliance Assurance (Fair Lending AI Compliance)

Compliance is non-negotiable. Our experts embed responsible AI in lending principles from the design phase, ensuring your systems meet stringent regulatory requirements for fair lending AI compliance in North America.

- Focus Areas: Implementing robust AI governance for lenders and AI model governance in BFSI; providing explainable AI in lending (XAI) features to generate transparent rationales for every AI-powered loan decision; and actively mitigating AI discoverability bias in lending. We ensure continuous AI compliance in lending through dedicated AI model monitoring for credit solutions.

3. High-Impact Automation & Agentic AI

We drive efficiency by leveraging the latest Agentic AI for lending and generative AI for lending technologies, delivering true AI workflow automation for lending.

- Focus Areas: Deploying advanced automated loan underwriting AI solutions for straight-through processing; building a smart, real-time fraud detection agent to protect against synthetic identity fraud and scams; and implementing sophisticated AI-driven loan servicing and collections strategies that lower operational costs and improve recovery rates.

4. Expert MLOps for Lending Models and Scalability

Our approach is built on MLOps (Machine Learning Operations), ensuring your AI lending models are not just launched but are continuously monitored, updated, and governed to maintain peak performance and risk-based accuracy.

- Focus Areas: Establishing MLOps pipelines for AI loan processing automation; evaluating the AI lending automation performance metrics; and providing post-deployment AI development services to future-proof your investment in AI in fintech.

Partner with VLink to leverage the full spectrum of AI for lending capabilities. We provide the strategic guidance and technical excellence needed to transform your loan portfolio, accelerate decision-making, and secure your leadership position in the future of AI in banking.

Conclusion: The AI Mandate for Lending Success in 2026

AI in lending is no longer a strategic option; it is a competitive necessity. For US and Canadian lenders, the adoption of AI-powered lending will define who leads the market in speed, efficiency, and financial inclusion in 2026 and beyond.

The future of AI in banking demands a cohesive strategy that integrates AI lending software across the entire lifecycle—from AI credit scoring and loan origination systems to AI-driven loan servicing and AI fraud detection. Institutions that embrace decision-engine modernization and commit to AI lending automation will be best positioned to unlock the full potential of risk-based loan-pricing AI.

Crucially, success hinges on responsible AI in lending. Deploying advanced tools like Agentic AI for lending and sophisticated AI underwriting software must go hand in hand with robust AI governance for lenders and AI compliance in lending. This ensures that the pursuit of efficiency supports fair lending AI compliance and builds trust with both regulators and customers.

Ready to unlock the benefits of AI in lending and build an AI-driven loan management system that scales? Reach out today, and let’s discuss how AI for lending and AI-powered lending can transform your portfolio, your customer experience, and your growth trajectory in 2026 and beyond.

Vice President, Strategy – VLink Inc.

Sambhavi Gopalakrishnan is the Vice President of Strategy at VLink Inc., bringing over a decade of experience in IT leadership, project implementation, and strategic growth. She possesses a strong foundation in technical project management and pre-sales, driving innovation and business transformation at VLink.

Shivisha Patel

Shivisha Patel