The clock is ticking. And for CTOs and VPs of Digital at Canadian financial institutions, 2026 is not a soft target — it is a hard regulatory line.

Canada is entering its most significant banking transformation in decades. The Consumer-Driven Banking (CDB) Framework, backed by federal legislation (Bill C-69), mandates that designated banks give Canadians secure, standardized access to their own financial data — starting with read-only access by early 2026, followed by expanded write-access by mid-2027.

Here is what that means in practice: Over 9 million Canadians currently share their financial data through insecure screen scraping. (Source: FCAC, 2024). That practice ends with open banking. Every bank in the designated scope must transition to a regulated, API-first data-sharing ecosystem.

The stakes are large. Accenture estimates that open banking could deliver a $2.9 billion economic boost to Canada's financial sector. An EY consumer survey found that 76% of Canadians want more control over their financial data — yet security remains their top concern. That combination of demand and concern is exactly where banks need to lead, not just comply.

This blog is a practical 2026 readiness guide for bank technology and digital leaders. Not another regulatory summary — a roadmap you can take into your planning cycle.

Why 2026 Is a Structural Inflection Point for Canadian Banking

2026 is widely regarded as a structural inflection point for the Canadian banking sector because it marks the convergence of a massive credit cycle reset, a fundamental overhaul of the regulatory landscape, and the birth of a more competitive digital ecosystem.

While the "mortgage cliff" was once the primary concern, the shift is now defined by a transition from a stable, high-barrier-to-entry "old world" to a more volatile, consumer-directed "new world."

- The Shift from Screen Scraping to Consumer-Driven Banking

Screen scraping is how most Canadians share their data today. Users hand over their banking credentials to fintech apps, which then log in and pull data on their behalf. It is insecure, unreliable, and — under the new framework — it will no longer be the standard.

Open banking in Canada replaces that with direct, tokenized API connections governed by clear rules on consent, security, liability, and data use. For banks, this is a foundational architecture change — not a feature update.

- Why Compliance-Only Strategies Will Fail

Banks that treat open banking as a checkbox exercise will miss the point. A compliance-only posture — building the minimum API capability to satisfy the FCAC — means ceding ground to fintechs and neobanks who will use the same infrastructure to launch embedded finance software solutions and products, aggregation tools, and data-driven offers.

The banks that win in a post-2026 world will be those who treat open banking Canada as a modernization catalyst, not a regulatory burden. PwC Canada puts it plainly: banks that approach this as a "compliance check" will lose market share to "Bank-as-a-Platform" competitors.

That window is narrow. Most banks need 18 to 24 months to reach Phase 1 readiness. That means meaningful planning and investment must begin now.

What Is Open Banking in Canada and How It Will Actually Work

Open banking — officially called Consumer-Driven Banking (CDB) in Canada — gives consumers the legal right to share their financial data with accredited third-party providers (TPPs) through secure, standardized APIs. The data belongs to the consumer. They decide who sees it, and they can revoke access at any time.

The philosophy is simple: The data belongs to you, not the bank. You decide who sees it, what they use it for, and you can "unplug" their access at any moment.

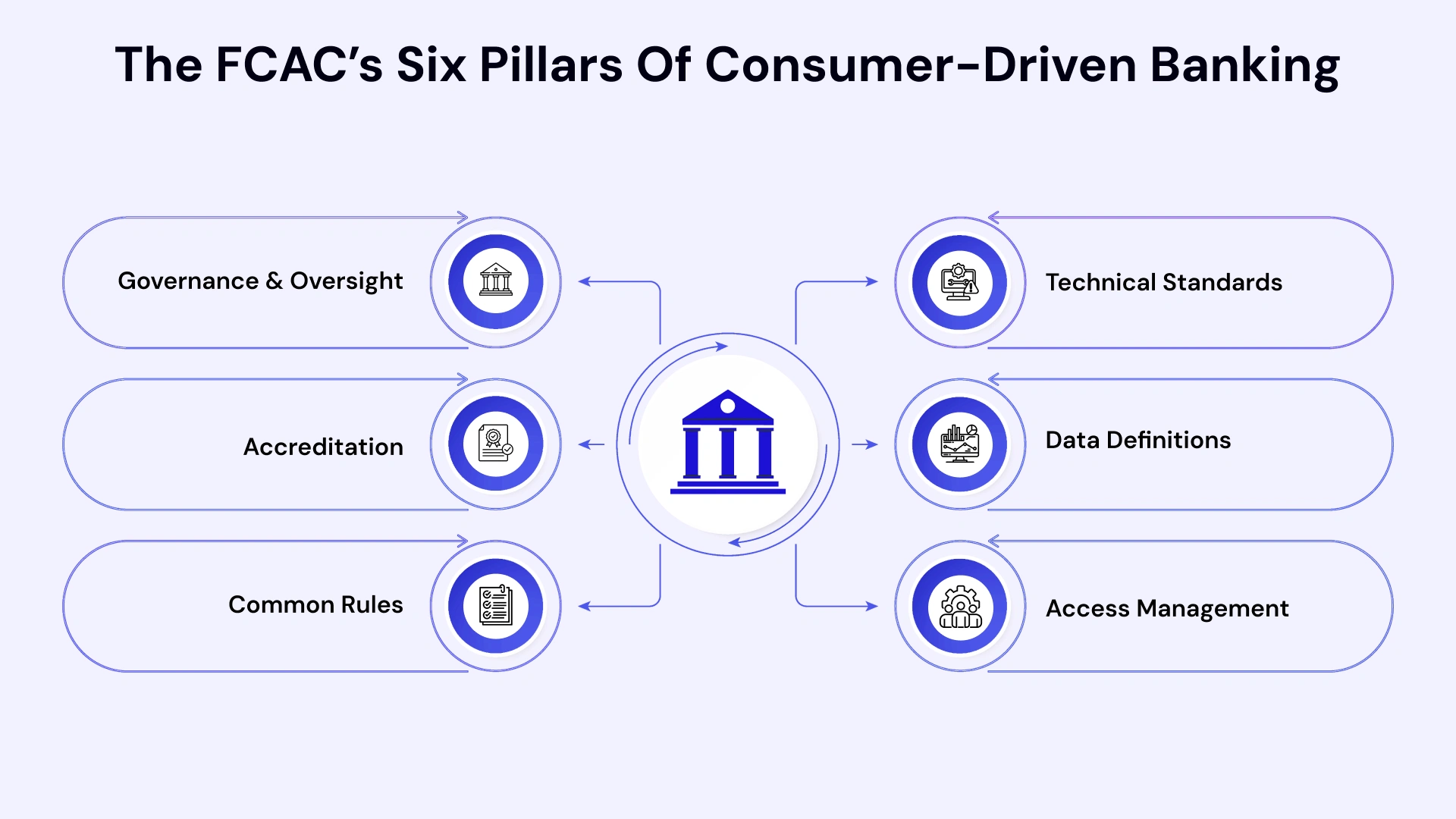

How the Framework Protects You

To make this work safely, the Financial Consumer Agency of Canada (FCAC) has established a framework built on six critical pillars:

- Governance & Oversight: Clear rules on who runs the system.

- Accreditation: Only vetted, secure companies get to participate.

- Common Rules: Uniform standards for privacy, liability (who pays if something goes wrong), and security.

- Technical Standards: Moving away from risky "screen scraping" (sharing your password) to secure APIs.

- Data Definitions: Ensuring all banks speak the same digital language.

- Access Management: Giving consumers a "dashboard" view of who has their data.

The framework adopts the FDX (Financial Data Exchange) standard. Since this is already the benchmark in the U.S., it ensures that Canadian fintechs can scale and stay compatible with global partners.

The Rollout: What Data Can You Share?

Canada is taking a phased approach to ensure the plumbing is leak-proof before turning on the high-pressure taps.

| Feature | Phase 1 (The "Read" Phase) | Phase 2 (The "Action" Phase) |

| Timeline | Immediate / Current Rollout | Expected Mid-2027 |

| Capabilities | Read-only access. Apps can see your data to provide insights. | Write access. Apps can move money or trigger actions. |

| Included Data | Chequing/savings accounts, credit cards, and investment products. | Payment initiation and seamless account linking. |

| Backbone | Secure API connectivity. | Integration with the Real-Time Rail (RTR) for instant payments. |

Canada's Open Banking Timeline: 2024 to 2027 at a Glance

Timeline — 2024 to 2027 with phase milestones

| Phase | Period | Key Milestones |

| Foundation | 2024 – Q1 2025 | Federal Budget 2024 commits to open banking in Canada; Bill C-69 introduced; FCAC named as lead regulator; FDX standards scoping begins |

| Standards & Supervision | Q2 2025 – Q4 2025 | Technical standards published; accreditation process opens for TPPs; banks begin sandbox development |

| Phase 1: Read-Only Access | Early 2026 | Mandatory read-only API access goes live; chequing, savings, credit card, and investment data in scope; screen scraping begins phase-out |

| Phase 2: Write Access | Mid-2027 | Write-access APIs enabled; Real-Time Rail integration; expanded product scope; embedded finance use cases activate |

The sequencing matters. Phase 1 is about foundational infrastructure — building it right matters more than building it fast. But building it slowly is not an option.

Open Banking Regulation: What CTOs Must Translate Into Technology

In 2026, Canada’s Consumer-Driven Banking (CDB) framework has moved from policy to production. For a CTO, this isn't just a compliance check—it’s a fundamental re-architecting of how your institution handles data sovereignty, identity, and third-party risk.

Open Banking Regulations

- Governance and Oversight Requirements

The FCAC holds primary oversight. Banks must demonstrate that their open banking in Canada programs are governed at a senior leadership level — which means the CTO and CRO must be aligned and accountable. Regulatory reporting automation is expected from day one.

- Accreditation and Third-Party Provider Standards

Banks will not just be data providers — they will also be gatekeepers. Only accredited TPPs will receive API access. Banks must build TPP onboarding and vetting workflows that verify credentials, enforce contractual data-use limits, and automate revocation when accreditation lapses.

- 24/7 API Availability Mandates

This is a hard technical requirement. Consumer-Driven Banking APIs must be available around the clock with defined uptime SLAs. For banks still running batch-based core systems, this is a wake-up call. Legacy core architectures that cannot support real-time API calls will need an abstraction or middleware layer to bridge the gap.

- Liability Follows Fault: Technical Implications

The CDB framework adopts a "liability follows fault" principle. If a data breach occurs because of a bank's API failing, the bank owns the liability. If a TPP misuses the data, the TPP is liable. For CTOs, this means ironclad logging, audit trails, and incident response playbooks tied directly to API activity.

- Overview:-

| Regulatory Requirement | Required Technical Control | Owner | Timeline |

| FCAC governance reporting | Automated compliance dashboard | CTO / CRO | Q4 2025 |

| TPP accreditation enforcement | API gateway with credential checks | Architecture Team | Q3 2025 |

| 24/7 API availability | Real-time API layer + monitoring | Platform Engineering | Q1 2026 |

| Liability and audit logging | Immutable API event logs | Security & Compliance | Q4 2025 |

| Consent management | Centralized consent engine | Product + Engineering | Q4 2025 |

| Data minimization | Scoped token access controls | Data Governance Team | Q1 2026 |

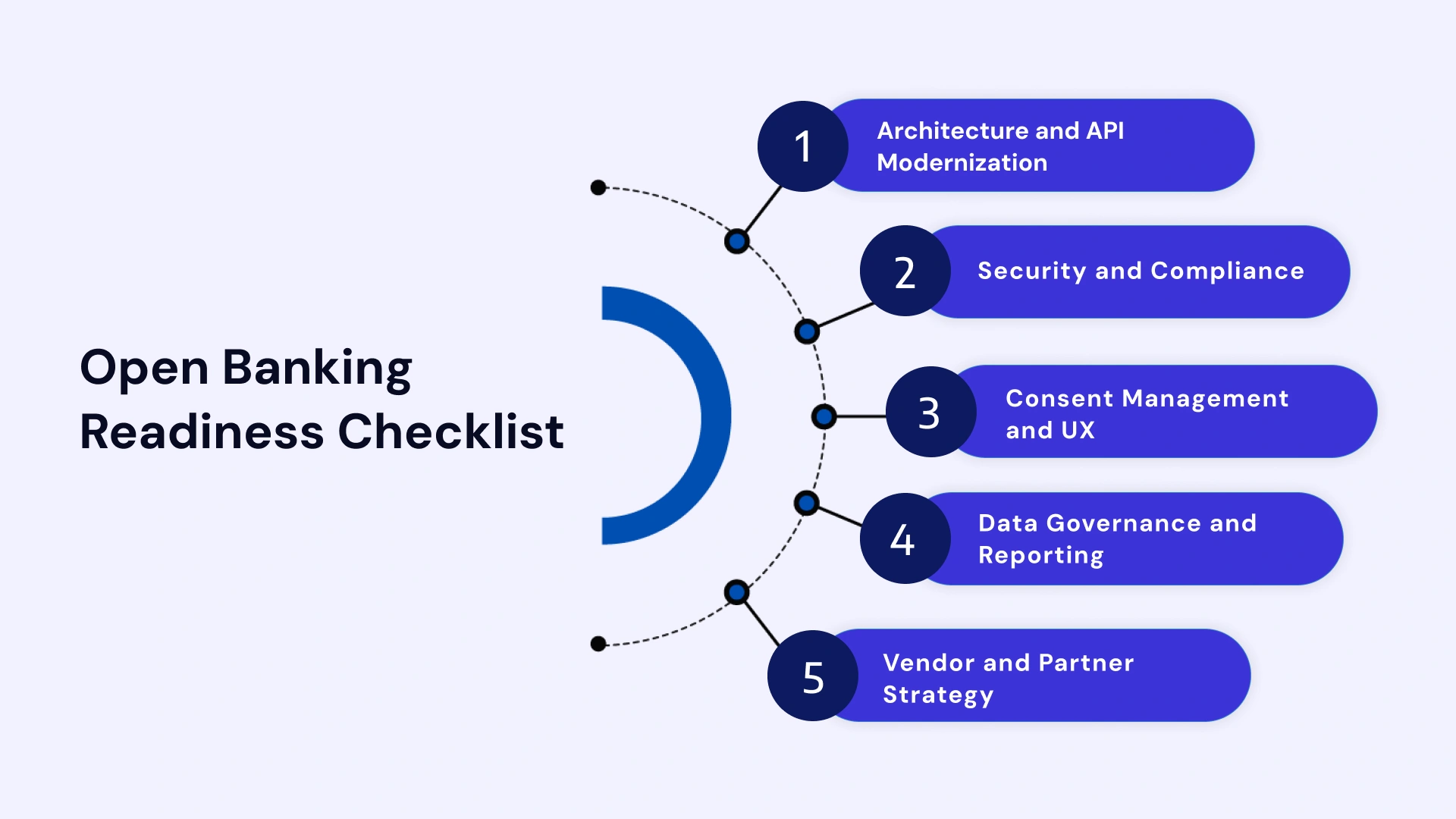

A 2026 Open Banking Readiness Checklist for Canadian Banks

This section is your starting point for internal planning. Use this as a working checklist with your team — across architecture, security, product, and data governance.

A. Architecture and API Modernization

- Build an API abstraction layer to decouple core banking from the open banking Canada interface

- Adopt FDX data specifications for all shared data structures

- Stand up a developer sandbox for TPP testing — separate from production environments

- Implement observability and real-time monitoring across all open banking in Canada API endpoints

- Assess your core banking platform's ability to serve real-time API calls — not just batch

B. Security and Compliance

- Implement OAuth 2.0 with multi-factor authentication for all API access flows

- Enforce TLS 1.3 encryption end-to-end across all data in transit

- Build incident response runbooks specifically for API security events

- Align your cybersecurity posture with open banking in Canada' security standards under the CDB framework

- Engage a managed cybersecurity services partner to support 24/7 API threat monitoring

C. Consent Management and UX

- Deploy a centralized consent dashboard that gives users full visibility and control

- Build granular revocation flows — consumers must be able to withdraw access immediately

- Timestamp and log every consent event with an immutable audit trail

- Design the consent UX to be clear and accessible — not buried in legal language

D. Data Governance and Reporting

- Complete a full data mapping exercise: where does consumer data live across your enterprise?

- Apply data minimization principles — share only what is required and consented to

- Automate FCAC regulatory reporting pipelines

- Build data classification and lineage tracking into your governance framework

E. Vendor and Partner Strategy

- Evaluate open banking Canada platform vendors against FDX compatibility, security certifications, and Canadian regulatory alignment

- Define your build vs. buy vs. hybrid approach early — mid-course changes are expensive

- Run interoperability testing with TPPs in your sandbox before production launch

Use this maturity model to benchmark your current state and set your 2026 target:

| Maturity Level | Description | Minimum Capability |

| Level 1: API Hygiene | Basic compliance readiness | FDX-aligned APIs live; OAuth 2.0 in place; uptime SLA met |

| Level 2: Consent-Centric Architecture | Consumer trust and control built in | Centralized consent dashboard; granular revocation; full audit logging |

| Level 3: Embedded Finance Platform | Strategic market leadership | TPP partner ecosystem active; embedded finance products live; data-driven cross-sell enabled |

Segmented Roadmap: Big 6 vs. Tier-2 vs. Digital-Only Banks

Not every bank starts from the same place. Your open banking in Canada roadmap should reflect your actual architecture, legacy state, and competitive position.

- Big 6 Banks: Scaling Existing API Programs

Canada's largest banks — RBC, TD, Scotiabank, BMO, CIBC, and National Bank — already have API programs in some form. For them, the challenge is standardization, not starting from scratch. The priority is migrating internal APIs to FDX specifications, enforcing TPP accreditation at scale, and governing consent management across millions of customers.

RBC's early partnership with fintechs like Wealthsimple is a visible example of the co-opetition model that open banking Canada will accelerate.

- Regional and Tier-2 Banks: Modernization Under Constraint

Mid-size banks and regional credit unions face the sharpest tradeoffs. They may lack dedicated open banking Canada engineering teams and face budget constraints that make a full-stack rebuild unrealistic. The smarter play is an API abstraction layer deployed on managed cloud services — essentially a middleware that connects legacy core systems to a modern, FDX-compliant API interface without replacing the core itself.

One Tier-2 bank benchmarked in industry research achieved this transition in 18 months through a hybrid approach combining a cloud-native middleware with a cybersecurity service provider overlay.

- Digital-Only Banks: Platform Advantage

Canada's digital-native institutions — EQ Bank is the clearest example — have already built API-first architectures. EQ Bank's cloud-native foundation allows it to aggregate external account data into its own app, positioning it as a financial hub rather than just a bank.

For digital banks, the 2026 deadline is less a compliance burden and more a market opening: the new TPP ecosystem gives them partners, distribution channels, and data they previously could not access.

Strategic Opportunities Beyond Compliance

Several strategic opportunities have emerged for banks to monetize the new ecosystem. Such as:-

- Becoming the Financial Aggregator

Open banking's "read" mandate is actually the first step toward a much larger strategic position. Once your APIs are live and your consent infrastructure is mature, you can begin ingesting data from other institutions — with user permission. That gives you a 360-degree view of your customer's total financial picture. Banks that build this capability first become the primary financial relationship, not just one of several.

- Embedded Finance and Platform Banking

The next frontier is embedding your banking services where customers already live — inside payroll platforms, e-commerce checkouts, accounting software, or real estate transactions. Open banking Canada is the infrastructure that makes embedded finance possible. Deloitte's research frames this as a "Trust Premium": the first bank to offer a seamless, secure data-sharing experience will capture the Gen Z and Millennial demographic for the long term.

- Cross-Border Interoperability via the FDX Standard

Canada's alignment with FDX is not accidental. The U.S. Consumer Financial Protection Bureau (CFPB) has also moved toward FDX-compatible open banking in Canada rules. For Canadian banks with U.S. operations, building to FDX now means your API infrastructure is interoperable across borders — reducing future integration costs and opening cross-border partnership opportunities.

- Executive Overview:-

| Strategy | Risk if Missed | Upside if Captured |

| Compliance Only (Level 1) | Minimum regulatory exposure | None — fintechs capture relationship value |

| Data Aggregation (Level 2) | Customer attrition to aggregator apps | Full financial picture; upsell and retention advantage |

| Embedded Finance Platform (Level 3) | Competitive irrelevance vs. fintech platforms | New revenue streams; partner ecosystem; Gen Z acquisition |

How to Choose the Right Open Banking Partners

Here is a framework for evaluating and choosing open banking partners in the current Canadian landscape.

- Evaluating Open Banking Vendors

The vendor landscape for open banking infrastructure falls into three categories: API infrastructure providers (who handle the connectivity layer), middleware platforms (who bridge legacy core to open APIs), and full-stack open banking platforms (who offer end-to-end solutions including consent management, TPP onboarding, and compliance reporting).

- API Infrastructure vs. Middleware vs. Platform Providers

For Big 6 banks with existing API programs, an API infrastructure enhancement with FDX overlay is usually the right fit. For Tier-2 banks with legacy cores, a middleware provider that decouples the core from the consumer interface is the lowest-risk path. For digital banks, a full-stack platform partner accelerates time-to-ecosystem.

- Build vs. Buy vs. Hybrid Framework

| Approach | Best For | Key Risk |

| Build in-house | Big 6 with large engineering teams and existing API programs | High cost; long timelines; requires deep open banking expertise |

| Buy (vendor platform) | Tier-2 banks needing speed and compliance certainty | Vendor lock-in; customization limits |

| Hybrid (middleware + internal build) | Banks with legacy cores but some internal capability | Integration complexity; requires strong architecture governance |

- Security-First Partner Criteria

Any open banking Canada vendor you engage must be evaluated on five non-negotiable security criteria: FDX certification status, OAuth 2.0 and FAPI compliance, incident response SLAs, data residency (Canadian data must stay in Canada), and third-party penetration testing cadence. Do not shortcut this evaluation — liability follows fault, and your vendor's security posture becomes your exposure.

VLink: Engineering the Future of Finance

VLink is a technology partner purpose-built for financial institutions navigating digital transformation. We help Canadian banks move from regulatory obligation to competitive advantage — across the full open banking technology stack.

Our capabilities span mobile app development, custom software development, managed services, and finance software solutions. We have worked with financial institutions to build API abstraction layers, deploy consent management engines, and architect the cloud-native infrastructure for open banking in Canada demands.

Whether you are a Big 6 bank scaling your existing API program or a Tier-2 institution modernizing under constraint, our teams understand the regulatory, technical, and operational dimensions of open banking readiness in the Canadian market.

We do not just advise on open banking in Canada' strategy — we build the systems that make it work, on time and within scope.

Conclusion

The 2026 deadline is real. But the real opportunity is larger than compliance. Canadian banks that approach open banking as a modernization catalyst — rather than a regulatory burden — will emerge from this transition with stronger customer relationships, new revenue streams, and an API-first architecture that positions them for the embedded finance era.

The banks that wait for certainty before acting will find the window closed by the time they start. The planning, budgeting, and architecture decisions that determine your 2026 readiness need to happen now.

Use the readiness checklist in this guide as your starting framework. Assess your maturity level. Define your path from Level 1 compliance to Level 3 platform leadership. And choose technology partners who understand both the regulatory landscape and the infrastructure demands of what comes next.

Global Delivery Manager, VLink Inc.

Shivisha Patel serves as the Global Delivery Manager at VLink Inc., bringing a wealth of experience in program delivery and management, particularly in the insurance and banking sectors. She has a robust technical background with deep expertise in WebSphere MQ, WTX, IIB, middleware, and enterprise system integration.

Shivisha Patel

Shivisha Patel