AI in debt collection is revolutionizing how banks and fintech lenders manage overdue accounts, driving efficiency, cost reduction, and enhanced customer engagement through data-driven automation and predictive analytics.

This global growth, with North America holding a dominant market share (over 30% in the highly specialized AI for Debt Collection market), underscores the critical need for sophisticated solutions. AI debt collection solutions enable up to 8x faster operations, a 2–4x boost in collector productivity, and a 25%+ cut in loan delinquencies, with response rates soaring up to tenfold and debtor coverage costs potentially falling by 70%.

This fundamental shift from a reactive, one-size-fits-all approach to a proactive, personalized strategy is not just about streamlining processes; it delivers measurable upticks in recovery rates, compliance, and profitability, making it a critical area of investment for financial organizations seeking an edge in this multi-billion-dollar sector.

AI in Debt Collection: Market Overview and Key Trends

AI debt collection solutions are rapidly being adopted in the financial sector, automating tasks, personalizing communication, and transforming the way lenders and agencies approach credit risk, account prioritization, and debtor engagement.

The Banking, Financial Services, and Insurance (BFSI) segment is the dominant market shareholder, recognizing the immense value of this technology for managing vast loan portfolios.

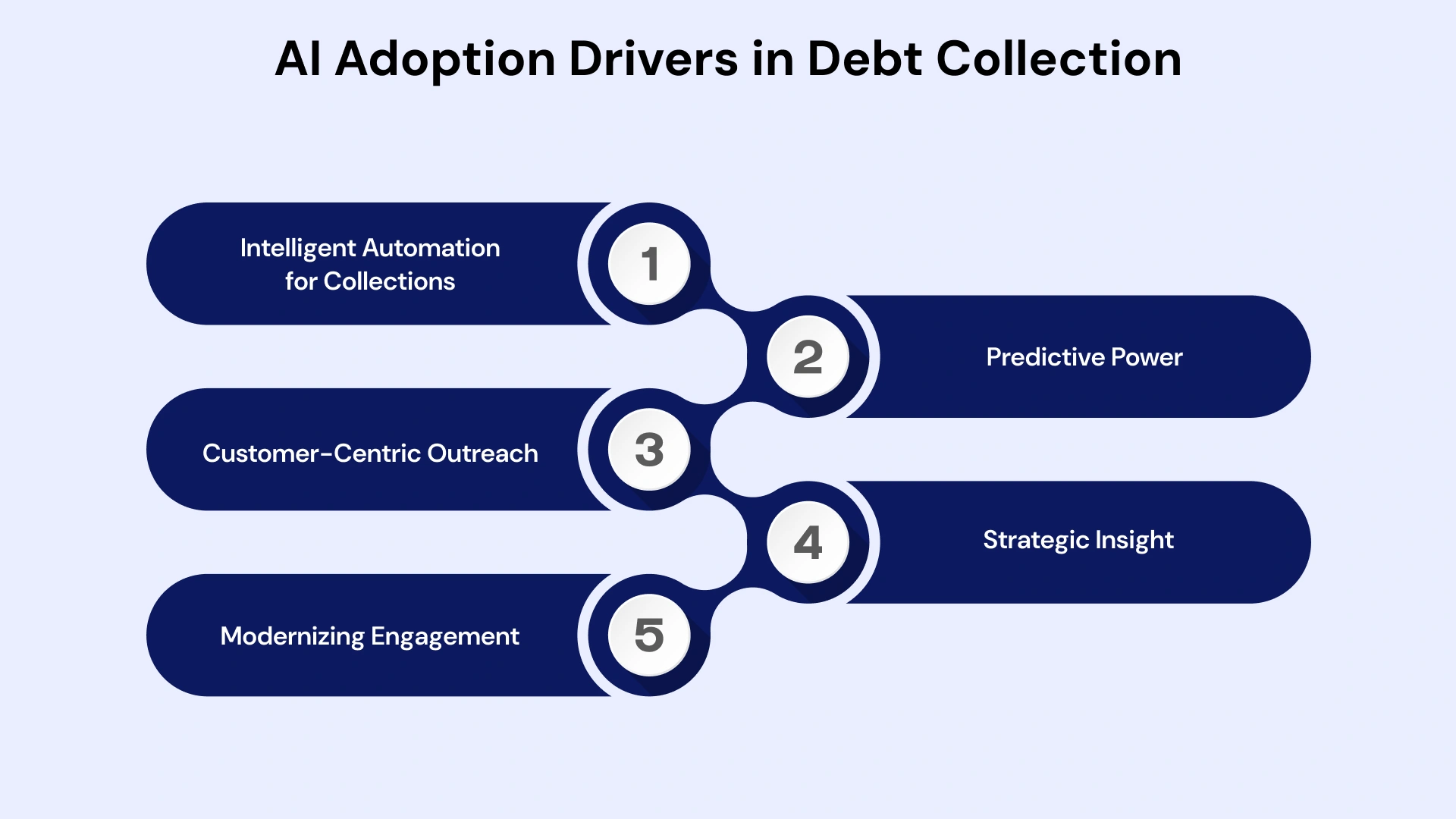

Key trends fueling the adoption of AI Development Services in debt collection include:

- Intelligent Automation for Collections: End-to-end debt collection automation with AI of workflows, from initial reminders to legal escalation. This uses debt-collection technology, such as Robotic Process Automation (RPA), seamlessly integrated with machine learning models.

- Predictive Power: Enhanced machine learning in debt collection for hyper-accurate AI for loan default prediction and nuanced customer segmentation, moving beyond traditional scoring methods.

- Customer-Centric Outreach: NLP-powered debt collection chatbots and virtual agents for compliant, 24/7 self-service engagement, improving overall debtor experience.

- Strategic Insight: Debt collection predictive analytics for real-time credit risk analytics using AI and optimizing resource allocation.

- Modernizing Engagement: AI-powered debt recovery portals supporting seamless, AI-powered self-service payment portal options for debtors.

The increasing complexity of regulations and the sheer volume of delinquent accounts are pushing institutions to seek out advanced AI debt collection solutions to maintain both efficiency and compliance.

10 Strategic Benefits of AI in Debt Collection

For commercial banks and fintech lenders, implementing AI in debt collection provides a broad spectrum of commercial advantages that directly impact the bottom line and long-term customer relationships.

1. Elevated Debt Recovery Rates and Strategic Focus

By moving beyond simple FICO scores and static rules, AI in debt collection employs sophisticated machine learning models to analyze hundreds of internal and external data points—from payment history and channel engagement to macro-economic indicators. This enables the model to accurately predict an individual's propensity to pay and identify their optimal cure strategy.

This precision ensures collection efforts are focused on accounts with the highest probability of successful recovery, leading to reported improvements of 25% or more in recovery rates. The use of AI for accounts receivable collections and other loan types becomes highly efficient.

2. Significant Reduction in Operational Costs

Debt collection automation with AI is a powerful lever for cost savings. It handles the bulk of high-volume, low-value interactions and administrative tasks—such as sending personalized reminders, updating CRM records, and processing basic payments.

This intelligent automation for collections drastically reduces the necessity for large, expensive call center teams dedicated to routine work, often cutting debtor coverage and operational overhead costs by up to 70%.

3. Real-Time Credit Risk Analytics and Dynamic Prioritization

Unlike static monthly reporting, AI provides real-time credit risk analytics, enabling dynamic account prioritization. Accounts are continuously rescored using AI-based risk scoring for collections, based on live engagement data, communication history, and any shifts in external financial indicators.

This means an account showing sudden, unexpected high-risk indicators is immediately flagged for a proactive, high-touch intervention, long before it escalates to a serious default. This ensures optimal use of limited agent time.

4. Hyper-Personalized Communication for Better Engagement

The core of effective AI-powered debt recovery is personalized communication. AI for personalized repayment reminders uses Natural Language Processing (NLP) to dynamically determine the most effective communication channel (SMS, email, app notification, phone call), the optimal time of day for outreach, and the most empathetic yet firm message tone.

This level of customization, based on historical debtor behavior, significantly increases debtor response rates—sometimes tenfold—making the interaction feel less adversarial and more collaborative.

5. Guaranteed Regulatory Compliance and Risk Mitigation

One of the most critical advantages for US and Canadian institutions is regulatory certainty. Modern AI debt collection solutions enforce compliance by design. They provide a digital, auditable trail for every action.

Furthermore, NLP for debt collection can monitor agent-debtor conversations (both live and automated scripts) in real time, instantly flagging or stopping interactions that violate strict regulations such as the FDCPA, CFPB rules, or local consumer protection laws, providing greater compliance assurance.

6. Boosted Collector Productivity and Strategic Focus

AI tools for debt recovery teams function as an advanced co-pilot. By offloading up to 90% of routine interactions to automated channels and bots, the system frees up skilled human agents.

The AI doesn't just automate; it provides agents with prescriptive insights through AI-based optimization of collection strategies (e.g., "The best offer for this customer is a 20% principal discount with a 6-month installment plan"). Agents can then focus their expertise on complex negotiations and high-value, sensitive accounts, maximizing their human potential.

7. 24/7 Self-Service and Enhanced Customer Satisfaction

Modern debtors expect convenience. The deployment of top AI chatbots for debt collection and fully functional AI-powered self-service payment portals gives customers the power to resolve their debts on their own terms, at any time.

They can check their balance, resolve disputes, and set up an AI-driven repayment schedule optimization plan without ever speaking to an agent. This reduces friction, improves the overall customer experience, and dramatically increases the conversion rate for self-cured accounts.

8. Superior Early Loan Default Prediction

Machine learning in debt collection is a powerful tool for loss prevention. AI for loan default prediction models analyzes subtle, early-stage behavioral signals that precede formal delinquency—such as changes in credit card spending habits or a sudden shift in login frequency.

By identifying borrowers at risk before the first missed payment, institutions can deploy proactive, preventive outreach strategies, such as offering financial counseling or temporary loan restructuring, dramatically reducing expected credit losses.

9. Dynamic and Optimized Repayment Schedule Planning

Generic repayment plans often fail because they don't align with a debtor's financial reality. AI-driven repayment schedule optimization analyzes a debtor's income frequency, debt-to-income ratio, and willingness-to-pay profile to suggest or automatically offer an adaptive payment plan.

This flexibility—such as aligning payment dates with salary cycles or allowing variable installment amounts—significantly improves the success rate of payment arrangements compared to rigid, standard plans.

10. Future-Proofing and Scalability through AI Development Services

Investing in AI in debt collection through specialized AI Development Services and Software Development Services future-proofs the organization. The models continuously learn and improve with every interaction, ensuring the collections process becomes incrementally smarter over time.

The cloud-native architecture of modern AI debt collection solutions enables institutions to scale their collection capacity instantly during economic downturns or periods of portfolio growth, without the need to hire and train large new call center staff.

In summary, the strategic value of AI is not just in cost savings, but in creating a smart, compliant, and scalable system that preserves customer relationships. For banks and fintech lenders, adopting these AI debt collection solutions transforms collections into a reliable, high-performing strategic asset, crucial for managing risk and maximizing lifetime customer value.

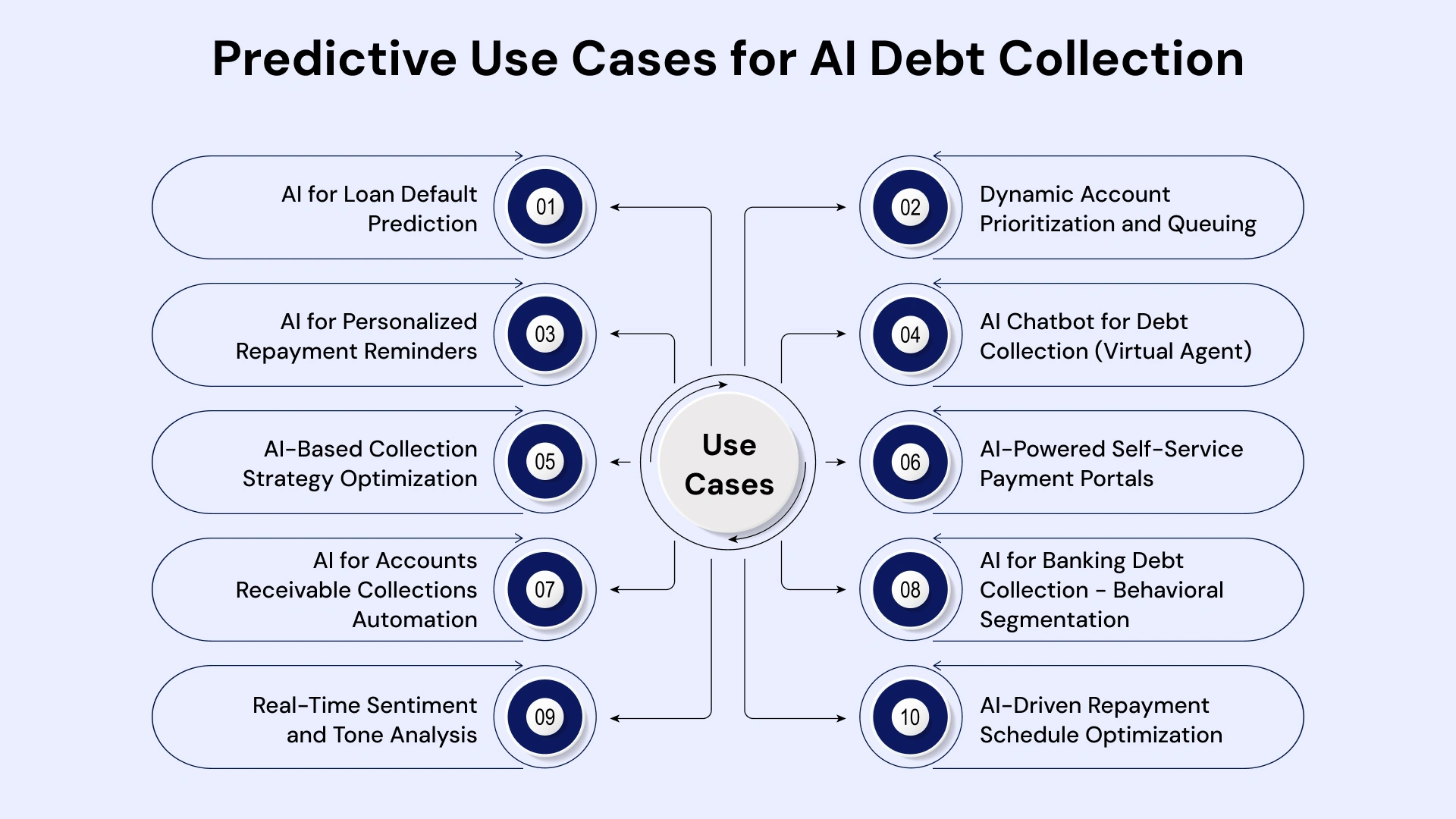

Top 10 Predictive Use Cases for AI Debt Collection

These real-world predictive AI debt-collection use cases demonstrate the power of predictive analytics to drive superior outcomes for banks and fintech lenders.

1. AI for Loan Default Prediction

- Mechanism: Machine learning models are trained on historical payment data, usage patterns, credit bureau information, and even macroeconomic trends.

- Action: It identifies individual borrowers with a high probability of default over the next 30-90 days, enabling preemptive intervention.

- Key Value: Moving from reactive collections to proactive loss prevention and management, particularly effective for AI for personal loan collections and revolving credit.

2. Dynamic Account Prioritization and Queuing

- Mechanism: Continuous AI risk scoring for collections based on multiple factors: Propensity-to-Pay score, Collection-Strategy-Effectiveness score, and current credit risk.

- Action: The system dynamically ranks the account queue in real time, ensuring human agents always work on accounts where their intervention will generate the highest expected value.

- Key Value: Maximizing collector productivity and ensuring resources are never wasted on low-probability accounts or those that will self-cure.

3. AI for Personalized Repayment Reminders

- Mechanism: The AI analyzes past response rates, time-of-day effectiveness, and preferred communication methods stored in the AI debt management system.

- Action: It selects the optimal channel, message, and time to send the initial soft reminder, maximizing the chance of a payment or engagement without a human call.

- Key Value: Driving up self-cure rates and cutting down the cost-to-collect on early-stage delinquencies.

4. AI Chatbot for Debt Collection (Virtual Agent)

- Mechanism: Uses NLP for debt collection and complex dialogue management to handle structured, repetitive debtor inquiries.

- Action: Provides 24/7 service for balance checks, clarification of simple disputes, and automated, compliant setup of payment arrangements.

- Key Value: Drastically reducing call center wait times and providing modern, instant service to debtors.

5. AI-Based Collection Strategy Optimization

- Mechanism: Prescriptive analytics models evaluate thousands of historical collection paths and their outcomes.

- Action: The AI suggests the single "next best action" for a specific account—be it a call, an email, a particular offer (e.g., principal reduction), or an automatic escalation to legal.

- Key Value: Removing guesswork from the collection process and ensuring a tailored approach to achieve higher success rates across categories such as AI for SME loan recovery.

6. AI-Powered Self-Service Payment Portals

- Mechanism: Integration of the predictive model into the customer-facing interface.

- Action: The portal uses the AI's data to present the debtor with the pre-approved, optimal payment plan immediately upon logging in, streamlining the resolution process.

- Key Value: High conversion rates for self-service payments, a cornerstone of effective debt collection automation.

7. AI for Accounts Receivable Collections Automation

- Mechanism: Specific models tailored for B2B transactions, focusing on invoice aging, contract terms, and corporate payment cycles.

- Action: Automates the sequencing of reminders and formal notices for past-due commercial invoices, ensuring timely follow-up.

- Key Value: Faster cash conversion and better management of commercial credit lines for large financial institutions.

8. AI for Banking Debt Collection - Behavioral Segmentation

- Mechanism: Machine learning identifies subtle behavioral clusters (e.g., "Digital-Only Responders," "Hardship Avoiders," "One-Time Defaulters").

- Action: The entire collection strategy is customized based on these psychological and behavioral segments, not just the debt amount or age.

- Key Value: Deploying more effective, segment-specific strategies that increase engagement, particularly for high-volume portfolios managed by AI for banking debt collection.

9. Real-Time Sentiment and Tone Analysis

- Mechanism: Uses advanced NLP for debt collection and voice analytics during live agent-debtor calls.

- Action: The system monitors the emotional tone and sentiment of the conversation, alerting the agent in real time if the interaction is escalating or noncompliant.

- Key Value: Minimizing costly disputes, preserving customer relationships, and ensuring compliance, especially critical for sensitive AI for mortgage loan collections.

10. AI-Driven Repayment Schedule Optimization

- Mechanism: Prescriptive modeling analyzes a debtor's income predictability and historical debt repayment capacity.

- Action: Automatically generates an adaptive, customized repayment schedule (e.g., lower payments initially, higher payments later) that the debtor is statistically most likely to complete.

- Key Value: Significantly increasing the long-term success of payment arrangements and reducing the likelihood of re-default.

These 10 predictive use cases illustrate how debt collection predictive analytics leverages data to shift collections from guesswork to a precise science. By leveraging machine learning in debt collection, financial institutions can move beyond reactive measures, ensuring every interaction is the most effective and profitable possible.

Commercial Applications Across Loan Categories

AI in debt collection is versatile, with specialized AI debt collection solutions available for every major loan category, ensuring compliance and effectiveness across the diverse portfolios of banks and fintech lenders.

AI for Credit Card Debt Collection

Credit card accounts are high-volume, dynamic, and often carry higher risk. AI for credit card debt collection targets these high-risk revolving accounts by monitoring real-time spending and payment behaviors to deploy optimal, legally compliant strategies immediately. Predictive models here focus on early-stage intervention to prevent the account from maxing out or being charged off.

AI for Personal Loan Collections

Personal loans require a greater degree of empathy and personalization. AI for personal loan management system collections tailors outreach to offer flexible repayment options, such as loan restructuring or temporary forbearance, based on the customer's predicted repayment ability, leading to higher conversion and retention rates.

AI for SME Loan Recovery

Small and Medium Enterprise (SME) loans have unique risk profiles tied to business cycles and commercial events. AI for SME loan recovery enhances segmentation accuracy, providing customized strategies that factor in cash flow patterns, industry trends, and invoice aging, which are critical for successful commercial collections.

AI for Mortgage Loan Collections

Mortgages are the most valuable and sensitive debt category. AI for mortgage loan collections automatically identifies distressed accounts and suggests complex repayment alternatives, such as loan modifications, forbearance, or short sales. The AI debt collection workflow automation ensures that all offers are fully compliant and documented to meet rigorous regulatory requirements, providing agents with all necessary data for complex negotiations.

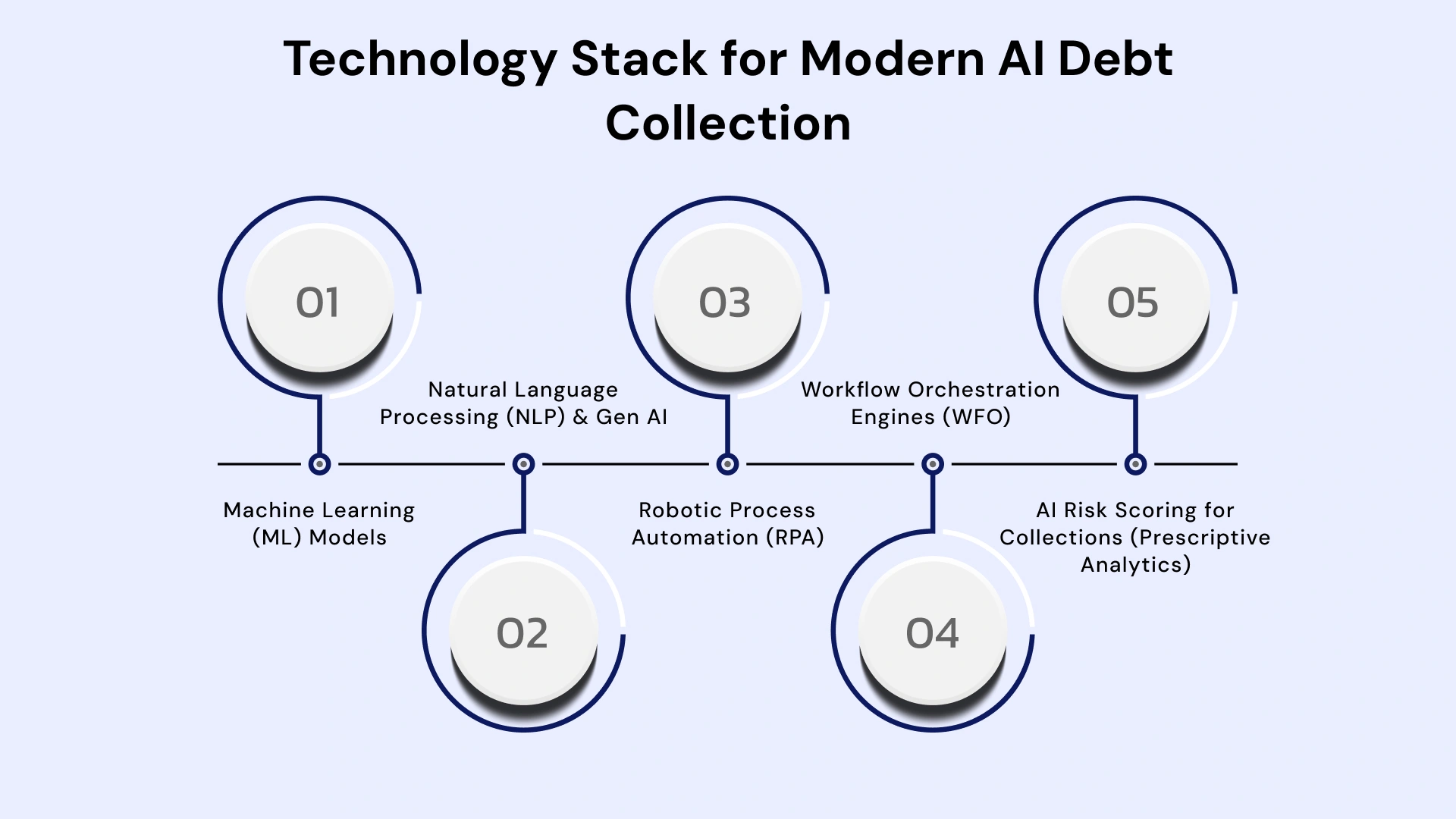

Technology Stack: AI Debt Collection Solutions

A robust AI in a debt collection platform is built on a sophisticated, integrated stack of modern debt collection technology. These components work synergistically to deliver comprehensive intelligent automation for collections, moving beyond simple task automation to accurate data-driven decision-making.

Machine Learning (ML) Models:

The foundational core engine for predictive analytics in debt collection. ML models ingest vast historical and real-time data to build specialized scoring systems, including the Propensity-to-Pay (the likelihood that a customer will make a payment), Channel Preference (the most effective outreach method), and the optimal Cure Strategy (the best offer/plan to resolve the debt). This is where the true AI for loan default prediction occurs.

Natural Language Processing (NLP) & Generative AI:

Powers all conversational and text-based elements. NLP enables the AI chatbot for debt collection and virtual agents to understand and generate human language. Crucially, it facilitates real-time compliance monitoring and sentiment analysis, interpreting a debtor’s tone (e.g., frustration, willingness to comply) to dynamically adjust the automated response or provide human agents with immediate guidance.

Robotic Process Automation (RPA):

The engine for high-volume, rules-based execution. RPA is used for debt collection automation of repetitive administrative tasks, like:

- Data entry and validation across disparate systems.

- Updating core banking and legacy systems after a payment is made.

- Generating and dispatching standardized legal notices, letters, or reports.

Workflow Orchestration Engines (WFO):

This provides the essential backbone for AI debt collection workflow automation. The WFO engine dynamically sequences and routes accounts based on the predictive scores from the ML models. It determines the "next best action," automatically triggering the appropriate step: sending a personalized SMS, nudging the AI-powered self-service payment portals, or escalating the case to a human agent.

AI Risk Scoring for Collections (Prescriptive Analytics):

These are specialized, highly dynamic algorithms responsible for credit risk analytics using AI. Unlike static credit scores, this component constantly recalculates a debtor's risk profile based on dozens of factors, including real-time engagement and behavioral signals. It provides agents with prescriptive guidance, specifying the specific action to take to maximize the probability of recovery.

These technologies consolidate diverse data sources into a unified AI debt management system, ensuring the entire collection process is data-driven, compliant, and highly efficient.

Workflow Automation: AI Debt Collection Process

The shift to AI debt collection workflow automation transforms the traditional, linear collections process into a dynamic, intelligent loop:

1. Ingestion & Scoring: New accounts enter the system, and credit risk analytics using AI immediately generate initial scores (Propensity to Pay, Cure Strategy, Best Channel).

2. Automated Outreach (Self-Cure): The workflow engine deploys the lowest-cost, most effective non-human action (e.g., a personalized SMS reminder or an email linking to AI-powered self-service payment portals).

3. Dynamic Segmentation: If the automated outreach fails, the AI re-scores the account and determines the next step. It may be an AI chatbot for debt collection or auto-escalation for a human call.

4. Agent Support: If escalated, the AI tools for debt recovery teams provide the human agent with real-time scripts, compliance alerts, and AI-driven suggestions for optimizing repayment schedules.

5. Compliance & Audit: Throughout the process, the system maintains a complete, immutable audit trail of all communications, ensuring regulatory compliance across all AI for banking debt collection activities.

This intelligent automation for collections significantly shortens recovery cycles and dramatically reduces the cost-to-collect.

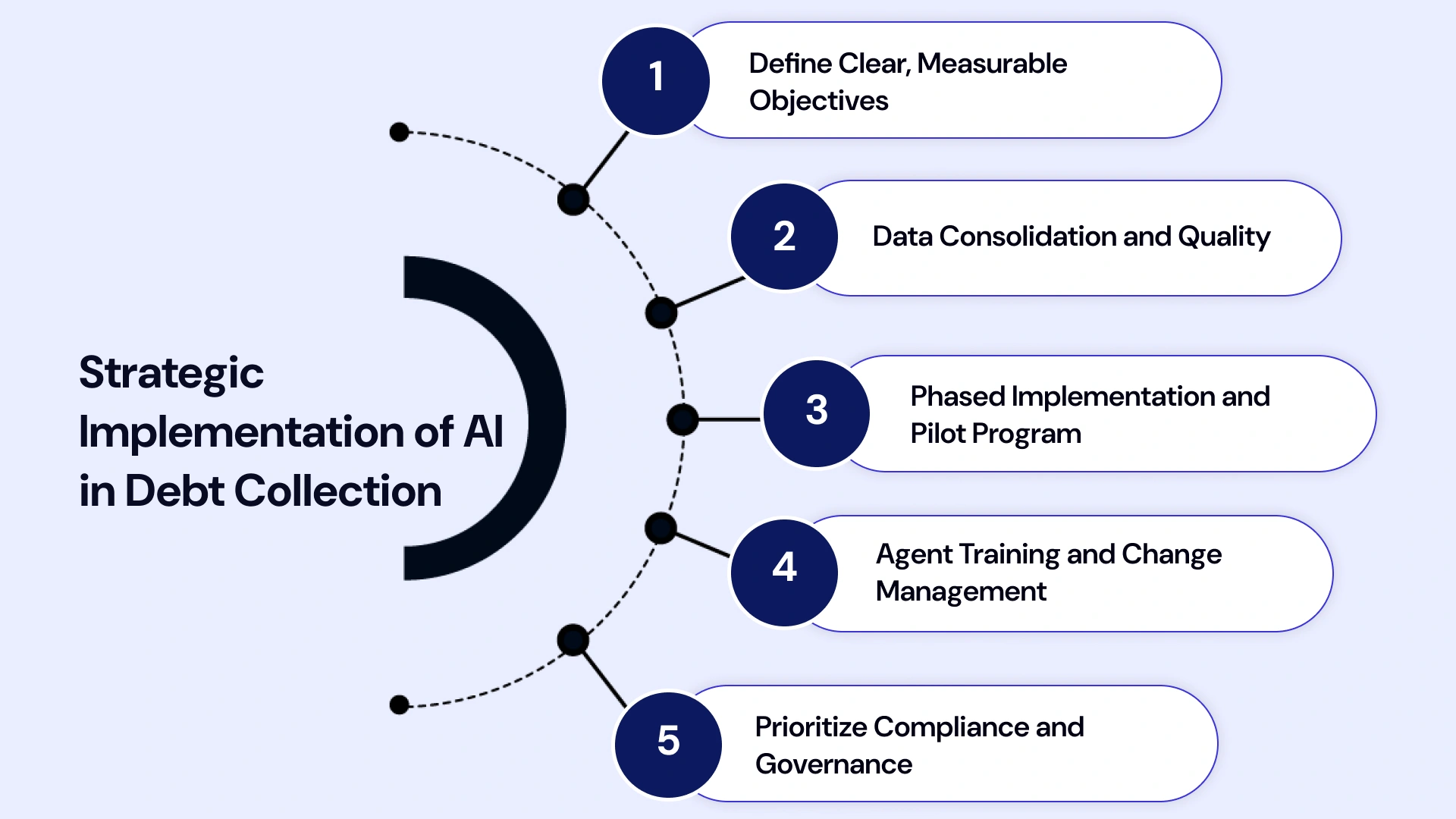

AI Debt Collection Implementation Strategies

Successfully adopting AI into a debt collection strategy requires a clear roadmap, whether through partnering with AI Development Services or leveraging in-house Software Development Services.

1. Define Clear, Measurable Objectives

Start with specific, achievable goals. Instead of "Improve collections," aim for "Reduce 30-day delinquency rate by 5% within 12 months" or "Increase self-service payment portal usage by 20%." These concrete targets will define the scope for the AI debt collection solutions.

2. Data Consolidation and Quality

The performance of machine learning in debt collection is entirely dependent on data quality. Financial institutions must consolidate fragmented data from legacy debt-collection technology systems, CRM systems, and communication logs. Data preparation is the most time-consuming but crucial step for achieving high accuracy in AI for loan default prediction.

3. Phased Implementation and Pilot Program

Do not attempt a full-scale rollout immediately. Start with a focused pilot program on a specific, manageable portfolio (e.g., all personal loans delinquent 30-60 days). This enables AI debt collection solutions to be fine-tuned and for teams to be trained on the new AI-powered debt recovery workflows before scaling.

4. Agent Training and Change Management

AI is meant to augment, not replace, human collectors. Training should focus on leveraging AI tools for debt recovery teams—using AI-suggested scripts, understanding predictive scores, and specializing in complex negotiation cases that the AI filters out. This positive change management is key to adoption.

5. Prioritize Compliance and Governance

Regulatory compliance, particularly in North America, must be a non-negotiable feature. The chosen platform must include automated regulatory monitoring and be architected for robust data privacy and security to support AI for loan collection activities.

Future Trends: AI Debt Collection Solutions

The evolution of AI debt collection is poised for continuous growth, driven by advancements in generative AI and greater integration with financial technologies.

- Hyper-Personalized Negotiations: Future AI chatbot for debt collection will use Generative AI to conduct sophisticated, hyper-personalized negotiations in real time, tailoring language, tone, and offers based on sentiment analysis of the debtor's input.

- Predictive Portfolio Management: Credit risk analytics using AI will move beyond individual accounts to manage entire portfolios, automatically restructuring credit limits or proactively offering refinance options for at-risk segments before widespread delinquency occurs.

- Voice and Emotion AI: Voice recognition and emotion AI will analyze live call data to determine a debtor’s stress level and sentiment, allowing the system to instantly adjust the collector's script or the offered payment plan for maximum de-escalation and success.

- Blockchain Integration: The use of blockchain technology will enhance the transparency and auditability of the entire AI debt collection workflow automation process, providing an immutable record for regulatory bodies and debtors alike.

Choose VLink Expertise to Improve Debt Collection Strategies

The transition to an AI in debt collection model is a complex strategic undertaking, not merely a technology installation. It requires deep expertise in AI Development Services, financial regulations, and the ethical application of machine learning in debt collection.

At VLink, our dedicated team specializes in delivering enterprise-grade AI debt collection solutions that deliver measurable ROI while ensuring compliance.

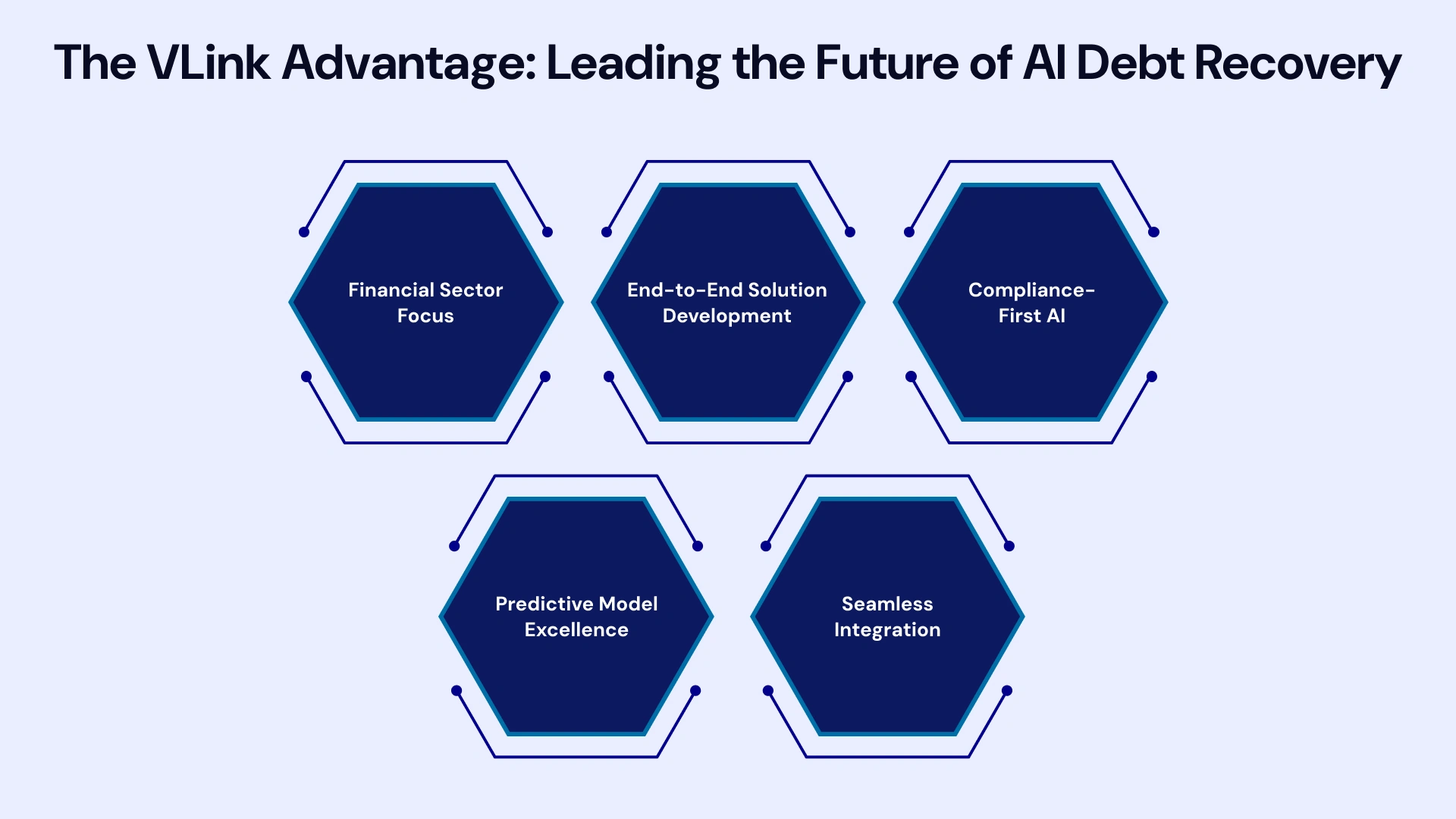

Why Partner with VLink for AI-Powered Debt Recovery?

- Financial Sector Focus: Our expertise is rooted in decades of serving banks and fintech lenders. We understand the critical nuances of AI for banking debt collection, AI for mortgage loan collections, and high-volume AI for credit card debt collection.

- End-to-End Solution Development: We offer complete Software Development Services to either integrate AI models into your existing debt collection technology stack or deploy a custom, scalable AI debt management platform.

- Compliance-First AI: Our AI-powered debt recovery platforms are engineered with automated compliance monitoring built into the core, giving US and Canadian institutions confidence that their AI-driven debt collection automation adheres to all federal and provincial regulations.

- Predictive Model Excellence: Our data scientists develop proprietary AI risk-scoring models for collections and loan default prediction, continuously trained on massive datasets to deliver the highest possible accuracy and predictive power.

- Seamless Integration: We ensure your new AI debt collection workflow automation integrates seamlessly with legacy core systems, CRMs, and communication channels, minimizing disruption and maximizing data flow for superior predictive analytics in debt collection.

Whether you require advanced AI-based collection strategy optimization or a full overhaul toward intelligent automation for collections, VLink provides the strategic consulting and technical AI Development Services necessary to secure a competitive edge and significantly boost your recovery rates.

Conclusion

AI in debt collection is the definitive path forward for banks and fintech lenders, marking a decisive shift from costly, reactive manual systems to a precision-driven, empathetic, and compliant AI-powered debt recovery model.

The strategic advantage is clear: massive operational cost reductions are achieved alongside significantly higher recovery rates, fueled by AI for loan default prediction and hyper-personalized customer outreach. By fully leveraging AI- and advanced analytics-driven debt collection automation, organizations can transform their collections function from a reactive cost center into a powerful, proactive engine for profitability and risk mitigation.

For institutions operating in a highly regulated market, investing in ethical, data-driven AI debt-collection solutions is no longer a competitive choice—it is a prerequisite for sustainable growth. The market leaders of tomorrow will be those who demonstrate that efficiency and customer empathy can, and must, go hand-in-hand in the future of finance.

Are you ready to move beyond outdated collection practices and implement a compliance-first, AI-powered debt recovery strategy? Partner with our experts to design and deploy custom AI debt-collection solutions that maximize recovery rates while ensuring rigorous regulatory compliance.

Vice President, Strategy – VLink Inc.

Sambhavi Gopalakrishnan is the Vice President of Strategy at VLink Inc., bringing over a decade of experience in IT leadership, project implementation, and strategic growth. She possesses a strong foundation in technical project management and pre-sales, driving innovation and business transformation at VLink.

Shivisha Patel

Shivisha Patel