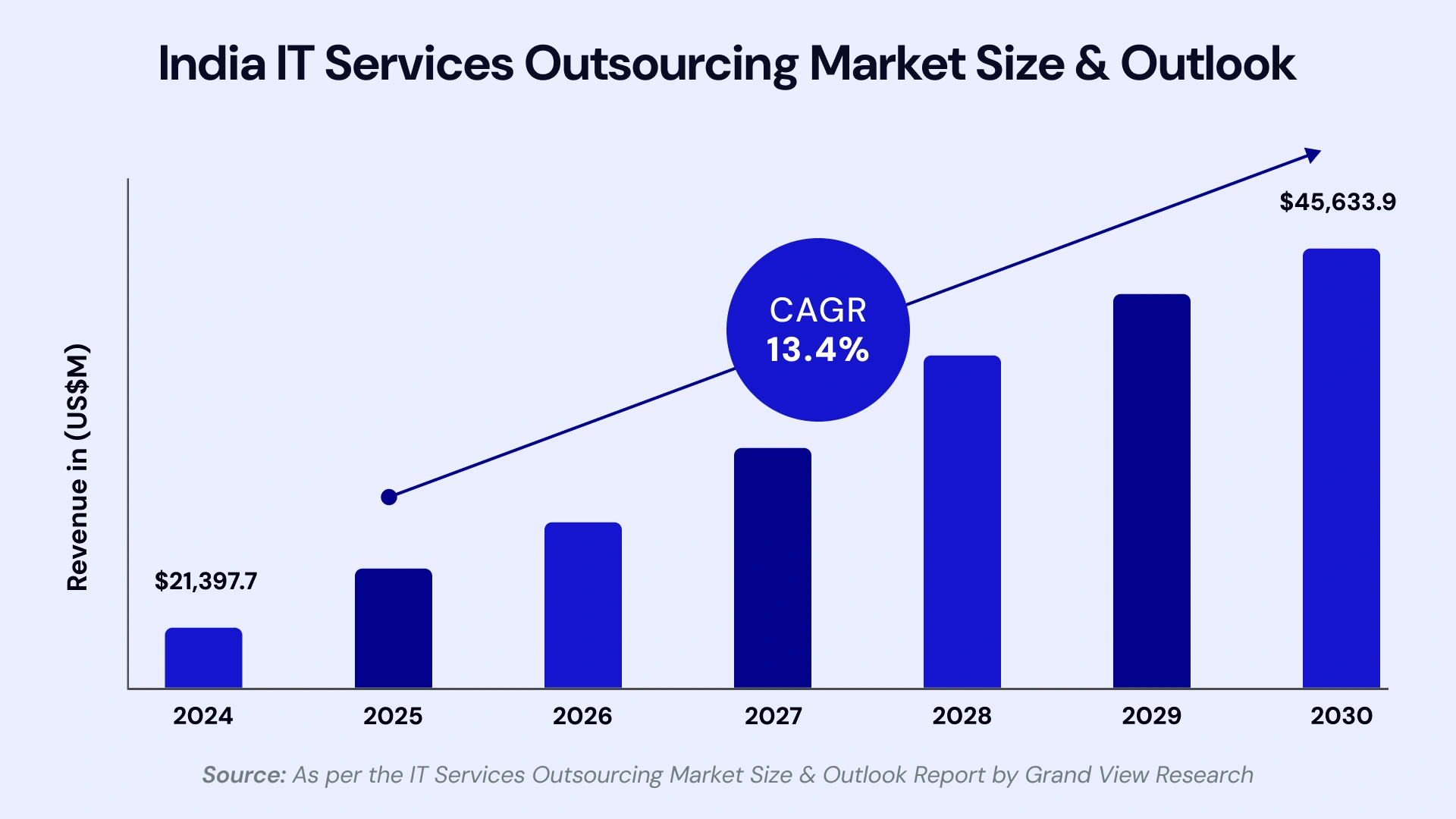

A compound annual growth rate of 13.4% is expected of India's services outsourcing market from 2025 to 2030.

Yet with scale comes risk — and with risk comes regulation.

The Reserve Bank of India has drawn a line in the sand. Whether you're a PSU bank migrating workloads to AWS, a private bank deploying a SaaS-based core banking system, or an NBFC integrating a fintech partner for loan origination, the compliance clock is ticking.

April 10, 2026, is the RBI deadline for NBFCs to align existing vendor contracts with the 2025 Outsourcing Directions. Banks are already under active scrutiny. And the rules are clear: outsourcing your IT functions does not outsource your accountability.

This RBI IT Outsourcing Compliance guide is written for CIOs, CTOs, and enterprise architecture leaders in Indian banking and financial services. It is not a legal commentary. It is an operating manual — with frameworks, checklists, and a 30-60-90 day action plan you can use tomorrow.

What RBI IT Outsourcing Compliance Means in 2026

The phrase 'IT outsourcing compliance' is often treated as a legal formality. Inside the RBI framework, it is something far more operational — and consequential.

When a bank or NBFC outsources any IT function to a third party — a cloud provider, SaaS vendor, managed SOC, or data analytics firm — it enters a regulated relationship. The RBI's directions on IT outsourcing govern every aspect of that relationship: how it is selected, contracted, monitored, audited, and exited.

The 'Zero-Dilution Responsibility' Principle

The foundational rule of every RBI outsourcing direction is this: regulated entities (REs) remain fully responsible for any service or function they outsource. There is no liability transfer to the vendor. If your cloud provider suffers a breach and customer data is exposed, the RBI holds your bank — not the vendor — accountable.

This principle shapes every compliance requirement. Audit rights, SLA monitoring, subcontractor visibility, and BCP obligations all exist to ensure the bank retains effective control of outsourced functions. This is the lens through which every CIO and CTO must read the IT Outsourcing Compliance Guide.

Why Outsourcing No Longer Transfers Risk

In practice, many compliance gaps arise because IT leaders assume that vendor certifications — such as ISO 27001, SOC 2, and PCI-DSS — satisfy RBI requirements. They do not. Certifications are a baseline. The RBI requires banks and NBFCs to conduct independent due diligence, maintain their own audit rights, and verify that vendor controls actually align with RBI IT audit outsourcing for banks standards.

The 2025 NBFC Directions and the 2023 Bank Directions both reflect a regulatory philosophy: trust is earned through verification, documentation, and continuous oversight — not delegation.

Who Must Comply? Banks vs NBFCs Explained

The RBI IT Outsourcing Compliance Guide applies differently depending on your entity type. Understanding the distinction is critical — both for compliance planning and for prioritizing your resource allocation.

Entities Covered Under RBI Directions

- Public Sector Banks (PSU Banks) — nationalized banks and the SBI group

- Private Sector Banks — domestic private banks and small finance banks

- Foreign Banks — operating through branches in India

- Non-Banking Financial Companies (NBFCs) — particularly systemically important NBFCs (SI-NBFCs), upper-layer NBFCs, and those with significant digital operations

- Payment System Providers — where IT outsourcing intersects with payment processing

Bank vs NBFC Compliance Differences

The table below summarizes the key differences in compliance scope and timeline:

Parameter | Banks (PSU, Private, Foreign) | NBFCs (Systemically Important) |

Governing Direction | RBI Master Directions on IT Outsourcing (2023) | RBI Directions: Managing Risks in Outsourcing (2025) |

Compliance Deadline | Already effective; ongoing compliance required | April 10, 2026 (transition period active) |

Board Policy Mandate | Board-approved outsourcing policy mandatory | Board-approved policy mandatory for material activities |

Audit Rights | Full right to audit IT vendors and sub-contractors | Audit rights clause mandatory in all contracts |

Cloud / SaaS | Covered; data localization rules apply | Covered; NBFC must map cloud vendors as material |

Subcontracting | Requires prior approval + visibility of 4th-party risk | Vendor must disclose sub-contractors; NBFC approval needed |

Supervisory Oversight | Direct RBI inspection; quarterly reporting in some cases | NBFC responsible; RBI may inspect vendor premises |

Core RBI Principles Every CIO & CTO Must Understand

The RBI's outsourcing framework is built on four operational pillars. These are not abstract legal concepts — each one maps directly to decisions you make as a technology leader.

Accountability & Governance

The board of directors is ultimately responsible for all outsourced functions. This is non-negotiable. As CIO or CTO, you are the bridge between technical vendor relationships and board-level accountability. This requires you to maintain a current vendor register, conduct periodic risk reviews, and escalate concentration risks before they become supervisory findings.

Customer Protection & Data Responsibility

Any outsourced function that involves customer data — names, financials, transaction history, KYC documents — must be governed by strict data handling controls. Data localization outsourcing compliance is a specific obligation: customer data must remain within India unless explicitly permitted otherwise. Cloud vendors claiming 'India region' availability must be independently verified by your architecture team.

Operational Resilience & Continuity

Outsourcing cannot create a single point of failure. Operational resilience in RBI IT outsourcing means that if a vendor fails, goes bankrupt, or suffers a cyberattack, the bank must continue critical operations. This requires active BCP/DR testing — not just documented plans. RBI inspectors increasingly ask for evidence of DR tests, not just DR policies.

Risk-Based Materiality Classification

Not every outsourced vendor requires the same level of scrutiny. The RBI expects you to classify vendors by materiality — based on whether the function is critical to operations, involves customer data, or creates concentration risk.

Use this framework to make that determination:

- Does the vendor handle or process customer data? → High materiality

- Would a service outage halt business-critical operations? → High materiality

- Is this vendor also used by 3+ other banks / NBFCs? → Concentration risk flag

- Does the vendor use subcontractors you cannot identify? → Sub-contracting risk

Governance Model: What RBI Expects from Your Organization

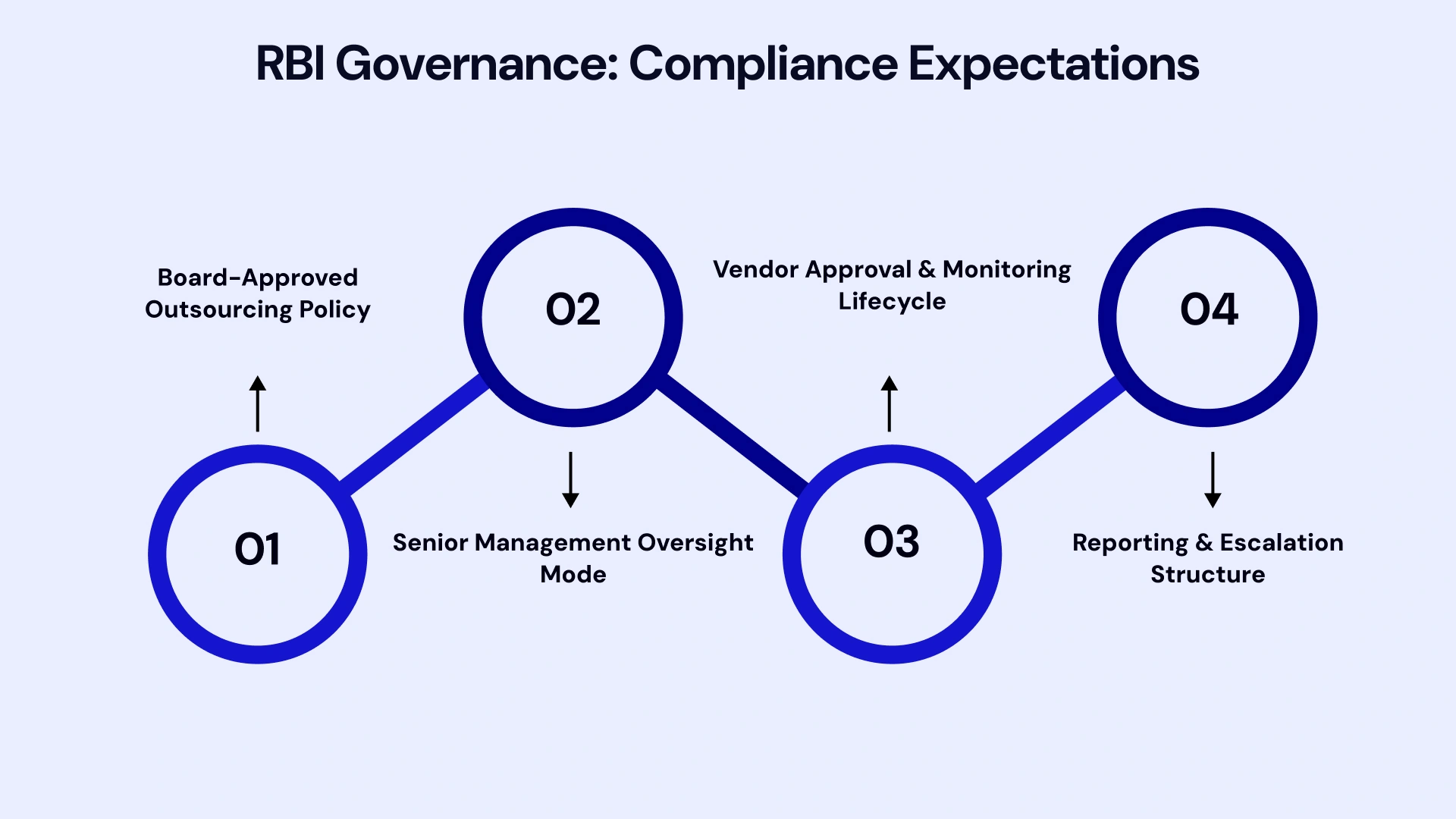

Governance is where RBI inspectors begin. Before examining vendor contracts or audit logs, they want to see whether the bank has a functioning oversight structure for outsourced IT.

Board-Approved Outsourcing Policy

Every bank and NBFC must have a board-approved outsourcing policy that covers IT outsourcing. This policy must define what constitutes a material activity, how vendors are approved, who holds accountability at each level, and how disputes and failures are managed. The policy should be reviewed and reapproved annually — and that review must be minuted.

Senior Management Oversight Model

Beneath the board sits the senior management oversight layer. For technology-intensive banks, this typically means the CTO or CIO chairs a Vendor Risk Committee or IT Outsourcing Steering Group. This body reviews vendor performance quarterly, escalates material risks to the board, and approves new material vendor engagements.

Vendor Approval & Monitoring Lifecycle

RBI outsourcing compliance for banks requires a lifecycle approach to vendor management: pre-approval due diligence, contract execution with mandatory clauses, periodic performance reviews, and formal exit planning. This lifecycle must be documented — not just practiced.

Reporting & Escalation Structure

Regulatory incidents involving IT vendors — system outages, data breaches, vendor failures — must have a defined reporting path to RBI within prescribed timelines. Your incident response plan must include vendor-triggered events, not just internal failures.

IT Vendor Due Diligence Checklist (Pre-Onboarding)

The most common RBI inspection finding? Banks and NBFCs onboarded vendors without a structured due diligence process. The IT outsourcing due diligence checklist below is your pre-onboarding defense.

Security & Data Protection Controls

- Verify encryption standards at rest and in transit (AES-256 minimum)

- Review the vendor's data classification and retention policy

- Confirm data localization — customer data hosted within India

- Assess IT outsourcing for cybersecurity risk: vulnerability scanning cadence, VAPT reports

- Check incident history and regulatory breach disclosures

SLA, Uptime & Performance Metrics

- 99.9% uptime SLA minimum for critical systems; penalty clauses for breach

- Recovery Time Objective (RTO) and Recovery Point Objective (RPO) are defined in the contract

- Escalation matrix for Severity 1 incidents with RBI-reportable thresholds

Subcontracting & Fourth-Party Risk

- Full disclosure of subcontractors is required before onboarding

- Bank/NBFC must approve material sub-contractor changes in advance

- Sub-contracting risk RBI outsourcing: flow-down clauses mandatory in vendor contracts

- Audit rights must extend to subcontractors handling your data

Financial & Operational Stability

- Audited financials for the last 2 years

- Key-person risk assessment — especially for niche IT vendors

- IT vendor risk management: reference checks with other regulated entities

Exit Strategy & Reversibility Planning

- Data return and deletion timelines are defined in the contract

- Knowledge transfer obligations on the vendor in the event of termination

- Migration assistance: vendor must support transition to alternate provider

Vendor Risk Scoring Model

Use this scoring model to assess and document vendor risk before onboarding:

Risk Dimension | Weight | Score (1–5) | RBI Relevance |

Data security & encryption controls | High | ___ | Customer data protection obligation |

SLA performance & uptime history | High | ___ | Operational resilience requirement |

Sub-contractor disclosure | Medium | ___ | 4th-party risk & concentration |

Exit strategy & data return plan | High | ___ | Reversibility & continuity |

Audit rights contractually secured | Critical | ___ | RBI inspection access |

Financial stability of vendor | Medium | ___ | Third-party risk management banks |

Incident response & reporting SLA | High | ___ | Regulatory reporting obligation |

Cloud, SaaS & SOC Outsourcing: Hidden Compliance Risks

This is where the RBI IT Outsourcing Compliance Guide diverges most sharply from competitor content — and where most CIOs have the largest exposure.

SaaS Is Not 'Low Risk' Under RBI

A common misconception: SaaS tools used for non-core functions carry low compliance risk. Under the RBI framework, if that SaaS tool processes, stores, or transmits customer data, it is a material outsourcing activity. This includes CRM platforms, HR tools with employee financial data, and analytics dashboards fed by banking APIs.

Cloud Data Localization Challenges

Cloud outsourcing guidelines require careful mapping. AWS, Azure, and GCP all offer India regions — but multi-region replication, backup storage, and disaster recovery configurations can silently route data outside India. Your architecture team must audit cloud configurations, not just vendor certifications. Data localization outsourcing compliance is a technical obligation, not just a contractual one.

SOC Outsourcing & Log Ownership Rules

Outsourcing your Security Operations Centre (SOC) is now common in Indian BFSI. The RBI's expectations are clear: even if the SOC is operated by a third-party, your bank owns the logs. Your bank retains audit access. Your bank defines the incident escalation path. The vendor cannot control what data is reported to RBI or limit your visibility into security events on your own infrastructure.

Subcontractor Visibility Problem

Cloud vendors use subcontractors for infrastructure, colocation, and content delivery. Many SaaS platforms run on AWS or Azure without disclosing this to their bank customers. This creates a chain of fourth-party risk that the RBI expects banks to map and manage. If you cannot name the subcontractors processing your customer data, you are not compliant.

Red Flags: Stop These Vendor Relationships Before They Start

- No audit rights in the contract — walk away or renegotiate

- SLA below 99.5% for critical systems

- Unknown or undisclosed subcontractors

- No exit clause or data return obligation

- Data storage location unverified beyond the vendor's own assurance

- No incident escalation path tied to RBI-reportable thresholds

Concentration Risk, BCP & Disaster Recovery Expectations

Concentration risk in IT outsourcing is one of the RBI's most active areas of supervisory concern. When multiple banks rely on a single cloud provider, a single fintech API gateway, or a single data center, the failure of that provider becomes a systemic risk.

Vendor Concentration Risk

The RBI expects banks and NBFCs to monitor and report concentration, not just manage it at the individual entity level. If more than 30–40% of your critical IT operations are dependent on a single vendor, that is a concentration risk requiring board attention and mitigation planning. This applies to cloud providers, core banking vendors, and data analytics platforms equally.

Business Continuity Planning (BCP)

Business continuity plan IT outsourcing RBI requirements go beyond having a BCP document. The RBI expects evidence of: annual BCP tests involving outsourced vendors, documented results shared with the board, and remediation plans where gaps are found. BCP must cover the scenario where your primary IT vendor is unavailable for 72 hours or more.

Disaster Recovery (DR) Testing Requirements

Example scenario: Your bank uses a single cloud provider for core banking. A ransomware attack takes the vendor offline. Can you restore operations within your RTO?

If the answer is uncertain, your DR strategy is not RBI-ready. The RBI requires annual DR tests with documented RTO/RPO outcomes. These results must be available for RBI supervisory inspection.

Audit Readiness: Documents You Must Maintain

When an RBI inspection dedicated team arrives, the first thing they ask for is documentation. Not your strategy. Not your roadmap. Your evidence. Here is what you need — mapped to RBI inspection expectations.

Document / Evidence | Responsible Owner | RBI Inspection Relevance |

Board-approved outsourcing policy | Board / Company Secretary | Governance & oversight |

Vendor risk assessment reports | CTO / CISO | IT outsourcing due diligence checklist |

Signed IT outsourcing contracts with RBI clauses | Legal / Procurement | Contract compliance |

SLA performance logs (last 12 months) | Vendor Manager | Operational resilience RBI IT outsourcing |

Incident log and RBI-reported incidents | CISO / IT Head | Regulatory reporting |

BCP / DR test results and dates | IT Architecture / CTO | Business continuity plan IT outsourcing RBI |

Sub-contractor disclosures | Procurement | Sub-contracting risk RBI outsourcing |

Exit strategy test records | Architecture Lead | Concentration risk in IT outsourcing |

Evidence RBI Inspectors Typically Ask For

- Board meeting minutes showing outsourcing policy approval and annual review

- Vendor risk assessment reports for all material IT vendors (last 2 years)

- Copies of IT outsourcing contracts with RBI-mandated clauses highlighted

- SLA performance reports and incident logs for the last 12 months

- DR test results and BCP activation records

- Sub-contractor disclosure register with approval evidence

- RBI-reportable incident log and communication records

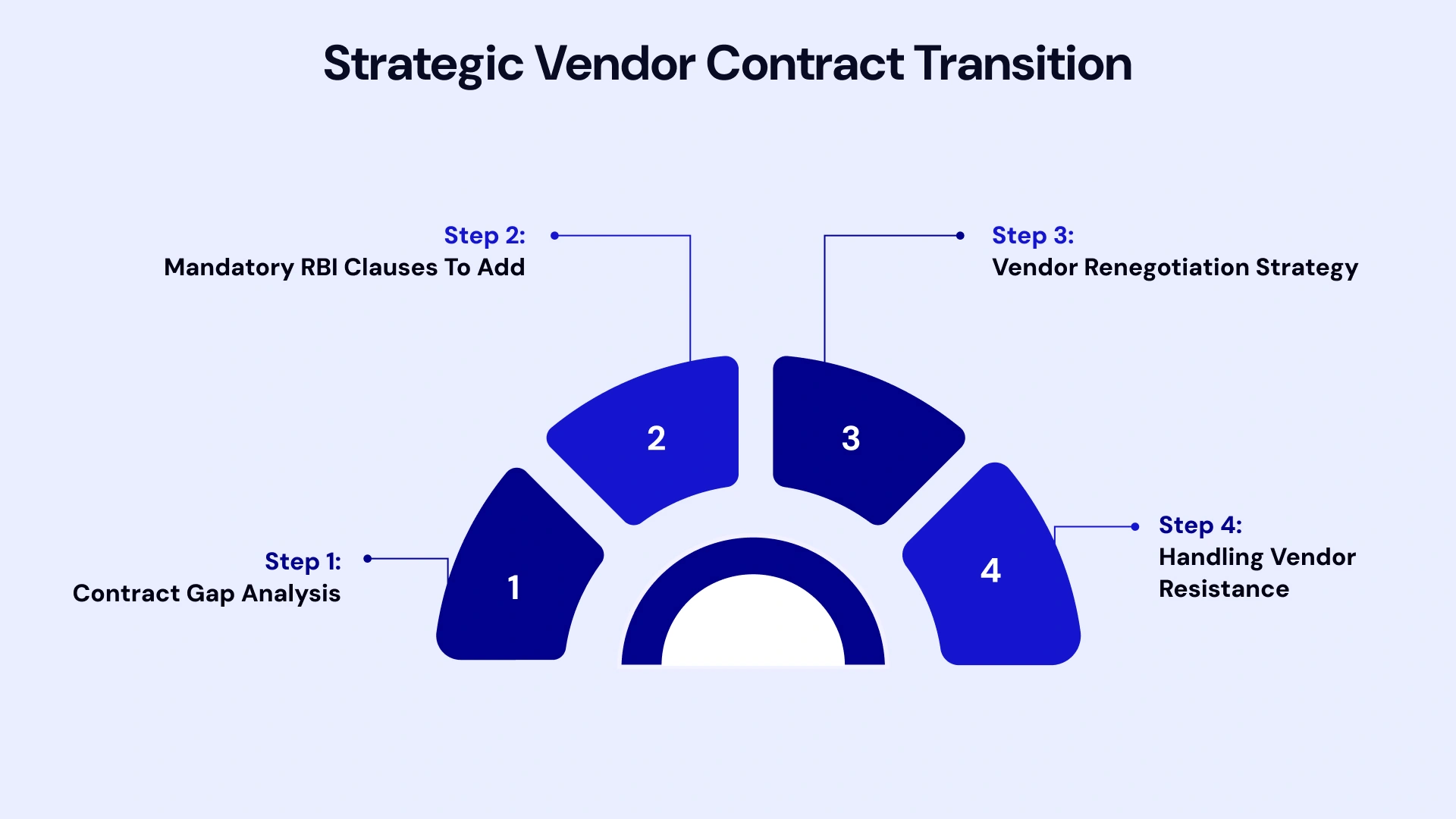

Transition Strategy for Existing Vendor Contracts

If your NBFC has existing vendor contracts that pre-date the 2025 RBI Directions, you are in a transition window — but the window is closing. Here is how to move efficiently without disrupting live operations.

Step 1: Contract Gap Analysis

Map every existing IT vendor contract against the RBI's mandatory clause list. Key gaps typically found: missing audit rights clauses, no sub-contractor disclosure obligation, inadequate exit provisions, and SLAs that do not meet RBI operational resilience thresholds.

Step 2: Mandatory RBI Clauses to Add

- Right to audit the vendor and its subcontractors at any time

- Obligation to disclose subcontractors and obtain prior approval for changes

- Data return and deletion timelines on contract termination

- Incident reporting obligation: vendor must notify the bank within 6 hours of a material event

- BCP cooperation clause: vendor must participate in the bank's BCP and DR tests

- RBI access clause: RBI has the right to inspect vendor premises related to bank operations

Step 3: Vendor Renegotiation Strategy

For strategic vendors, frame the renegotiation as a mutual compliance exercise — not a punitive review. Most mature IT vendors (especially those serving multiple Indian banks) already have RBI-aligned contract addenda ready. Ask for their standard regulated-entity addendum.

Step 4: Handling Vendor Resistance

If a vendor refuses to accept audit rights or sub-contractor disclosure obligations, that is a red flag, not a negotiating point. Material vendors who resist RBI-standard clauses represent a regulatory risk you cannot carry. Consider initiating a dual-vendor strategy or accelerating exit planning.

30-60-90 Day Implementation Plan

| Phase | Key Actions | Owner |

| Day 1–30 | Complete vendor inventory; classify by materiality; identify contract gaps | CTO, Procurement, Legal |

| Day 31–60 | Renegotiate contracts; add RBI mandatory clauses; run vendor risk scoring | Legal, CISO, CTO |

| Day 61–90 | Activate BCP/DR testing; document audit trail; submit board report | CTO, Board, Compliance |

Step-by-Step RBI IT Outsourcing Compliance Framework

Here is the operating model — a five-step framework that converts RBI guidelines on outsourcing of IT services into an executable compliance program.

Step | Activity | RBI Compliance Link |

1 | Vendor Inventory & Classification | Identify material vs non-material activities; classify cloud, SaaS, SOC vendors |

2 | Risk & Materiality Mapping | Apply outsourcing risk management framework; score by data sensitivity and criticality |

3 | Due Diligence & Contract Controls | Run IT outsourcing due diligence checklist; embed RBI-mandated clauses |

4 | Continuous Monitoring | Track SLA, incidents, sub-contractor changes; quarterly board reporting |

5 | Exit Strategy Testing | Test data retrieval, migration and BCP annually; document results for RBI supervisory inspection |

Real-World Use Cases: Banks & NBFCs

Below are some of the primary real-world use cases currently transforming the sector:

PSU Bank Cloud Migration Case

A large public sector bank migrated its analytics workloads to a public cloud provider. Initial compliance review found the vendor's India-region replication included EU backup nodes — a data localization violation. The bank's architecture team renegotiated storage configurations documented the change and added an annual configuration audit obligation to the vendor contract. Result: clean RBI inspection finding in the next supervisory cycle.

NBFC Fintech Integration Case

A systemically important NBFC integrated a fintech partner for digital loan origination. The fintech used three sub-contractors for credit bureau access, e-KYC, and cloud storage — none disclosed at onboarding. Post the 2025 Directions, the NBFC ran a sub-contractor mapping exercise and found concentration risk: two of the three sub-contractors were also used by seven other NBFCs in the same product segment. Mitigation: alternate vendor onboarded for credit bureau access; fourth-party risk register established.

Common Mistakes That Trigger RBI Findings

In 2026, the Reserve Bank of India (RBI) intensified its "Risk-Based Supervision" (RBS), moving away from simple checklist audits to deep behavioral and systemic analysis. Findings (deficiencies identified during inspections) often lead to penalties, business restrictions, or "Show Cause" notices.

The following are the most common "preventable" mistakes that trigger RBI findings for Banks and NBFCs today:

- Over-relying on vendor certifications (ISO, SOC 2) as a substitute for independent due diligence

- Contracts without audit rights — the most frequently flagged RBI outsourcing compliance gap

- Weak SLA enforcement — agreements exist, but breaches are not tracked or penalized

- No sub-contractor register — NBFC cannot name who processes its customer data

- BCP plans that exist on paper but have never been tested with vendor participation

- Concentration risk unmonitored — single vendor used for 60%+ of critical IT functions

- Exit clauses missing — no plan for data recovery if the vendor relationship ends

Modernizing Banking Operations with VLink's Strategic Solutions

RBI IT outsourcing compliance is not just a risk management exercise — it is the foundation for confident digital transformation. At VLink, we work with BFSI enterprises to build technology operations that are both innovation-ready and regulation-proof.

Whether you need IT staff augmentation services to plug compliance gaps in your vendor oversight function or dedicated teams to build your third-party risk management framework from the ground up, VLink's BFSI practice brings cross-functional expertise across tech talent sourcing in India and regulatory alignment.

Our BFSI compliance specialists have supported banks and NBFCs across:

- Vendor inventory and materiality classification exercises

- RBI-aligned contract gap analysis and renegotiation playbooks

- Cloud architecture reviews for data localization compliance

- IT staff augmentation strategies for fintech teams managing third-party risk

- BCP/DR testing programs that satisfy RBI supervisory inspection standards

- Dedicated teams for continuous vendor monitoring and quarterly board reporting

VLink does not just tell you what the regulations say. We build the operating infrastructure that makes compliance a repeatable, scalable function — not a one-time audit scramble.

Conclusion: Compliance as a Competitive Advantage

The CIOs and CTOs who treat RBI IT outsourcing compliance as a checklist exercise will always be one RBI inspection away from a supervisory finding. The ones who treat it as an operating model will use compliance as a lever for trust, resilience, and competitive differentiation.

In Indian BFSI, regulatory trust is a brand asset. An NBFC that can demonstrate clean vendor governance, robust BCP, and proactive risk management is not just compliant — it is investment-grade. A bank that leads on outsourcing risk governance builds the foundation for faster, safer digital transformation.

Use this RBI IT Outsourcing Compliance Guide as your starting point. Translate it into vendor contracts, board policies, and operating procedures. And if you need a partner with deep BFSI compliance and technology execution experience, VLink is ready.

Ready to move from compliance risk to compliance confidence? Talk to VLink's BFSI Experts Today. Book a Strategy Call Now!

Vice President & Global Head of Digital, VLink Inc.

Amitabh is the Vice President and Global Head of Digital at VLink Inc., with over 20 years of leadership experience in IT strategy, digital transformation, and emerging technologies.

Shivisha Patel

Shivisha Patel