For CIOs and VP-level engineering leaders in Canada's banking sector, this isn't just another technology trend report—it's a wake-up call. Most agentic AI projects right now are early-stage experiments or proofs of concept, driven mainly by hype and often misapplied, warns Gartner Senior Director Analyst. The real culprit isn't AI's immaturity or lack of use cases; it's the decades-old technological foundation upon which banks attempt to build these sophisticated systems.

At least 55% of banks say the limitations of their existing core solutions are the biggest roadblock to achieving their business goals, according to research from 10x Banking. Meanwhile, 75% of banks, insurers, and financial firms rank legacy system compatibility as critical for successful AI integration, far more than in other industries. These numbers paint a clear picture: legacy system blockages in BFSI aren't just a technical inconvenience—they're the primary barrier preventing financial institutions from realizing the transformative potential of AI.

In this comprehensive guide, we'll explore why legacy systems that block AI adoption represent one of the most critical challenges facing Canadian BFSI organizations today, examine the specific technical and operational barriers that create this blockage, and outline proven strategies to overcome these constraints and unlock genuine AI transformation.

Understanding the Legacy System Challenge in Canadian BFSI

Canadian banks and financial institutions have built their operations on infrastructure that was cutting-edge decades ago but now serves as a millstone around innovation efforts. Legacy platforms consume up to 70 percent of IT budgets, leaving little room for digital transformation initiatives. This financial drain creates a vicious cycle: the more resources consumed by maintaining antiquated systems, the less capital remains available for modernization efforts.

Legacy systems modernization and observability consume 75% of IT budgets for maintenance while limiting innovation and creating security vulnerabilities that expose banks to an average breach cost of $4.45M. For Canadian BFSI leaders, this represents not just an operational challenge but a strategic vulnerability that competitors—both traditional and fintech disruptors—are eager to exploit.

The infrastructure problem extends beyond mere maintenance costs. 53% of institutions utilizing legacy core systems are struggling to scale their operations due to data silos and production bottlenecks. These silos prevent the seamless data flow that AI systems require, creating fundamental incompatibilities between what modern agentic AI needs and what legacy architectures can deliver.

Why Traditional Banking Infrastructure Fails Modern AI

Legacy banking systems were architected for a different era—one prioritizing stability, batch processing, and branch-centric operations. Over 55% of institutions find that legacy systems slow progress, creating subtle roadblocks that frustrate teams and complicate decision-making. The architectural assumptions embedded in these systems create multiple failure points when integrating AI.

Organizations modernizing legacy environments often evaluate migrating legacy core banking systems to reduce disruption while improving scalability and long-term maintainability.

Legacy platforms weren't architected for today's interconnected digital landscape, and their rigid design philosophy creates substantial barriers to institutions' adoption of contemporary capabilities. Agentic AI systems require real-time data access, distributed processing, and flexible integration points—characteristics that are fundamentally at odds with monolithic legacy architectures.

Only 32% of banks have successfully integrated artificial intelligence into their core systems, leaving them at a significant disadvantage compared to more agile competitors. This integration gap doesn't merely slow innovation; it threatens the competitive viability of institutions unable to deliver the personalized, intelligent services that customers increasingly expect.

The Agentic AI Promise and Reality Gap

Agentic AI represents a fundamental evolution beyond conventional AI assistants and automation tools. Agentic AI refers to artificial intelligence systems that have the agency—within defined guardrails—to go beyond merely augmenting workflows to fully automating them. These systems can interpret user intent, access relevant data across multiple applications, and produce meaningful outcomes with minimal human intervention.

For BFSI organizations, the potential applications span the entire operational spectrum. From autonomous fraud detection and risk assessment to intelligent loan underwriting and personalized wealth management, agentic AI promises to transform not just individual tasks but entire business processes. AI is revolutionizing BFSI by optimizing credit decisioning, fraud detection, compliance management, and customer interactions.

The business value proposition is compelling. Gartner predicts that at least 15% of day-to-day work decisions will be made autonomously through agentic AI by 2028, up from 0% in 2024. Additionally, 33% of enterprise software applications will include agentic AI by 2028, up from less than 1% in 2024. This exponential growth trajectory represents both opportunity and urgency for Canadian financial institutions.

The Integration Complexity Challenge

The excitement surrounding agentic AI often obscures the practical realities of implementation. Integrating agents into legacy systems can be technically complex, frequently disrupting workflows and requiring costly modifications. This technical complexity manifests across multiple dimensions simultaneously.

Many financial compliance systems were designed decades ago with rigid architectures, and unlike newer, modular financial platforms, these legacy systems lack interoperability and require extensive customization to enable AI adoption. The gap between AI's requirements and legacy capabilities creates substantial engineering challenges that most organizations underestimate.

Gartner estimates only about 130 of the thousands of agentic AI vendors are real, with many engaging in "agent washing"—rebranding existing products without substantial agentic capabilities. This market confusion compounds the technical challenges, making it difficult for BFSI leaders to distinguish genuine solutions from repackaged conventional tools.

The Business Value Measurement Problem

Beyond technical integration challenges, organizations struggle with demonstrating a clear return on investment. Most agentic AI propositions lack significant value or return on investment, as current models don't have the maturity and agency to autonomously achieve complex business goals or follow nuanced instructions over time.

Today's ROI models fixate on short-term metrics like headcount reduction or immediate cost savings, overlooking the fundamental value drivers such as improved decision quality, enhanced customer experience, and accelerated time-to-market for new products. This measurement mismatch leads executives to cancel projects that might deliver substantial long-term value but fail to demonstrate immediate returns.

The challenge intensifies in regulated industries like BFSI. 51% of financial institutions cite regulatory risks as a top challenge, compared to 29% of technology companies, underscoring the need for compliance to be tightly woven into every integration decision. This regulatory complexity adds layers of validation requirements, extending implementation timelines and increasing costs.

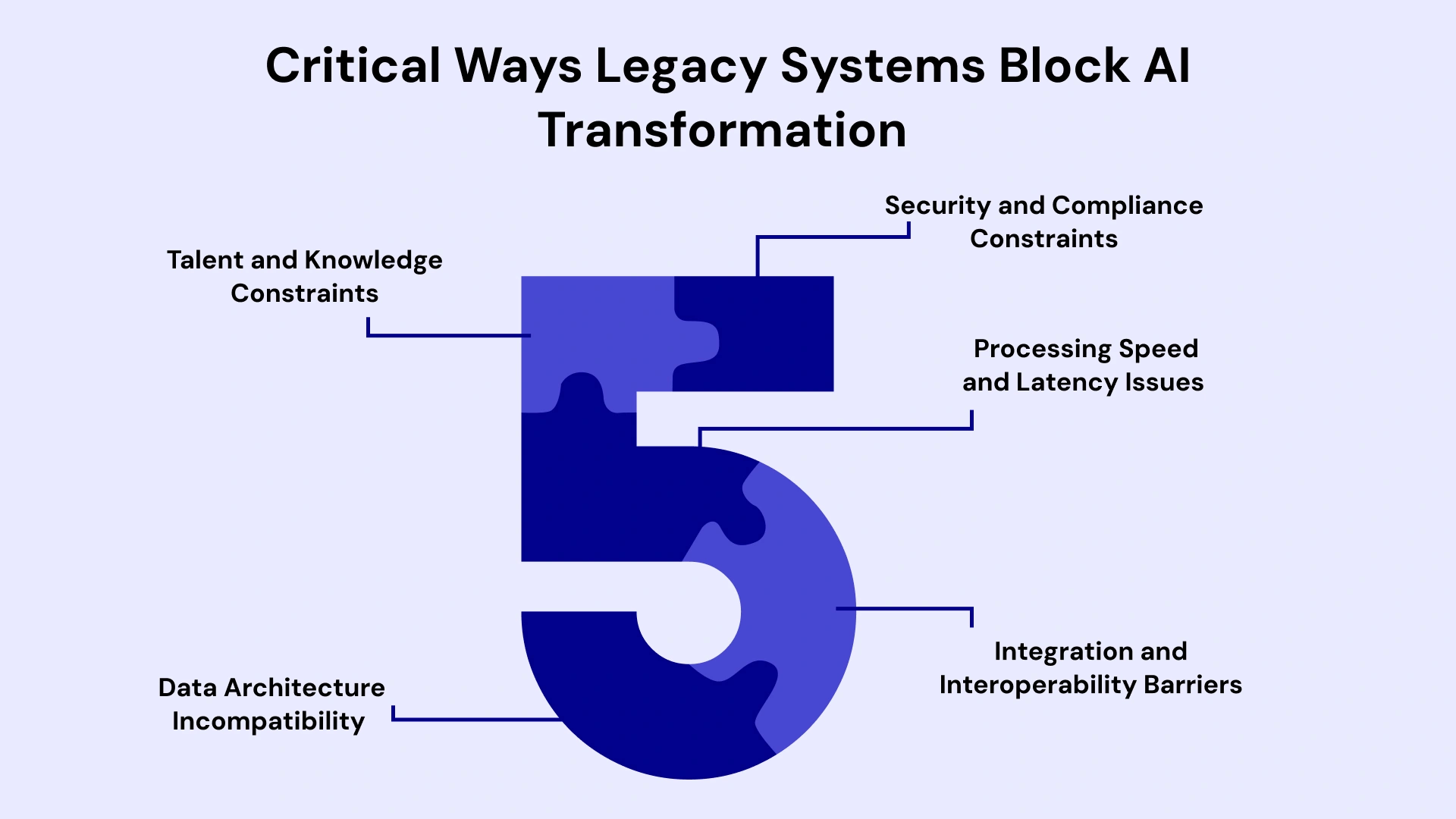

5 Critical Ways Legacy Systems Block AI Transformation

While legacy systems are often the backbone of a company’s operations, they serve as a "technical anchor" when launching AI initiatives. Transitioning from traditional software to AI-driven processes isn't just about adding new tools; it requires a structural overhaul that legacy environments often can't support.

Here are the five critical ways legacy systems block AI transformation:-

1. Data Architecture Incompatibility

Modern agentic AI systems thrive on unified, real-time access to data across organizational silos. Legacy systems, conversely, were designed around departmental boundaries and batch processing paradigms. Legacy systems often lead to stranded or uncollected data, hindering banks from effectively competing with other digital players, implementing advanced analytics-based solutions, or experimenting with predictive analytics, AI, and ML.

This architectural mismatch creates several specific problems. First, data remains trapped in proprietary formats that AI systems cannot efficiently access or interpret. Second, the lack of real-time synchronization means AI models operate on stale information, reducing their effectiveness and reliability. Third, inconsistent data quality across disparate systems undermines AI model accuracy, leading to unreliable outputs that erode user trust.

Incumbent banks cannot perform real-time business intelligence and advanced big data analysis with their outdated system unless they establish a robust data management platform. This fundamental constraint limits even well-designed AI initiatives to operating at speeds and scales far below their potential.

2. Integration and Interoperability Barriers

Legacy banking cores function as closed ecosystems, restricting third-party integrations to approved vendor partnerships. Legacy cores often function as gatekeepers, restricting third-party services to preferred vendor ecosystems, and retrofitting modern tools requires substantial investments in data transformation, API development, and infrastructure upgrades.

The technical challenge extends beyond simple connectivity. Monolithic architectures lack the modular design principles that enable flexible integration. Making changes to one component risks cascading failures across the entire system, forcing conservative change management practices that slow AI deployment to a crawl.

Retrofitting AI into existing financial crime prevention workflows can involve significant investments in data transformation, API development, model training, rewriting code, and system security enhancements. These costs often exceed initial estimates by orders of magnitude, leading to project cancellations before full implementation.

3. Processing Speed and Latency Issues

Agentic AI systems require near-instantaneous data access and processing capabilities to deliver responsive, intelligent interactions. Legacy systems operate on fundamentally different time scales. Legacy cores operate on batch processing models and overnight jobs rather than the continuous data streams modern digital experiences require.

This temporal mismatch creates critical limitations for AI applications. Customer-facing AI agents cannot deliver personalized recommendations when the product catalog is updated nightly. Fraud detection systems lose effectiveness when transaction analysis occurs hours after the fact. Risk assessment models produce outdated conclusions when market data is refreshed on batch schedules.

The latency problem compounds when AI systems must query multiple legacy components to assemble the information needed for decision-making. Each system call introduces additional delay, degrading the user experience below acceptable thresholds and negating the efficiency gains that motivated the AI investment.

4. Security and Compliance Constraints

Modern AI systems require broad data access to function effectively, creating security challenges when integrated with legacy systems designed around compartmentalized data access. Many traditional banks grapple with legacy systems that hinder the seamless integration of cutting-edge AI defenses, creating new vulnerabilities.

The compliance dimension adds further complexity. Regulations such as Basel III, PSD2, and GDPR require real-time reporting and monitoring, which legacy systems struggle to support. AI systems that cannot provide transparent audit trails or explain their decision-making processes face regulatory rejection, regardless of their technical sophistication.

Canadian financial institutions face particularly stringent privacy requirements, which make the limitations of legacy systems even more acute. AI systems must demonstrate data residency compliance, consent management, and right-to-explanation capabilities—all of which are difficult to implement when the underlying systems lack the necessary architectural foundations.

5. Talent and Knowledge Constraints

COBOL and other legacy skills are increasingly scarce, increasing the risk of outages and costly errors. This talent shortage creates a double bind: organizations need experts who understand both legacy systems and modern AI technologies, but such individuals are hard to find.

You need engineers who understand legacy systems and specialists who can build modern architectures, and the few people who can bridge both worlds spend their time firefighting instead of advancing transformation. This resource constraint prevents organizations from maintaining existing systems while simultaneously building new AI capabilities.

The challenge of knowledge transfer intensifies as experienced engineers retire. Undocumented system behaviors, unofficial workarounds, and tribal knowledge disappear, increasing the risk of critical failures during AI integration attempts. Organizations find themselves trapped between preserving institutional knowledge and building new capabilities.

Why Canadian BFSI Faces Unique Challenges

While Canadian BFSI institutions share many global legacy headaches, they face a specific set of hurdles—often referred to as the "Stability Paradox." Canada has one of the world's most stable financial systems, but that very stability has created a unique environment that complicates AI transformation.

Regulatory Complexity and Consumer Protection Standards

Canadian financial institutions operate under some of the world's most rigorous regulatory frameworks. The Office of the Superintendent of Financial Institutions (OSFI) maintains stringent capital adequacy requirements, stress testing protocols, and operational resilience standards that influence technology decisions at every level.

These regulatory requirements create specific constraints for AI deployment. Model validation processes extend implementation timelines significantly beyond those in less regulated markets. Explainability requirements force organizations to sacrifice some AI model performance in favor of interpretability, reducing the competitive advantage these systems provide.

Consumer protection standards add further complexity. Canadian privacy regulations require explicit consent for data usage, limiting the information available to train AI models. Cross-border data restrictions prevent Canadian institutions from leveraging global datasets or cloud services without substantial compliance frameworks, increasing costs and complexity.

Market Concentration and Competitive Dynamics

Canada's banking sector is highly concentrated, with five major banks dominating the market. This oligopolistic structure creates both challenges and opportunities for AI transformation. On one hand, market leaders can afford substantial technology investments that smaller competitors cannot match. On the other hand, the competitive intensity among major players creates a sense of urgency for innovation.

The threat of fintech disruption looms larger in Canada than many executives acknowledge. Digital-native competitors unencumbered by legacy infrastructure can launch new products and services at speeds traditional banks cannot match. Wealth management platforms, payment processors, and lending marketplaces steadily erode market share in high-margin segments while incumbents struggle with system modernization.

Bilingual Requirements and Regional Variations

Canadian institutions face unique operational requirements around bilingual service delivery and provincial regulatory variations. AI systems must function effectively in both English and French, with language models that understand financial terminology, cultural nuances, and regulatory differences across languages.

These requirements complicate AI deployment beyond the challenges faced by institutions in monolingual markets. Training data must adequately represent both linguistic communities. User interfaces must support seamless language switching. Compliance frameworks must address language-specific regulations in Quebec and other provinces.

Strategic Approaches to Breaking the Legacy Blockage

Here are the five strategic approaches to breaking the legacy blockage:

Adopt a Phased Modernization Strategy

In many cases, rethinking workflows with agentic AI from the ground up is the ideal path to successful implementation. Rather than attempting wholesale system replacement, successful organizations adopt incremental approaches that reduce risk while building momentum.

The phased strategy begins with a comprehensive system assessment. Organizations must understand current dependencies, identify critical components, and map data flows before designing modernization plans. This discovery phase often reveals unexpected interdependencies that would derail poorly planned transformation efforts.

Next, prioritize modernization based on business value and technical feasibility. Start with systems that touch customer experience directly and have clear ROI metrics. Build confidence through visible wins before tackling more complex core systems. This approach maintains stakeholder support throughout the extended transformation journey.

Bring in specialized teams for the complex parts instead of waiting to hire unicorns. Partner with experts who have successfully navigated similar transformations rather than attempting to build all capabilities internally. This approach accelerates progress while developing internal expertise over time.

Implement AI Overlay Architecture

AI overlays serve as middlemen between legacy systems and advanced AI-powered compliance solutions, which can be particularly appealing given the long-term nature of corporate software agreements. This architectural pattern enables organizations to deploy AI capabilities without requiring fundamental changes to underlying systems.

AI overlays function by creating an abstraction layer that mediates between legacy data sources and modern AI engines. The overlay handles data transformation, enrichment, and synchronization, presenting a clean, standardized interface to AI systems while managing the complexity of legacy integration behind the scenes.

This approach delivers several key advantages. First, it preserves existing investments in core systems while enabling AI innovation. Second, it reduces risk by isolating AI experimentation from production systems. Third, it allows gradual capability enhancement without disruptive system replacements.

AI overlays enable financial institutions to deploy the latest technology in name screening, transaction screening, and transaction monitoring without disrupting core banking functions. Organizations can realize AI benefits in months rather than years, generating business value that funds continued modernization efforts.

Establish Cloud-Native Development Practices

Shifting from monolithic systems to modular, cloud-native architectures provides agility, scalability, resilience, and integration capabilities essential for successful AI deployment. Cloud-native approaches fundamentally change how organizations build, deploy, and operate software systems.

Microservices architecture enables independent development and deployment of system components. Teams can iterate rapidly on AI capabilities without coordinating complex release schedules across monolithic systems. This development velocity allows organizations to test hypotheses, gather feedback, and refine approaches much faster than traditional methods permit.

API-first design principles ensure that systems expose well-defined interfaces that AI agents can programmatically access. Rather than screen-scraping or database integration hacks, AI systems interact through stable, versioned APIs that provide clean data access with proper authentication and authorization.

Container orchestration platforms like Kubernetes enable consistent deployment across development, testing, and production environments. AI models can run in isolated containers with guaranteed resource allocation, preventing the "works on my machine" problems that plague traditional deployment processes.

Focus on Data Platform Modernization

Shifting to a unified data platform will significantly enhance data traceability, accountability, and reporting capabilities, helping banking institutions remain compliant with the latest industry regulations. Data platform modernization often delivers more immediate value than attempting to replace core transaction systems.

Modern data platforms consolidate information from disparate sources into unified storage with consistent access patterns. Data lakes and warehouses built on cloud infrastructure provide the scalability and performance characteristics that AI systems require while maintaining cost efficiency.

Real-time data streaming architectures enable AI systems to operate on current information rather than stale batch extracts. Technologies such as Apache Kafka and cloud-native streaming services would allow events to flow from legacy systems to AI engines with minimal latency, dramatically improving decision quality.

Data governance frameworks ensure that AI systems access information appropriately while maintaining audit trails for compliance purposes. Metadata management, lineage tracking, and access control policies protect sensitive information while enabling legitimate AI use cases.

Develop Robust AI Governance Frameworks

In this early stage, Gartner recommends pursuing agentic AI only where it delivers clear value or ROI. Disciplined governance prevents organizations from falling into the hype-driven project proliferation that leads to the predicted 40% cancellation rate.

AI governance begins with clear evaluation criteria for use cases. Organizations should assess projects based on business impact, technical feasibility, regulatory compliance, and alignment with strategic objectives. This framework prevents waste of resources on low-value experiments while ensuring high-priority initiatives receive adequate support.

Model risk management becomes critical as AI systems influence consequential decisions. Organizations need frameworks for model validation, performance monitoring, and bias detection. These capabilities ensure AI systems remain accurate, fair, and compliant throughout their operational lifecycle.

Change management processes must adapt to AI's unique characteristics. Unlike traditional software that behaves deterministically, AI systems evolve through learning and may produce unexpected outputs. Governance frameworks must balance the need for innovation velocity with appropriate controls and oversight.

Real-World Implementation Lessons from BFSI Leaders

Implementing large-scale digital transformation in the BFSI sector is often described as "changing the engines of a plane while it’s in flight." In 2025 and 2026, leaders have moved past the initial hype of digitalization to focus on the grit of execution.

Below are the key real-world lessons and strategic pillars identified by industry leaders from recent implementations.

Start with Non-Critical, High-Visibility Use Cases

Successful organizations begin their agentic AI journeys with applications that demonstrate value without risking critical operations. Customer service chatbots, document processing automation, and marketing personalization represent ideal starting points. These use cases deliver tangible benefits while allowing teams to build expertise with manageable risk.

Test new AI capabilities alongside existing processes, enabling continuous service while generating evidence that AI-enhanced systems meet regulatory standards. Parallel operation reduces implementation risk while building stakeholder confidence in AI capabilities.

Quick wins generate organizational momentum and secure executive support for more ambitious initiatives. Each successful deployment builds credibility and demonstrates that AI transformation is achievable despite legacy constraints. This momentum proves essential for sustaining multi-year modernization programs.

Invest in Data Quality Before AI Development

Many organizations rush into AI development before ensuring data quality meets minimum requirements. This approach inevitably leads to disappointment when models trained on poor data produce unreliable results. A significant chunk of AI is fundamentally data science, especially ML, predictive analytics, forecasting, and business analytics, making data the maximum lever for financial software development services.

Data quality initiatives should focus on completeness, accuracy, consistency, and timeliness. Automated data validation pipelines catch quality issues before they contaminate AI training processes. Data cleansing efforts correct historical inconsistencies that would otherwise limit model effectiveness.

Master data management establishes a single source of truth for critical business entities, such as customers, products, and accounts. AI systems operating on consistent, authoritative data sources deliver more reliable results than those that attempt to reconcile conflicting information across siloed systems.

Build Cross-Functional AI Centers of Excellence

60% of BFSI firms struggle with AI talent shortages, underscoring the criticality of upskilling initiatives and AI literacy programs for transformation success. Organizations should establish centers of excellence that combine technical expertise, domain knowledge, and change management capabilities.

These centers serve multiple functions: developing reusable AI components, establishing best practices, training staff, and advising business units on implementation approaches. Centralizing expertise prevents duplicated effort and ensures consistent quality across AI initiatives.

Cross-functional teams bring together data scientists, software engineers, risk managers, compliance officers, and business stakeholders. This diversity ensures AI solutions address real business problems while meeting regulatory requirements and technical constraints. Siloed efforts typically fail to achieve this balance.

Measure Beyond Traditional IT Metrics

Organizations must focus on enterprise productivity rather than just individual task augmentation when evaluating AI success. Traditional IT metrics like system uptime or transaction throughput inadequately capture AI's business impact.

Successful organizations develop custom measurement frameworks to track business outcomes, including improvements in customer satisfaction, reductions in process cycle time, decreases in error rates, and revenue enhancements. These metrics demonstrate value in business terms that executives understand and appreciate.

Longitudinal tracking proves essential for AI initiatives in insurance software development services that deliver compounding benefits over time. Initial deployments may show modest returns, but as systems learn and users adapt, value accelerates. Measurement frameworks should capture this trajectory rather than making premature judgments based on early results.

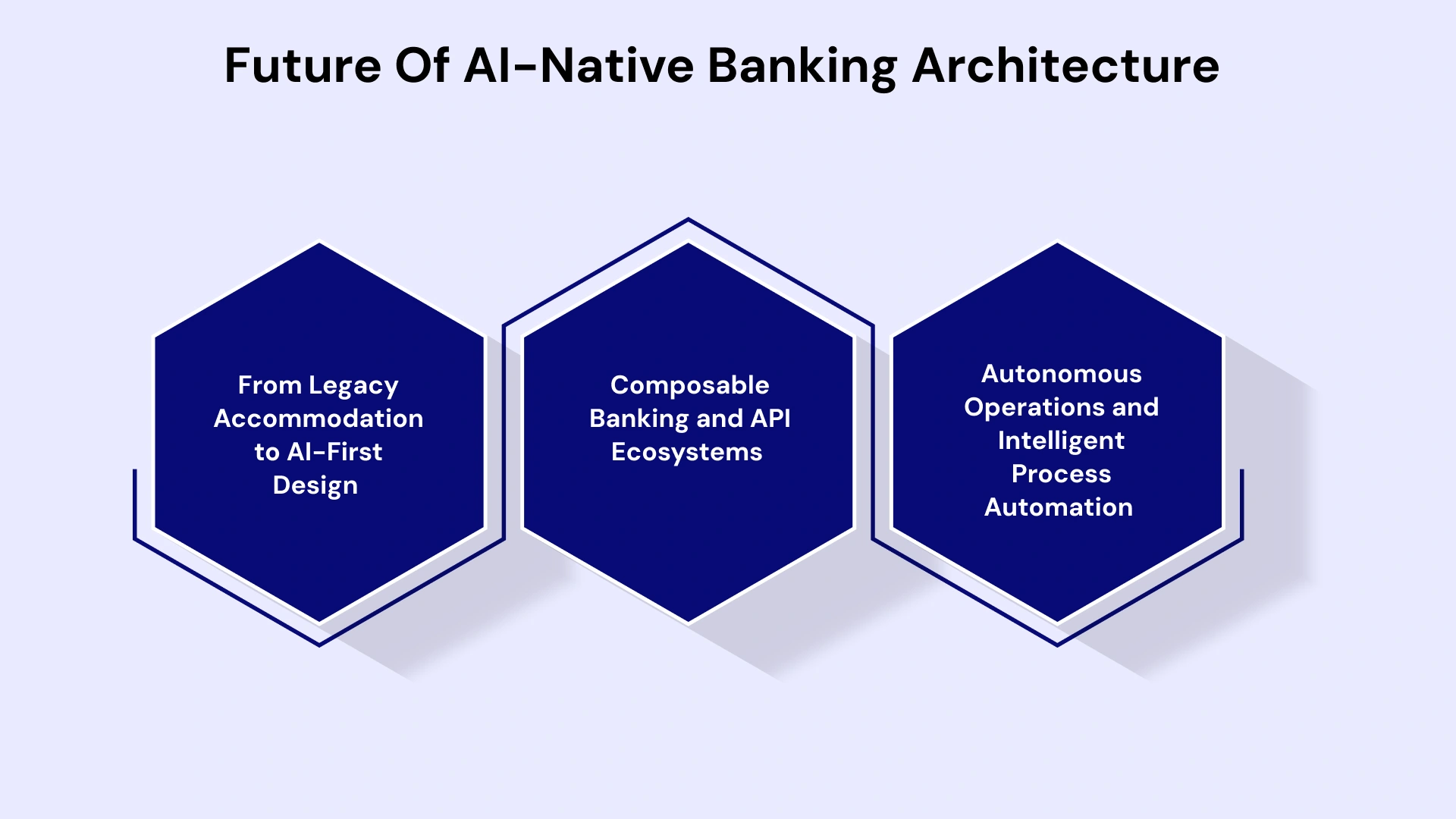

The Future of AI-Native Banking Architecture

In 2026, the industry has shifted from "digital-first" (adding a mobile app to a legacy core) to AI-Native Architecture. This means AI is not a peripheral feature but the bank's fundamental "nervous system," dictating how its core functions operate in real time.

From Legacy Accommodation to AI-First Design

The next generation of banking systems will invert the current paradigm. Rather than retrofitting AI into legacy architectures, institutions will design systems with AI capabilities as foundational components. This shift represents a fundamental rethinking of banking technology architecture.

AI-native systems embed intelligence throughout the stack rather than treating it as an afterthought. Real-time decision engines evaluate transactions, APIs leverage machine learning for fraud detection, and user interfaces adapt dynamically based on behavioral analysis. This pervasive intelligence becomes invisible infrastructure rather than special-purpose applications.

Event-driven architectures enable systems to react immediately to changing conditions. AI models monitor event streams, identify patterns, and trigger automated responses without human intervention. This reactive capability transforms how banks detect risks, serve customers, and optimize operations.

Composable Banking and API Ecosystems

The future of banking technology lies in composable architectures where capabilities assemble dynamically from reusable components. Banks become platforms that orchestrate services from internal systems and external providers, with AI agents coordinating these interactions.

API marketplaces enable rapid capability acquisition without lengthy procurement and integration cycles. Need enhanced identity verification? Call an API. Want improved credit risk models? Access them as services. This composability dramatically accelerates innovation velocity.

Open banking regulations already push institutions toward API-first thinking. Forward-looking organizations recognize that APIs represent more than compliance requirements—they're the foundation for ecosystem participation and partnership-based business models that define future competitive advantage.

Autonomous Operations and Intelligent Process Automation

To get real value from agentic AI, organizations must focus on enterprise productivity rather than just individual task augmentation. The ultimate vision involves end-to-end process automation where AI agents handle entire workflows with minimal human involvement.

Consider mortgage origination: AI agents gather applications, verify information, assess risk, generate offers, and manage documentation—orchestrating dozens of steps that currently require multiple departments and weeks of effort. This level of automation represents a genuine transformation rather than an incremental improvement.

The key differentiator involves intelligent exception handling. Rather than failing when encountering unexpected situations, AI agents escalate to human experts with complete context, learn from their decisions, and expand their autonomous capabilities over time. This learning loop continuously improves operational efficiency.

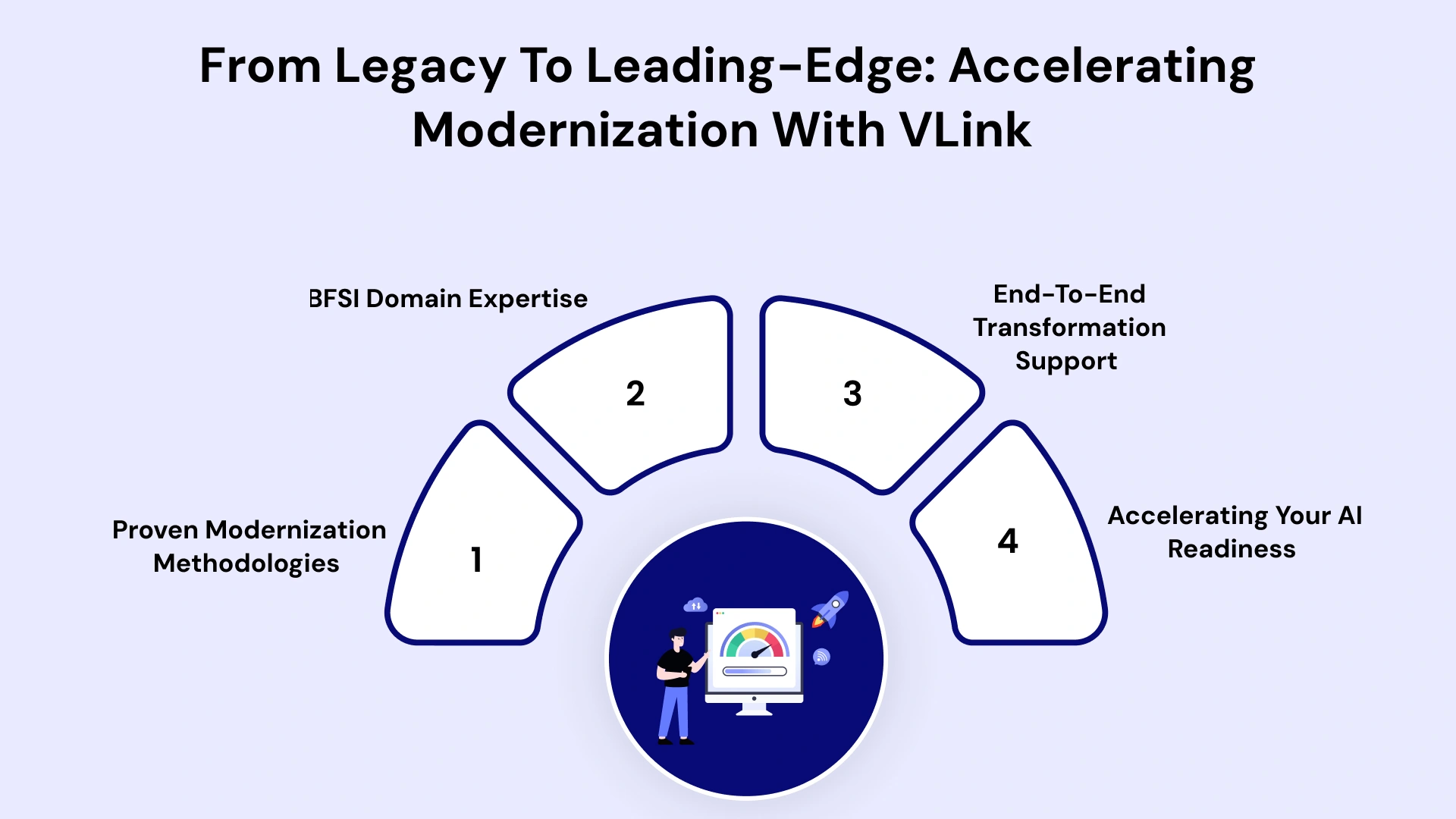

Leveraging VLink's Expertise for Legacy Application Modernization

As Canadian BFSI organizations navigate the complex journey from legacy constraints to AI-enabled futures, the right partnership becomes critical for success. VLink brings deep expertise in legacy application modernization services, specifically designed for the financial services sector, combining technical excellence with industry knowledge to accelerate transformation while managing risk.

Proven Modernization Methodologies

VLink's approach to legacy modernization balances pragmatism with ambition. Rather than proposing risky "big bang" replacements, we implement phased strategies that deliver continuous business value throughout the transformation journey. Our methodology encompasses comprehensive system assessment, strategic roadmap development, incremental implementation, and constant optimization.

We begin every engagement with profound discovery that maps your current state architecture, identifies critical dependencies, assesses data quality and governance, and evaluates team capabilities. This foundation ensures modernization plans reflect reality rather than assumptions, dramatically reducing implementation risks that derail less disciplined efforts.

Our modernization patterns span the full spectrum of approaches: replatforming to cloud infrastructure, API enablement for legacy systems, microservices decomposition, data platform modernization, and AI overlay implementation. We select strategies appropriate to your specific context rather than forcing one-size-fits-all solutions.

BFSI Domain Expertise

Financial services modernization demands more than technical proficiency—it requires a deep understanding of regulatory requirements, risk management frameworks, operational processes, and competitive dynamics. VLink's BFSI practice brings decades of combined experience serving banks, insurers, and asset managers across Canada and globally.

We understand that Canadian institutions face unique challenges: bilingual service requirements, provincial regulatory variations, OSFI guidelines, and specific privacy legislation. Our solutions address these requirements natively rather than as afterthoughts, ensuring compliance from day one.

Our domain expertise spans functional areas critical to AI transformation: customer data platforms for 360-degree views, transaction processing modernization, risk analytics enhancements, regulatory reporting automation, and fraud detection systems. We've solved similar challenges repeatedly, allowing us to accelerate your journey with proven approaches.

End-to-End Transformation Support

VLink provides comprehensive support throughout your modernization journey. Our services span strategy and assessment, architecture and design, implementation and integration, testing and quality assurance, deployment and migration, and ongoing optimization and support.

Our dedicated team recognizes that transformation success depends on more than technology. Change management capabilities ensure your teams embrace new approaches. Training programs build internal expertise that sustains progress beyond initial implementation. Knowledge transfer prevents dependence on external partners while enabling your staff to own and evolve modernized systems.

Our flexible engagement models adapt to your preferences and constraints. Whether you need full project delivery, staff augmentation for specific skills, or advisory services to guide internal teams, VLink structures engagements that fit your context and maximize value.

Accelerating Your AI Readiness

VLink's modernization approach specifically targets AI enablement. We don't just replace legacy systems—we build foundations that support current and future AI initiatives. Our solutions incorporate unified data platforms for AI model training, real-time event processing for intelligent decision-making, API-first architectures for AI agent integration, cloud-native infrastructure for scalability, and robust governance frameworks for risk management.

We've helped numerous BFSI organizations successfully integrate AI capabilities despite legacy constraints. Our experience spans customer service automation, fraud detection enhancement, credit risk assessment, regulatory compliance automation, and personalized wealth management. These proven implementations demonstrate that AI transformation is achievable with the right approach and partnership.

Conclusion: The Imperative for Action

The gap between ambitious Agentic AI goals and stubborn legacy realities is the defining challenge for Canadian BFSI leaders. With 40% of AI projects predicted to fail by 2027, success won't go to those with the best algorithms, but to those who systematically dismantle legacy constraints to build a modern, flexible architecture.

In an era where digital-first competitors launch products in weeks while traditional banks take months, modernization is no longer a "tech initiative"—it is an existential necessity. Your legacy systems are currently a liability, but the institutional knowledge they hold is your greatest asset. By bridging this gap with disciplined execution and patient capital, you can move from maintaining the past to leading the AI-native future.

Hence, don't let technical debt stall your AI ambitions. Whether you are looking to "hollow out the core" or orchestrate a full cloud-native migration, VLink’s experts are ready to help you navigate the complexities of the Canadian BFSI landscape. Contact our team today to schedule a strategic roadmap session and turn your legacy constraints into your competitive advantage.

Vice President, Strategy – VLink Inc.

Sambhavi Gopalakrishnan is the Vice President of Strategy at VLink Inc., bringing over a decade of experience in IT leadership, project implementation, and strategic growth. She possesses a strong foundation in technical project management and pre-sales, driving innovation and business transformation at VLink.

Shivisha Patel

Shivisha Patel