Most banking technology decisions come down to speed, control, and cost. But when it comes to core legacy modernization, the stakes are in a different league entirely.

Here are the numbers that should matter to every banking CTO in North America right now:

This is not a technical argument. It is a strategic one. The choice between Custom software and COTS (Commercial Off-The-Shelf) platforms will define your bank's innovation velocity, regulatory agility, and competitive position for the next decade.

This framework is built for banking CTOs and VP Technology leaders who are preparing for a modernization decision. Not a general IT audience. You.

Why Legacy Modernization in Banking Is Different

Every industry faces technology debt. But banks carry a burden unlike any other sector. The combination of regulatory oversight, 24/7 operational requirements, interconnected payment infrastructure, and decades of patched Legacy System Modernization creates a uniquely complex modernization environment.

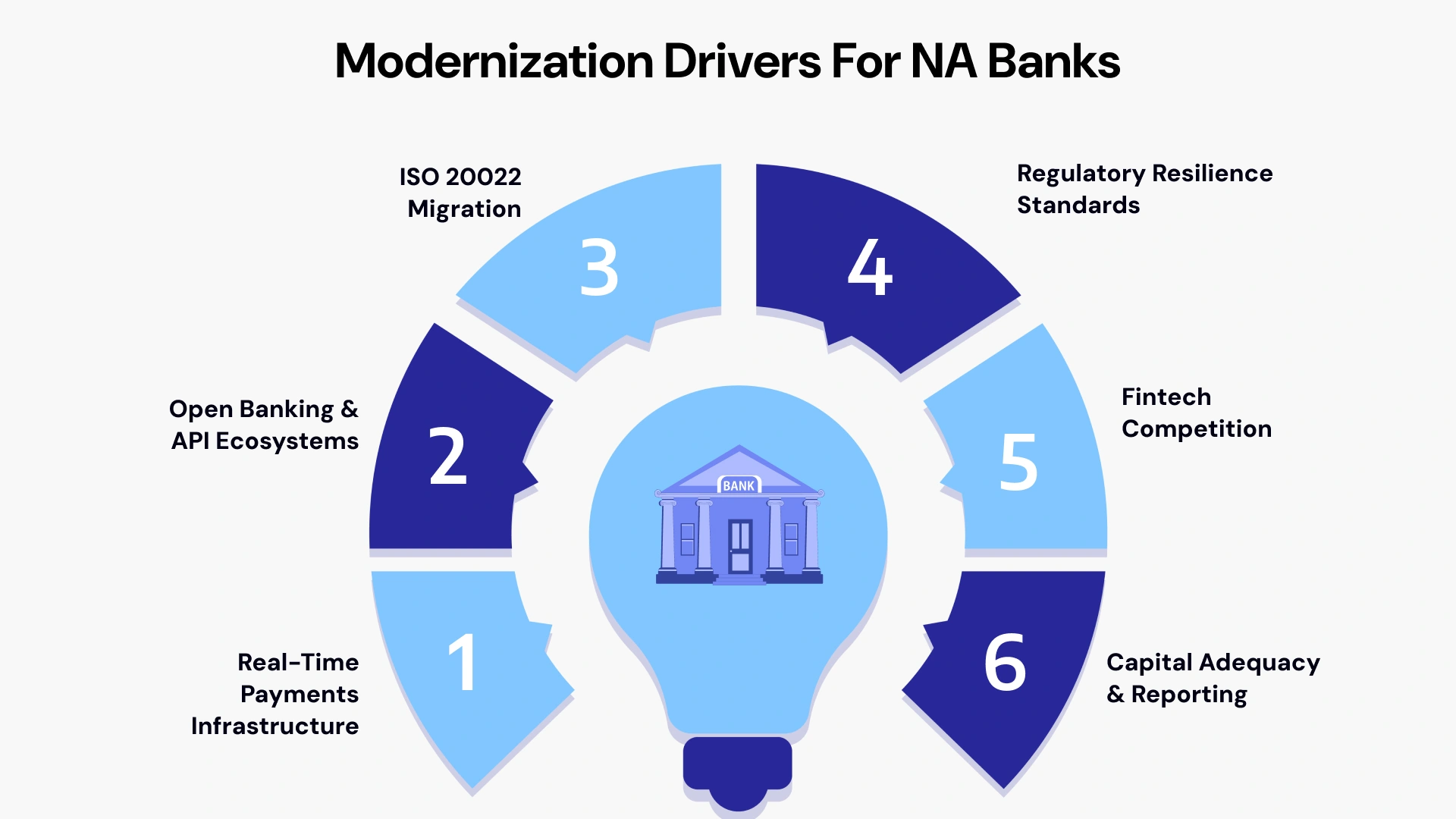

The key drivers pushing North American banks toward modernization right now include:

- Real-time payments infrastructure (FedNow, RTP) demands always-on, low-latency systems

- Open banking and API-first ecosystems requiring modular, interoperable architecture

- ISO 20022 migration timelines with hard regulatory deadlines

- FFIEC and OCC regulatory pressure on cyber resilience and operational continuity

- Customer expectations are shaped by fintech challengers offering instant, frictionless experiences

- Basel III/IV capital adequacy rules require real-time data availability across systems

The decision between custom software development and a COTS banking modernization platform is not made in isolation. It is made against this backdrop. A wrong choice does not just slow innovation. It can create regulatory exposure, talent retention issues, and architecture debt that compounds for years.

This is why banking modernization decisions require a different framework than standard IT procurement.

COTS vs Custom in Banking: Clear Definitions

In the banking sector, the "Build vs. Buy" debate centers on whether to adopt COTS software or develop Custom-Built solutions. This choice defines a bank’s agility, cost structure, and competitive edge.

What Is COTS Software in Banking?

COTS in banking refers to commercial, vendor-built platforms purchased and configured for use within a bank's technology stack. Examples include cloud-native core banking platforms (Thought Machine, Mambu, Temenos), payments processing platforms, loan origination systems (LOS), and regulatory reporting engines.

Key advantages of COTS in banking:

- Faster time-to-deployment (typically 22-52 weeks vs 18-36 months for custom)

- Pre-built compliance features and vendor-managed regulatory updates

- Lower upfront development cost

- Established vendor support and SLA guarantees

What Is Custom Software Development in Banking?

Custom banking software is built specifically for a bank's unique workflows, products, and customer experience requirements. Common areas for custom development include digital banking channels, customer onboarding platforms, AI-driven lending decisioning, fraud analytics, and proprietary wealth management tools.

Key advantages of custom development:

- Full architectural control and competitive differentiation

- Flexibility to integrate with any fintech partner or payment rail

- No vendor roadmap dependency or licensing fee escalation

- Tailored data models for advanced AI and analytics use cases

The Third Option: Composable Banking Architecture

Here is what most generic COTS vs. custom banking modernization guides miss. The modern answer is rarely binary. Leading North American banks are increasingly adopting a Composable Core approach: using COTS for non-differentiating back-office functions (general ledger, KYC, regulatory reporting) while building custom microservices for customer-facing experiences, AI capabilities, and proprietary products.

This is the pragmatic hybrid model. And it deserves explicit treatment in your modernization strategy.

The Decision Framework: 8 Dimensions for Banking CTOs

Use this framework to evaluate your modernization path across the dimensions that matter most in a regulated banking environment. This is not a generic IT matrix. Each dimension is calibrated for banking-specific trade-offs.

Decision Framework (Custom vs COTS Banking Modernization)-

| Dimension | COTS Platform | Custom Build | Composable/Hybrid |

| Regulatory & Compliance Agility | Vendor-managed updates; fast compliance rollout | Full internal control; slower cycle | COTS handles compliance layer; custom builds above it |

| Time-to-Market for New Products | Faster initial deployment (22-52 wks) | Slower (18-36 months for core) | Balanced: fast core, flexible features |

| Fintech & Ecosystem Integration | API-first COTS integrates well; some constraints | Total control over integration layer | Best of both: open APIs + custom connectors |

| Total Cost of Ownership (5-7 yrs) | Lower upfront; high licensing + upgrade costs | High upfront; lower long-term if maintained well | Moderate across both dimensions |

| Vendor Lock-in Risk | High — roadmap dependency | Low — full ownership | Medium — COTS core risk mitigated by custom layer |

| Data Strategy (AI/Analytics) | Limited data model flexibility | Full control; ideal for AI/ML use cases | Custom analytics layer on COTS data |

| Talent & Operating Model | Configuration skills; easier to outsource | Deep engineering talent needed; hard to retain | Mixed team model required |

| Cyber Resilience & Audit Trail | Vendor certified; limited deep auditability | Full auditability of proprietary logic | Hybrid: COTS core + custom logging layers |

The Hidden Costs That Will Surprise Your CFO

In 2026, the traditional "cost center" mindset is being upended. While your CFO is likely focused on interest rates and raw inflation, a set of "silent" financial drains is beginning to erode margins from the inside out.

Here are the hidden costs currently surprising the C-suite:

Hidden Costs of COTS in Banking

The RFP price is never the real price. Banks that have gone through COTS implementations consistently report cost drivers that were not visible in the initial vendor proposal:

- Annual licensing fees that escalate 5-15% per year as transaction volumes grow

- Forced upgrade cycles that consume internal engineering resources every 18-24 months

- Heavy customization layers required to match bank-specific workflows — often 30-50% of the base implementation cost

- Vendor roadmap misalignment: critical features you need may be 2-3 years away on the vendor schedule

- Exit costs: migrating data and integrations away from a deeply embedded COTS core can cost as much as the original implementation

Hidden Costs of Custom Development

Custom builds carry their own financial surprises:

- Engineering talent shortages: senior banking systems engineers command $180K-$280K base salaries in North America

- Architecture governance risk: without strong oversight, codebases drift into unmaintainable complexity

- Longer regulatory validation cycles when regulators must assess novel proprietary systems

- Internal maintenance burden: budget reallocation from innovation to maintenance typically accelerates after year 3

Legacy Modernization Patterns: Which Path Fits Your Architecture?

The choice between Custom vs COTS banking modernization is inseparable from your modernization pattern. Here are the four patterns most relevant to North American banks, and how the build-vs-buy decision plays out in each.

| Pattern | Description | Best Fit | COTS vs Custom Fit |

| Strangler Fig | Incrementally replace legacy modules; the legacy system remains active until fully replaced | Large banks with complex cores and multi-year migration timelines | Both work well; Custom for differentiating modules, COTS for commodity functions |

| Coexistence Architecture | Legacy core remains; new services run in parallel on modern infrastructure | Banks needing immediate digital capability without full core replacement | COTS new platform + custom integration layer is common here |

| Progressive Replacement | Modules replaced sequentially, starting with least critical | Regional banks with defined roadmaps and budget constraints | Strong fit for COTS replacement modules; Custom for proprietary workflows |

| Big Bang Replacement | Entire legacy system replaced in a single migration event | Regulatory-driven replacements or digital challenger bank launches | COTS is strongly preferred due to speed requirements; Custom only if strong engineering capability exists |

Most successful North American bank modernizations use the Strangler Fig or Progressive Replacement pattern. Big Bang replacements have a high failure rate in production banking environments due to operational risk.

TCO and Value Model: How to Think About Cost Over Time

A 12-month horizon will almost always favor COTS banking modernization. A 7-year horizon often reverses that advantage. Here is how to think about cost across both time frames for a representative regional bank scenario.

Scenario: Regional Retail Bank — Core Deposits and Lending Modernization

| Cost Category | COTS Platform | Custom Build |

| Initial Implementation | Medium ($5M-$15M) | High ($15M-$35M) |

| Annual Licensing (Year 1-7) | High ($2M-$8M/year, escalating) | None |

| Cloud Infrastructure | Medium (shared with vendor) | Medium (bank-managed) |

| Customization & Configuration | Medium (30-50% of license) | Medium (ongoing feature development) |

| Upgrade Cycles (forced) | High (every 18-24 months) | Controlled (bank-driven) |

| Year 7 Total Cost Estimate | $45M-$85M | $40M-$70M |

| Risk Profile | Vendor dependency, roadmap risk | Talent dependency, architecture risk |

The key insight here: COTS appears cheaper at year 1-2. By year 5-7, high-license COTS platforms can eclipse the total cost of a well-governed custom build. The inflection point typically occurs around year 4.

For CTOs preparing a board-level business case, the 7-year TCO model is a credible framing. A 12-month view will produce the wrong recommendation.

Risk and Governance: The Lens Competitors Ignore

Most COTS vs Custom banking modernization comparisons focus on cost and speed. Banking CTOs must also weight operational risk, regulatory risk, and governance complexity. Here is how each path performs.

COTS: Governance Considerations

- Vendor failure or acquisition risk: Consolidation in the core banking vendor market (Oracle, FIS, Fiserv dominance) creates single-point dependencies

- Release management complexity: COTS upgrade windows must align with the bank's regulatory and operational calendar, which is often a major constraint

- Auditability limitations: Regulators may request custom audit trails or data lineage that vendor systems do not natively support

Custom: Governance Considerations

- Internal capability risk: Losing key architects or engineers mid-program is a top failure mode in custom banking programs

- Architecture governance discipline: Without a strong enterprise architecture function, custom codebases drift toward unmaintainable complexity within 3-5 years

- Security validation: Novel proprietary systems require more extensive penetration testing and regulatory validation

When Should Banks Choose COTS, Custom, or Hybrid?

Not all banks face the same decision. Here is a bank-archetype decision guide based on organizational profile.

| Bank Archetype | Recommended Path | Primary Rationale |

| Large Tier-1 Universal Bank | Composable/Hybrid | Scale requires COTS stability; innovation requires custom differentiation layers. Data strategy demands custom analytics. |

| Regional Bank ($1B-$50B assets) | COTS with Custom Digital Layer | Speed and compliance matter; differentiation at the customer experience level, not the ledger. |

| Digital-Only Challenger Bank | COTS Cloud-Native Core + Custom UX | Speed-to-market is the top priority; COTS core with fast custom front-end delivers the best outcome. |

| Credit Union (under $1B assets) | COTS | Limited internal engineering capacity; vendor-managed compliance is a major advantage at this scale. |

| Bank with Proprietary AI/Fintech Strategy | Custom or Composable | Competitive differentiation requires full control over data models, algorithms, and integration layers. |

The CTO Decision Checklist (RFP and Steering Committee Ready)

Use these 12 questions to structure your internal modernization decision workshop or vendor RFP process.

1. How fast must the modernization program deliver visible results — months or years? (Speed pressure favors COTS banking modernization)

2. Which specific banking functions create competitive differentiation for your institution? (Differentiating functions favors Custom banking modernization)

3. How mature is your internal DevOps, product management, and engineering culture? (Immature teams favor COTS guardrails)

4. What is the regulatory change velocity for your core systems — how often do compliance requirements shift? (High velocity may favor vendor-managed COTS compliance updates)

5. How open must the platform be to fintech partners, BaaS platforms, and open banking APIs? (High integration demand can favor Custom or Composable)

6. What is your 7-year TCO budget for this initiative? (Long-term cost analysis may favor Custom over high-license COTS)

7. Do you have a realistic vendor exit strategy if COTS fails to deliver on roadmap commitments?

8. Is your data strategy (AI, real-time analytics, personalization) dependent on controlling your own data models? (Yes, favors Custom)

9. How do your regulators (OCC, FFIEC) typically view novel proprietary systems versus established COTS platforms?

10. Have you modeled the architecture impact on your existing fintech ecosystem integrations under each path?

11. What is your organization's demonstrated track record with large-scale custom software delivery in banking?

12. Is there a composable architecture approach that captures the best of both paths for your specific modernization scope?

If your answers point predominantly to speed, compliance, and limited engineering scale, COTS is your likely path. If they point to data control, differentiation, and innovation velocity, Custom or Composable is the stronger strategic choice.

Pro Tips: Businesses evaluating The CTO Decision Checklist (RFP and Steering Committee Ready) should also consider open banking in Canada to improve execution quality, scalability, and long-term operational resilience.

Note: Organizations modernizing legacy environments often evaluate core banking system migration strategy to reduce disruption while improving scalability and long-term maintainability.

Integration with the Fintech Ecosystem

One of the most under-discussed dimensions of the COTS vs. custom banking modernization debate is the long-term impact on fintech integration. North American banks are accelerating their partnerships across open banking APIs, BaaS platforms, fraud/AML systems, real-time payment rails (FedNow, RTP), and data analytics platforms.

How does your architecture choice affect ecosystem integration?

- COTS platforms increasingly offer pre-built connectors for major fintech partners — but these can be inflexible or carry additional licensing costs

- Custom architecture gives full control over the integration layer, but require dedicated API management investment

- Composable architectures with an API-first design typically perform best here — the modular structure allows selective integration without full-stack dependencies

Pro Tips:- Key principle: ISO 20022 migration timelines mean your chosen architecture must support rich data messaging across the payments ecosystem by hard regulatory deadlines. This is not optional. Evaluate every vendor platform's native ISO 20022 readiness as a mandatory RFP criterion.

Trend Insights for Banking CTOs in 2026

The modernization landscape is shifting fast. Three trends are reshaping the COTS vs Custom calculus right now:

Trend 1: AI-Assisted COBOL Migration

Large language models are being applied to document, translate, and modernize legacy COBOL codebases at speeds previously impossible. This is making Custom builds faster and less risky than they were even 24 months ago. If your legacy core is COBOL-based, this changes your Custom viability assessment.

Trend 2: SaaS-ification of Banking Cores

The shift from 'buying banking software' to 'subscribing to a banking platform' is converting COTS from a CapEx to an OpEx model. For CTOs with capital constraint pressures, this makes cloud-native COTS subscription platforms more attractive from a balance sheet perspective.

Trend 3: Low-Code/No-Code Custom Wrappers

Banks are increasingly buying COTS cores and using low-code platforms to build custom front-end experiences rapidly. This hybrid pattern reduces custom development cost by 30-40% while preserving differentiation at the customer-facing layer. It is the practical version of the Composable Core model.

Future-Proofing Your Core: Modernizing Legacy Systems with VLink

Legacy modernization in banking is not a commodity project. It requires deep domain expertise in regulated financial systems, architecture pattern experience across COTS and custom builds, and the engineering execution capability to deliver without operational disruption.

VLink’s dedicated team partners with North American banks, credit unions, and fintech-adjacent financial institutions at every stage of the modernization lifecycle:

- Legacy System Modernization

Our approach to Legacy system modernization focuses on transforming technical debt into a competitive asset. By conducting a comprehensive architecture assessment, we identify the most efficient paths for COBOL migration and full-scale core system rationalization. This ensures that your foundational technology remains resilient, scalable, and ready to integrate with modern digital ecosystems.

- Custom Software Development

We specialize in a high-impact custom software development company tailored to the unique demands of the financial sector. From building high-performance proprietary banking applications to designing robust API platforms, our team delivers the tools you need to succeed. Furthermore, we integrate AI-driven lending and risk tools to automate decision-making and enhance institutional security.

- Cloud Migration Consulting Services

Our Cloud migration consulting services are designed to help firms navigate the complexities of digital transformation. We prioritize cloud-native infrastructure design and seamless platform migration to ensure your data stays accessible and secure. To meet the strict standards of DevSecOps for regulated environments, we embed compliance and security directly into your delivery pipeline.

Our teams have delivered modernization programs for regional banks facing the exact Custom vs COTS decision this framework addresses. We bring no vendor bias to the decision. Our starting point is always your bank's competitive strategy, regulatory environment, and engineering reality.

Whether you are evaluating a COTS banking modernization platform for your core deposits system, building a custom digital lending platform, or designing a composable architecture that bridges legacy and modern infrastructure, VLink can accelerate the decision and the delivery.

Conclusion: The Decision Is Strategic, Not Just Technical

The choice between Custom vs COTS banking modernization represents one of the most consequential decisions in a CTO’s career. Beyond the immediate tech stack, this pivot point dictates innovation velocity, regulatory agility, and the bank's competitive standing for the next decade.

The data is clear: neither path wins in every scenario. COTS is not plug-and-play in banking. Custom is not always more expensive over a 7-year horizon. And the most successful modernization programs in North America are increasingly adopting a Composable Core approach — buying commodity, building differentiation.

The right answer starts with the right questions. Use the 12-question checklist in this framework to structure your internal decision process. Map your bank's archetype to the recommended path. Model the 7-year TCO across all three options before committing.

And if you need a decision partner who has navigated this terrain in real banking environments — reach out to VLink’s expert now.

Global Delivery Manager, VLink Inc.

Shivisha Patel serves as the Global Delivery Manager at VLink Inc., bringing a wealth of experience in program delivery and management, particularly in the insurance and banking sectors. She has a robust technical background with deep expertise in WebSphere MQ, WTX, IIB, middleware, and enterprise system integration.

Shivisha Patel

Shivisha Patel